China's people are on a treadmill

They're working hard for someone else's benefit.

“And the man in the suit has just bought a new car/ From the profit he’s made on your dreams” — Traffic

Leftist online personality Hasan Piker recently took a trip to China, and — like many other influencers who have been there — declared it to be a paradise, praising “abundance style consumption paired up with a centrally controlled economy” and “1950s Soviet era building blocks next to the Gucci store”.1 Meanwhile, pro-China pundits continue to crow about the country’s technological achievements and export performance.

But when you talk to ordinary Chinese people about what their lives or their families’ lives are like these days, a less rosy picture emerges. Helen Gao writes:

Behind the orderliness of everyday life, a quiet desperation simmers. On social media and in private conversations, there is a common refrain: worry over joblessness, wage cuts and making ends meet…

Internationally, China looks strong…That muscular facade is punctured here in China, where despair about dimming economic and personal prospects is pervasive. This contrast between a confident state and its weary population is captured in a phrase Chinese people are using to describe their country: “wai qiang, zhong gan,” roughly translated as “outwardly strong, inwardly brittle.”…

Many now feel the very state policies that have made China appear strong overseas are hurting them. They see a government more concerned with building global influence and dominating export markets than in addressing the challenges of their households…These days, there is a sense of bitter anger among the people at being the voiceless victims of the state’s obsession with world power and beating the United States…The government recently began cracking down on social media content it considered “excessively pessimistic” — a clear sign it is concerned about this public unease undercutting its agenda.

For even more direct insight, I recommend the blog Reading the China Dream, which translates Chinese writing and online commentary. The blog has a good translation of a recent report from a Chinese marketing company on morale among the youth. Here are some excerpts from the bloggers’ summary:

The text translated here is [the] last of a series meant to sum up 2024 and preview 2025…[T]he tone of the text is unsparingly bleak: the China Dream has stalled and no one knows what to do about it…Chinese young people inherited great expectations from China’s phenomenal economic rise, which began to slow in the 2010s, and from the democratization of China’s higher educational system…This ringing success has fallen flat because the job market has not kept up with university expansion. Consequently, China’s vulnerable generation…find themselves in a limbo defined by a flat job market, stagnant salaries, and high prices, especially for real estate…This appears to be where China is now: school is a marathon, but nobody wins.

And this is from the translated report itself:

The number of young people who are depressed or anxious continues to rise, and young people have the worst emotional state of all age groups. The China National Mental Health Report (2019-2020) shows that young people aged 18-34 have the highest anxiety level; at the same time, people’s mental health level has dropped significantly compared with ten years ago.

Young people’s emotional problems are becoming more and more serious, especially in the context of fierce competition in education…As a result, emotional problems tend to emerge at a younger age. Through longitudinal comparison, the China Youth Research Center found that between 2015 and 2020, the sense of hope of primary and secondary school students decreased by 11.8 percentage points.

This all fits with everything my Chinese expat friends tell me about how their relatives are faring back home. It also fits with the descriptions of young Chinese people’s disillusionment in Dan Wang’s recent book Breakneck.

Essentially, it seems as if Chinese people — especially young people — are stuck on a treadmill. China’s young people are studying hard, getting a college education, and putting in grueling long work hours. And yet youth unemployment rates are rising relentlessly, many college graduates can’t find the kind of white-collar work they trained for, and wage growth is sluggish. To a huge number of Chinese people, the modern Chinese economy is less of a “Chinese Dream” than a Sisyphean nightmare.

In fact, the word “treadmill” also hearkens back to where China’s problems began. Way back in 2010, hedge fund manager Jim Chanos declared that China’s real estate market was on a “treadmill to hell”. That prediction was way too early — the real estate market probably didn’t become a bubble until the late 2010s, and didn’t begin to crash until near the end of 2021.

But crash it eventually did, and four years later it’s still in a protracted state of collapse. Despite government support, Chinese property prices are still falling:

China’s home-price slump worsened in October, ending a traditionally peak sales season with a weak reading as recent loosening measures failed to revive the moribund market…New-home prices in 70 cities, excluding state-subsidized housing, dropped 0.45% from September, the steepest decline in a year, National Bureau of Statistics figures showed Friday. Resale home values fell 0.66%, the fastest slide in 13 months.

This price decline is a catastrophe for regular Chinese households. Even more than in most countries, Chinese households have their wealth concentrated in real estate. The stock market is underdeveloped, and bonds have crappy interest rates,2 so people save money by buying houses or housing-linked bonds. When real estate prices go down, it means Chinese people are getting poorer and poorer, despite working hard and living frugal lives.

The property bust is also weighing on the macroeconomy. Property investment is down almost 15% since a year ago. This is a big reason why unemployment is rising, wages are stagnant, and lots of college grads can’t find jobs commensurate with their skills.

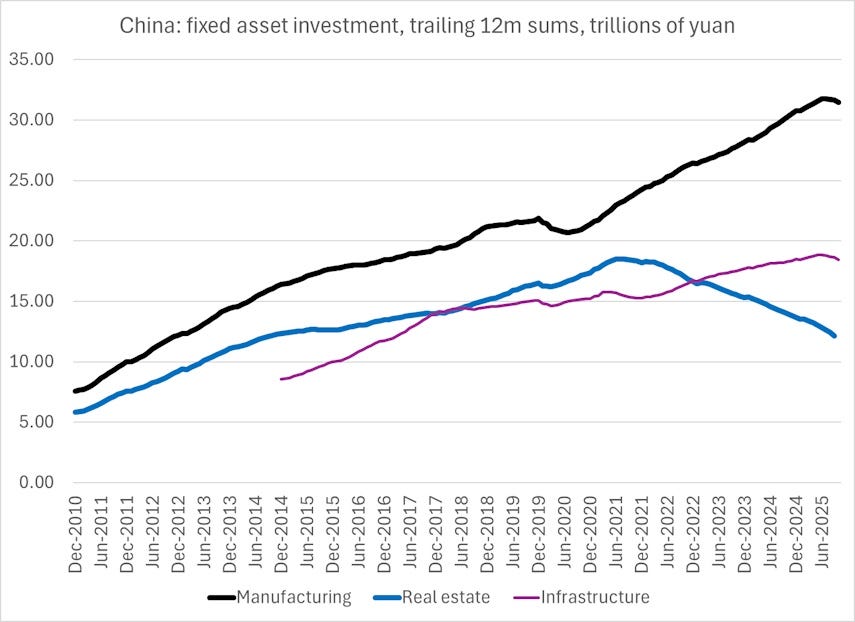

For a while, China used manufacturing investment to fill the economic hole left by real estate. The country embarked on the greatest industrial policy push in human history, spending an estimated 4.4% of GDP on manufacturing subsidies of various kinds. Industrial lending and output surged, keeping GDP growth from collapsing even as the real estate sector floundered.

But this strategy also hit its limits. It turns out that if you pay a whole bunch of companies to make the same products, they end up competing viciously with each other, and their profits evaporate. Here are some excerpts from a recent story in the Atlantic about China’s EV industry, which is both beating the world and floundering financially at the same time:

The Chinese electric car has become a symbol of the country’s seemingly unstoppable rise on the world stage…[But] bloated by excessive investment, distorted by government intervention, and plagued by heavy losses, China’s EV industry appears destined for a crash. EV companies are locked in a cutthroat struggle for survival. Wei Jianjun, the chairman of the Chinese automaker Great Wall Motor, warned in May that China’s car industry could tumble into a financial crisis; it “just hasn’t erupted yet.”…

Dunne Insights, a California-based consulting firm focused on the EV industry, counts 46 domestic and international automakers producing EVs in China, far too many for even the world’s second-largest economy to sustain…In most economies, the market would sort out this mess by culling the weakest players…In China, state support or ownership of automakers extends the life of struggling businesses. Local governments are also reluctant to lose the jobs they bring, so officials prop up unprofitable companies. The city of Wenzhou recently helped arrange financing for an EV maker called WM Motor, to get the company’s local factory humming again. The city of Hefei rescued the EV start-up Nio in 2020, but the publicly listed company continues to lose money—$1.6 billion in the first half of this year.

This so-called “involution” results in misallocation of capital, reducing productivity growth and ultimately slowing GDP growth. By destroying profit margins for even the best-run Chinese companies, involution damages their ability to invest for the future. The excessive corporate competition from involution contributes to China’s overwork problem, because it gives companies an incentive to work their employees to the bone in order to get a competitive edge. And worst of all, involution drives down prices, causing deflation that exacerbates the value of the debt left over from the property bubble.

So China’s leaders are going on an “anti-involution” campaign. It’s not clear what this means — the details of the policy are mostly out of the public eye — but if it’s anything like what Japan’s industrial policy bureaucrats did to stop “excessive competition” in the 1970s, it will probably involve telling Chinese companies to get together and all raise their prices at the same time.

That’s going to mean slower growth. Why? Because demand curves slope down. If Chinese car companies all raise their prices, fewer cars will be sold. Another way of saying the same thing is that the easiest way to raise prices is to curb production. Either way, this means less investment, because Chinese companies won’t need to build as many factories. And less investment means slower GDP growth in the short run.

In fact, this might already be happening. China’s fixed-asset investment has begun to fall in the last few months, right around the time the anti-involution campaign began. Bloomberg reports:

China’s economic activity cooled more than expected at the start of the fourth quarter…Fixed-asset investment shrank 1.7% in the first 10 months of the year…according to data released by [China’s] National Bureau of Statistics…Bloomberg Economics estimates investment dropped as much as 12% in October, extending its streak of declines into a fifth straight month.

And here’s a chart:

This investment drop is a bit statistically weird, since it contradicts some other data sources. Data quality in this area is notoriously bad. But it seems to fit with some other pieces of data, such as slowing loan growth — especially industrial loans — and rising unemployment.

It also fits with the generally pessimistic mood that Chinese people express about their economy:

Chinese households became more pessimistic last quarter and their view of the jobs market fell to the worst ever, according to a survey by the central bank…Consumers turned increasingly negative about income, employment, and prices in April-June, the poll showed…

The data also revealed that people’s willingness to consume dropped to the weakest since the outbreak of the pandemic, with almost two-thirds of respondents saying they want to save more, while an employment index fell to a record low…The data also showed a shrinking percentage of respondents expecting consumer and housing prices to rise.

Put this all together, and it makes perfect sense that Chinese people — especially young people — would be feeling futile and pessimistic. They’ve been hit with a bunch of huge negative shocks, all within a short space of time:

A real estate bust that destroyed a significant portion of their wealth, as well as their hopes of asset appreciation in the near future

An economic slowdown that destroyed expectations of constantly rising living standards, made it hard for people to find jobs, and meant that lots of college degrees are going to waste

A government industrial policy that encouraged “involution”, made a lot of people work hard for little gain, and exacerbated the hangover from the property crash

These negative shocks would be brutal for any country. But for China, which has known nothing but skyrocketing living standards for over three decades, it’s especially galling to be suddenly thrust into a world where you have to run flat-out just to stay in place.

Ten years ago, Chinese people worked hard because they knew that tomorrow would be much better than today; now, they work hard because they know that if they don’t, tomorrow will be much worse than today. Their dream has suddenly flipped from aspiration to survival.

All of this raises the question of who, exactly, the modern Chinese nation-state is built for. In many ways, China is the greatest nation on Earth — it has endless miles of high-speed rail, futuristic technological marvels, vast productive power, sprawling malls and highways and forests of towering apartment blocks. Its cities sparkle with light, drones zip through its skies, and robots crawl along its streets. And yet many of its people now toil in quiet desperation. It feels like a nation built for the glory and greatness of its leaders and owners, rather than for the happiness of its regular people.

This was not always true, of course. Under Deng Xiaoping, Jiang Zemin, and Hu Jintao, China vanquished poverty, created a vast middle class, and made a concerted effort to spread its new prosperity all across the nation. That was always the deal — prosperity for political quiescence. Now, under Xi Jinping, the deal has been altered. China’s people are basically being told “Let them eat national greatness.”

Interestingly, this is very similar to my own description of Chinese urban life: “at the end of the day you live in an isolated tower block and you drive to the mall.”

This is partly due to China’s strategy of “financial repression” — a policy of keeping interest rates low in order to make it cheap for businesses to borrow.

Very interesting analysis. Couldn't help but thinking, in parts of it, that you were talking about the U.S.

Wow... what a great article. China has engaged in four macro strategies all of which would seem at some point come to roost.

1) Currency Manipulation: To keep the perception of low-cost manufacturing.... however, the result would seem to be to rob the Chinese consumer of buying power.

2) Real Estate Loan Growth: well documented

3) Picking Winners/Losers in industrial policy: leading to large capital misallocations

4) Wolf diplomacy: making foreign markets wary of Chinese dependence and building a large cost in defense.

I am curious if there has been any serious economic work in modeling these topics in academia ?