Roundup #84: Bears on bikes

Vibecession (or not); AI depolarization; Existential AI risk; Millennials vs. Boomers; Deindustrialization; Russian oil revenue; GLP-1s; AI and jobs

An old friend recently wrote to me, telling me that I needed to write a blog post about bears on bicycles. He wrote: “The internet needs a large, apex predator trying its best to navigate a two-wheeled vehicle through the complexities of global supply chains and geopolitical shifts.” Wise words indeed. AI-generated words, to be sure, but full of wisdom nonetheless.

Writing a Noahpinion post about bears on bikes sounded challenging, but I’m never one to shrink from a challenge. So I’ve tried to include bears on bikes as a thematic throughline in today’s roundup.

But first, a podcast. I went on Sam Harris’ podcast to talk about the state of the macroeconomy! His podcast is paywalled, but you can listen to the first quarter of the discussion here:

Here’s a YouTube preview, if you like video.

Anyway, on to the roundup!

1. What if the “vibecession” is just bad data?

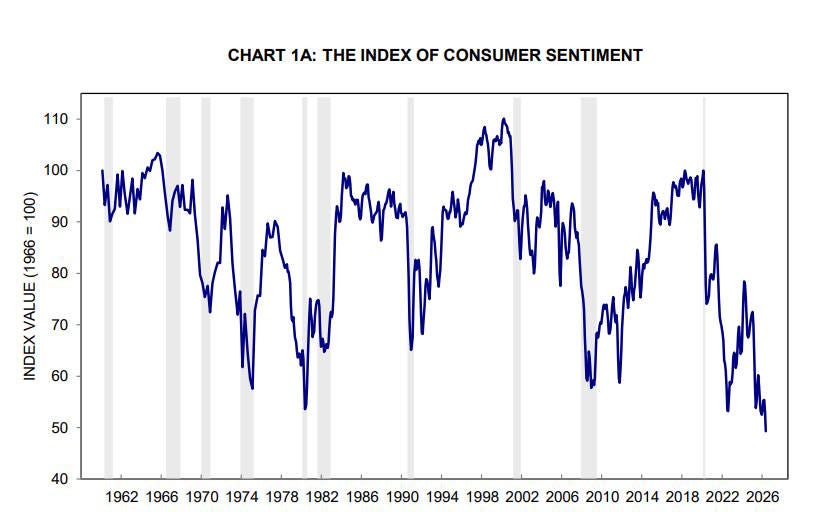

For years now, we’ve been wondering why Americans are in the dumps about the economy even though inflation is still relatively low and the employment rate is historically high. This “vibecession” is still happening, and it’s reaching absurd levels. The University of Michigan’s Index of Consumer Sentiment has hit its lowest level on record — lower than the inflation of the 70s, lower than the Great Recession, and lower than Covid:

Potential explanations have included:

Americans expressing unhappiness about political and social conflict by claiming the economy is bad

Increased partisanship making either Democrats or Republicans loath to admit that the economy is good, depending on which party has the presidency

High interest rates making it unaffordable to buy a home

A delayed reaction from years of rising service costs or other long-simmering economic difficulties

Now, over at Nate Silver’s blog, Joel Wertheimer has another potential explanation: Maybe the consumer sentiment data is just bad!

He writes:

The University of Michigan ICS [Survey of Consumers] is the gold standard sentiment survey measuring consumer sentiment. The survey has historically shown a very strong correlation with “hard” economic data such as inflation and unemployment. But…As with election polls, the ICS has struggled amid a shift away from telephone polling…So the problems with the ICS are these:

The switch to online polling made responses more negative and,

There are too many Democrats in the sample.

Thus, ICS data since mid-2024 is not comparable to past periods…Democrats right now say they hate the economy with Trump in charge…

When adjusted for these issues, the ICS should be substantially higher than the Great Recession lows we have witnessed over the past year. Weighting the survey to Pew’s National Public Opinion Reference Survey…would place the ICS at a level more like that in 2013…This adjustment would bring the survey in line with other measures of consumer confidence, such as those from the Conference Board, Gallup, and YouGov.

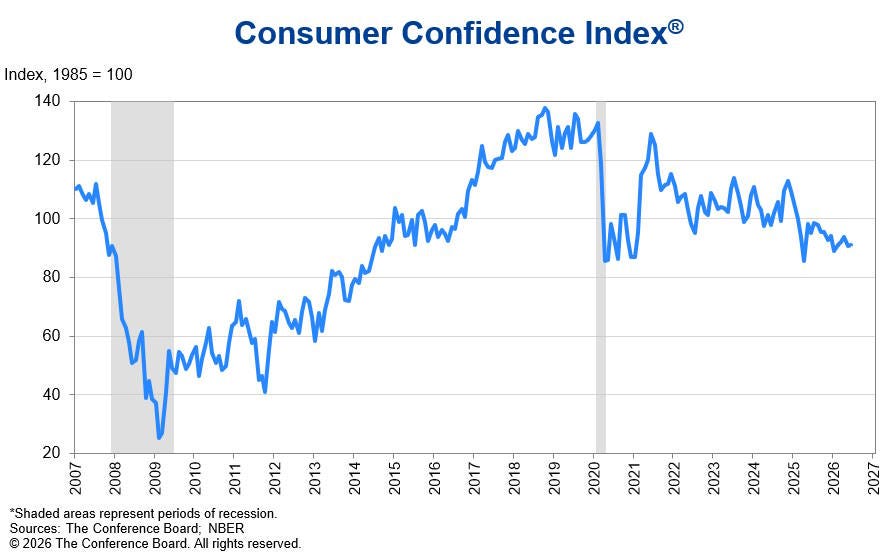

This seems like an important point. The Conference Board’s survey shows consumer confidence down from 2019, but still pretty good:

Gallup and YouGov don’t have data from before 2020, so I’m not sure how to use those as bases for comparison, but the disparity between the Conference Board’s survey and the University of Michigan’s survey seems important. And notice that the Conference Board doesn’t even show a “vibecession” during Biden’s term in office!

And although I missed it at the time, Ryan Cummings and Ernie Tedeschi did show that the University of Michigan’s index of consumer sentiment fell by 9 points when they shifted from telephone polling to online polling in 2024:

In other words, the notion that American consumers are ultra-bearish might be perched upon a flimsy bicycle of bad data.

So it might be that Americans are simply a lot less angry about the economy than we thought. That would be heartening from a “people are rational after all” standpoint, though perhaps disappointing for those who are hoping for a Democratic electoral sweep this fall.

2. A bit of evidence for Digital Cronkite

Back in March, I wrote a hopeful post about how AI might de-radicalize our politics:

The basic idea was twofold:

AI can inject lots of information into debates in real time, in order to bring them back to reality and correct misinformation.

AI is trained on a sample of writing from Democrats AND Republicans, so it tends to be more moderate than the typical human being in a polarized society.

I called depolarizing AI “Digital Cronkite”, because it could be a modern version of Walter Cronkite’s moderate voice of authority on broadcast television in the mid 20th century.

My post cited some papers in support of the thesis. Here’s one more. Conlon and Schwardmann (2026) set out to study the phenomenon of “AI sycophancy” — i.e., AI telling people what they want to hear. Sycophancy is a well-documented phenomenon — if you tell AI that bears ride bikes, it’s disturbingly likely to agree. Some people are naturally afraid that sycophancy will increase political polarization, by reinforcing people’s political beliefs. If AI tells Democrats “Yes, Republicans are bad and you’re right about everything,” and if it tells Republicans “Yes, Democrats are bad and you’re right about everything,” that could seemingly entrench polarization by turning every human-AI conversation into a little echo chamber.

But Conlon and Schwardmann found that AI does the exact opposite of this! From their abstract:

Our experiment involves 1,500 participants in 30 decision environments spanning core domains in economics and the social sciences…[W]e find that AI advice depolarizes choices on average, moving participants away from their initial leanings. This depolarization arises despite the LLM being measurably sycophantic: it disproportionately offers considerations that support users’ initial leanings and uses agreeable and flattering language. Depolarization occurs across moral and non-moral, objective and subjective, strategic and non-strategic, and complex and simple tasks. Increasing sycophancy weakens depolarization, showing that sycophancy is behaviorally relevant, even if it is generally outweighed by the informativeness of AI advice. [emphasis mine]

The authors go with the “substantive information” theory of AI depolarization, and they find some evidence to support it:

Why then does our baseline LLM depolarize choices, despite being sycophantic? One hypothesis is that it combines its agreeable framing with enough substantive information to counteract sycophancy’s polarizing force. Several facts corroborate this interpretation. First, in objective tasks, interacting with the baseline AI improves accuracy by 0.12 standard deviations (p < 0.05)…In contrast, we find no evidence that extra deliberation time, reactance, noise, or ceiling effects drive our results.

Interestingly, Conlon and Schwardmann don’t think about what seems to me to be the most obvious reason for AI depolarization — i.e., that AI is trained on the average of society, and thus is the ultimate Moderate Normie. That’s something worth following up on.

But whatever the reason, this is another piece of evidence in favor of the Digital Cronkite thesis. You should probably be a little more optimistic about AI’s effect on human politics.

3. A bad argument from a good economist about AI risk

Anthropic recently hired Chad Jones, my favorite growth theorist. That’s great news, both for Chad and for Anthropic! But a Financial Times article about the hire catches Chad saying some highly questionable things about existential AI risk in a working paper back in 2023:

What is the price of this amazing change in living standards? Recall that we would face a flow probability of existential risk of 1% per year for 40 years, so the probability we survive this A.I. explosion is exp(−.01 × 40) ≈ 0.67. In other words, with log utility it is optimal to take a 1 in 3 chance of ending human existence in exchange for a 2/3 chance of dramatically raising living standards by a factor of 55.

Chad’s point here is not that we should be blasé about the existential risk from AI. His purpose in the paper is to compare different utility functions and show how our attitude toward existential risk can change a lot depending on risk aversion. But I still don’t like his calculation here.

The main reason is that Chad sets the utility of human extinction equal to zero. This isn’t actually log utility. Log utility is just u(c) = ln(c), where c is consumption. If you consume nothing at all, then ln(c) = ln(0) = -∞. In other words, if you take log utility seriously, then death is infinitely bad.

That presents a problem for economic models, since it means that even the slightest chance of death is so scary — scarier even than a bear on a bicycle — that humans would do basically anything to avoid it. That obviously isn’t realistic. So instead, economists using log utility typically model it with a fudge factor. One option is to just set u=0. This is the assumption that if you’re dead, you’re not getting any utility from anything, so your utility should just be zero forever.

That’s what Chad Jones is doing in this paper, and it’s that choice that drives his result. But it’s a highly dubious assumption. Recall that ln(1) = 0. So this means that if you assume u(extinction) = 0, you’re saying that “humanity going extinct” is no worse than “humanity existing for all eternity at some baseline level of consumption”. That doesn’t sound realistic to me.

A better choice — which is what some economists do — is to set the utility of death equal to some constant, and then try to calibrate that constant against data on risky behavior. The constant wouldn’t be zero, and it would greatly alter Chad’s calculations on how much benefit we’d need from AI in order to accept existential risk.

But even here, we have to be cautious. Human extinction is not the same as an individual’s death. A lot of people would probably accept a lot less risk if they knew they were risking the lives of their families, friends, countrymen, and fellow human beings, than if they were only risking their own life. So you have to be very careful when looking at how much people care about the risk of the whole species dying.

Chad was not being careful here. I know this was 2023, before existential risk seemed like a serious thing to people outside the AI industry. But now that he’s at Anthropic, he should be more circumspect about these things.

4. Millennials are doing better than Boomers (but are more unequal)

During the 2010s, there was a pretty common narrative that economic progress had stalled in America, and that the Millennial generation had been screwed over. You still hear a few progressives argue this, but in general this narrative has been in retreat as new data has come in. As the Millennials have eased into middle age, it has become apparent that like every generation before them, they have experienced substantial economic progress. I first blogged about this shifting narrative back in 2023:

But I was a bit late to the party here — bloggers like Jeremy Horpedahl had been pushing back on the “generational stagnation” thesis for years.

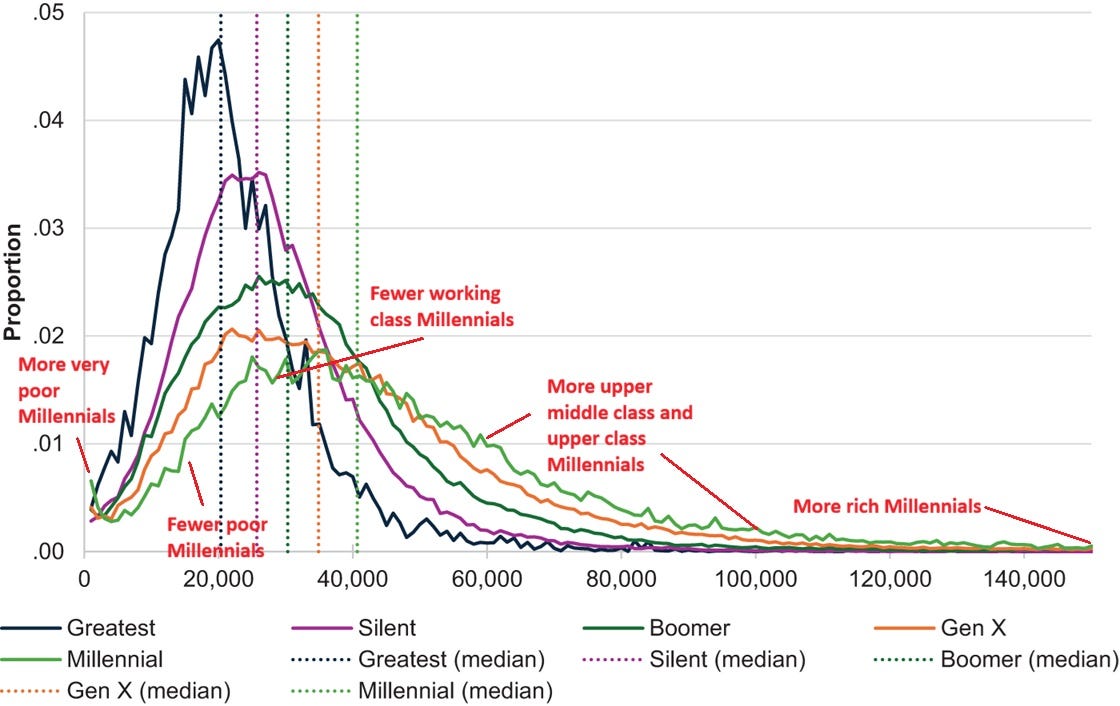

Anyway, as we get more data, Millennials’ advancement becomes even clearer. Tyler Cowen points us to Corinth and Larrimore (2026), who measure the income of each generation after all taxes and government transfers are accounted for. You can basically see the results in one chart, which I’ve helpfully labeled:

These are income distributions — they measure how many people in each generation are living at each level of income at an equivalent age, after adjusting for inflation (i.e., after adjusting for changes in the cost of living). What you can see here is:

There are a lot fewer Millennials making less than $30,000 (in 2019 dollars) than any other generation did at age 36-40.

There are more Millennials making over $40,000 than any other generation, and Millennials dominate other generations at every income level above $40,000.

It’s hard to observe incomes above $140,000, so these are left off the graph.

It looks like there are a few more Millennials making exactly zero income than other generations. This could reflect people who are still being supported by their parents, or people who somehow fall through the cracks in the data gathering process.

The Millennial income distribution is more spread-out — as Millennials have done better overall, some have seen bigger gains than others, resulting in increased inequality within the Millennial generation.

This is a pretty reasonable description of the reality that we’ve all seen over the course of our lives — most Millennials are more comfortable than their parents were, just as most Boomers are more comfortable than their parents were.

This doesn’t mean government redistribution is unnecessary — indeed, Corinth and Larrimore explicitly calculate income after redistribution has taken place. And America has become more redistributionary. So government is helping produce upward mobility for the poor. This is a big government success story.

But the narrative that Millennials are falling behind, and that the Boomers screwed their children over, just doesn’t hold up in the income data.

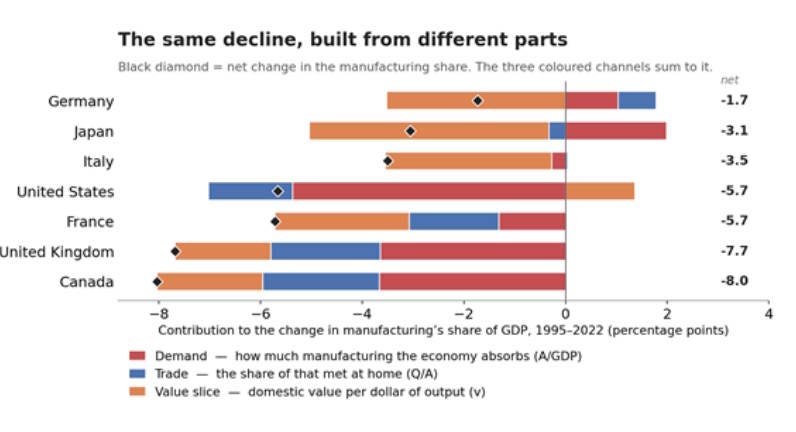

5. Why did America deindustrialize?

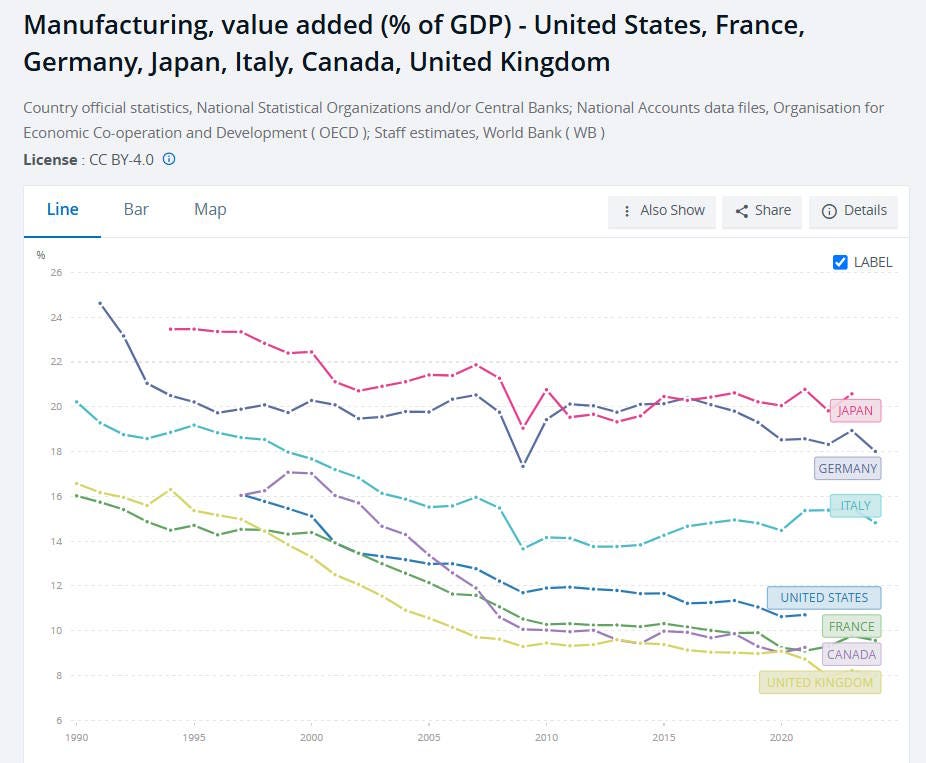

As countries get richer, manufacturing tends to become a less important part of their economies. You can just look at the declining trends for manufacturing as a percent of GDP in rich nations over the years:

A lot of people think that this happened because we outsourced our manufacturing to China. Other people think it’s because our demand for manufactured goods topped out over time, and we started to want to consume more services.

In fact, it was both of these! Richard Baldwin has a post decomposing each rich country’s deindustrialization into three factors:

How much demand shifted away from manufactured goods

How much final goods production shifted from domestic production toward imports

How much intermediate goods production shifted from domestic production toward imports

He finds that the rich countries have very different stories, even if their overall numbers look similar. Here’s the key chart:

America did actually outsource a fair amount of its final goods production, but this was almost balanced out by onshoring of intermediate goods production (at least, in terms of monetary value). Almost all of America’s deindustrialization since 1995 came from Americans spending a smaller % of their money on manufactured goods.

For other countries, it’s a different story. Germany and Japan actually spent more on manufactured goods, but lost tons of market share in the intermediate goods sector. For France, Canada, and the UK, all three factors contributed to deindustrialization.

This is very interesting. It implies that the simple, common story of “we outsourced everything to China” holds true for other rich countries — at least, in a generalized sort of way — a lot more than for the United States. For the U.S., the main reason we make less stuff is that we want less stuff — at least, relative to how many “experiences” we want to consume.1

6. How much did the Iran War help Russia?

The wheels are falling off the bicycle for the Russian bear. Ukraine is taking far fewer casualties, as it switches to a drone-intensive way of war that Russia has so far been unable to match. Russia is losing over a thousand men a day in futile assaults. Meanwhile, Ukrainian long-range strike drones are wreaking havoc on Russia’s logistics, strangling occupied Crimea, destroying Russian refineries, and causing fuel shortages throughout Russia. Meanwhile, the strain of war production is starting to cause cracks in Russia’s government finances.

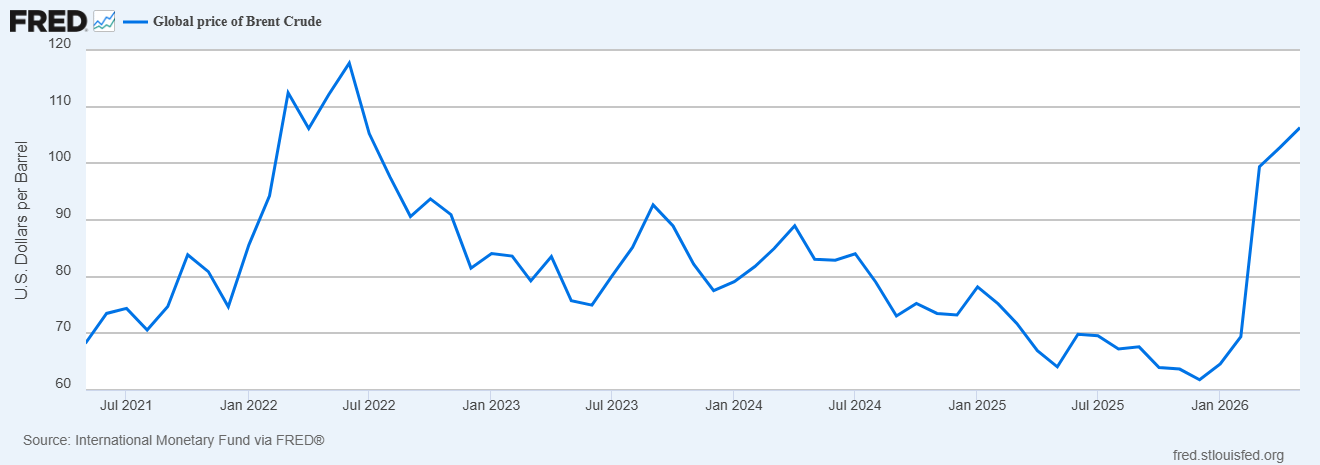

Russians had hoped that Donald Trump would ride to their rescue, pressuring the Ukrainians into ceding territory. He certainly tried, but was ultimately unable to bully the stubborn Ukrainians into backing down. But some believed that Trump would help Russia in a more indirect, accidental way — by launching a war against Iran, the hapless U.S. President would cause oil prices to spike and flood the coffers of Russia’s government with much-needed cash.

Indeed, when Iran closed the Strait of Hormuz — which ultimately decided the war in its favor — it caused oil prices to soar:

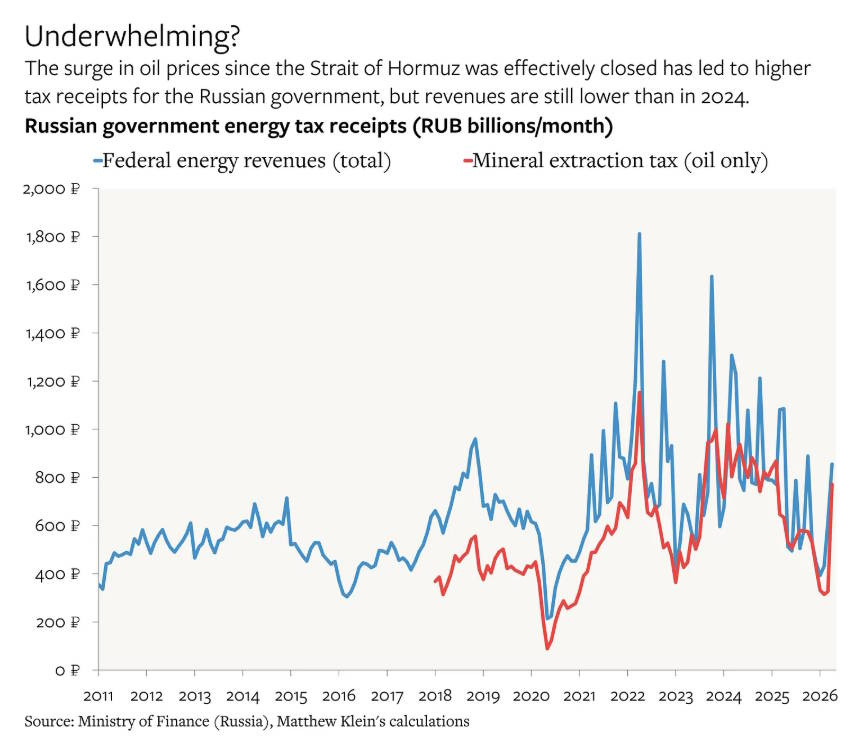

But at least by April — the most recent month we have data for — the benefits to Russia had been a lot smaller than Putin supporters hoped. Matt C. Klein had a good post about this:

Here’s the key chart:

Why has Russia only reaped a small windfall? One reason is the strengthening ruble, which means fewer rubles of revenue for every dollar of crude oil sales. Another reason is that Russia has been paying its refiners to keep fuel prices down in the face of Ukrainian attacks; because they handle these payments as tax deductions rather than as expenditures, it reduces the total amount of oil and gas revenue.

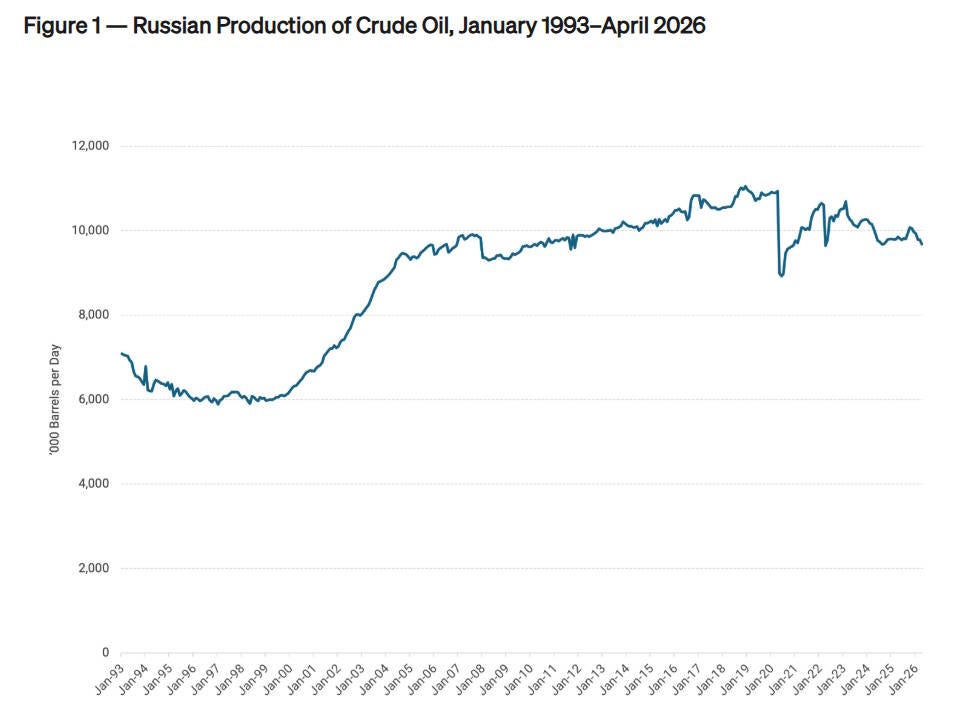

But there’s a third reason, which is a lot scarier for the Russians. The country’s crude oil production is falling:

Ultimately, it’s production declines that doom a petrostate — just look at what happened to Venezuela when Hugo Chavez starved the state oil company of funds for reinvestment.

Russia needs to invest huge amounts of money to expand production in Siberia, where the easily accessible oil is gone and only harder-to-get supplies remain. War spending may be starving the oil industry. And Western export controls may be successfully starving the Russian oil industry of the technology it needs to build and maintain its extraction infrastructure.

If this is true, then Russia is in big trouble. Crude oil exports are the big prop holding up Russia’s whole economy — no amount of macroeconomic policy or war mobilization can compensate for its loss. Putin’s Russia is a classic petro-empire that uses wealth extracted from the land to fund imperial conquests; when the oil runs out, such empires collapse.

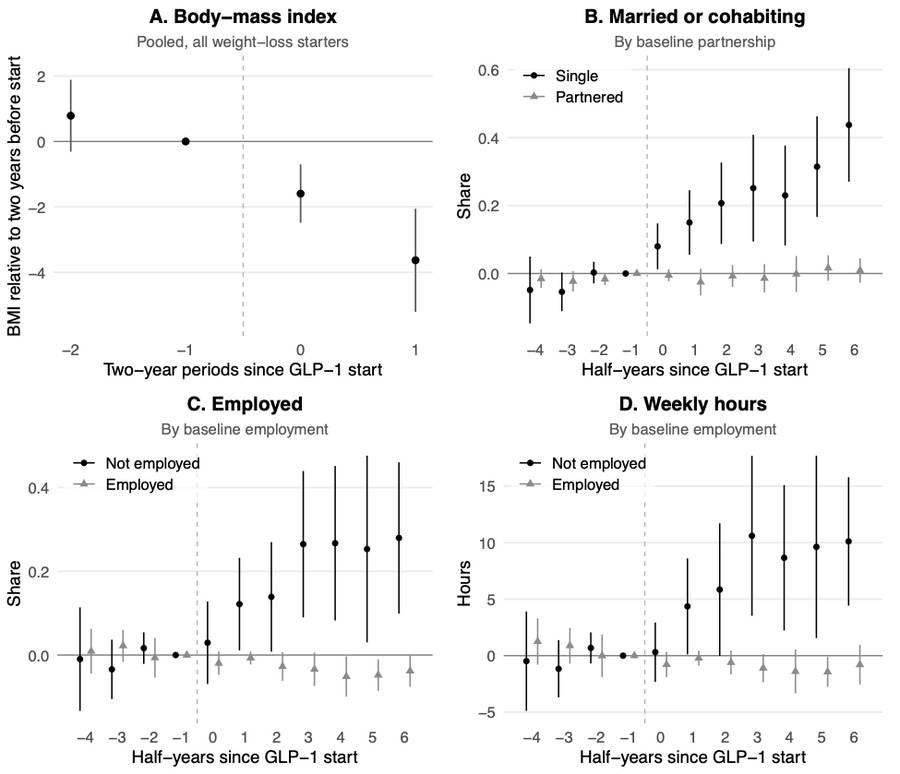

7. Not being fat is probably good for you

Usually, when you see eye-poppingly large estimates for the effect of some sort of policy or medicine or whatever, you should immediately distrust the methodology of the paper. But Rebecca Diamond is one of the most serious and respected empirical microeconomists in the business, so when she says that GLP-1 drugs have almost magical effects on women’s lives, we should at least sit up and listen.

Diamond’s paper compares people who go on GLP-1 drugs to A) those who say they want to go on the drugs but don’t, and B) those who go on the drugs a bit later. For men, she finds relatively few life changes beyond weight loss itself. But for women, she finds some pretty big effects! According to Diamond’s estimates, single women who go on the weight-loss drugs are 29% more likely to get married or cohabit over the next three years, and women without jobs are 27% more likely to get jobs, relative to the women who didn’t go on the drugs.

That’s a pretty dramatic result! It gives us one more reason — beyond the obvious health benefits — to treat weight loss as a technological problem, and just get on with it by any means necessary. The “fat acceptance” movement has gone too far — we should treat excess weight not as a piece of who we are, but simply as a physical impediment to be managed or removed. Fat is basically just a fat suit, and you can take it off if you want.

That said, there are some reasons why you shouldn’t put too much faith in this one empirical result. Although Diamond of course does an incredibly thorough job in trying to compare the GLP-1 users with the non-users in an apples-to-apples way, there’s still the possibility that people who actually go ahead and use the drugs are just different than people who don’t, or who use them only with a lag. They might be more purposeful, more motivated, etc. And that could explain at least part of their greater likelihood of getting a partner and getting a job.

What we really need here is a natural experiment — some policy that affects how easy it is for people to get GLP-1 drugs, preferably with different timing in different places. If we find similarly positive effects from that sort of study, we can be even more certain that these drugs are wonder drugs.

(Of course, drugs aren’t the only thing you should do to lose weight. You should also go for a bike ride! Especially if you’re a bear.)

8. The latest on AI and jobs

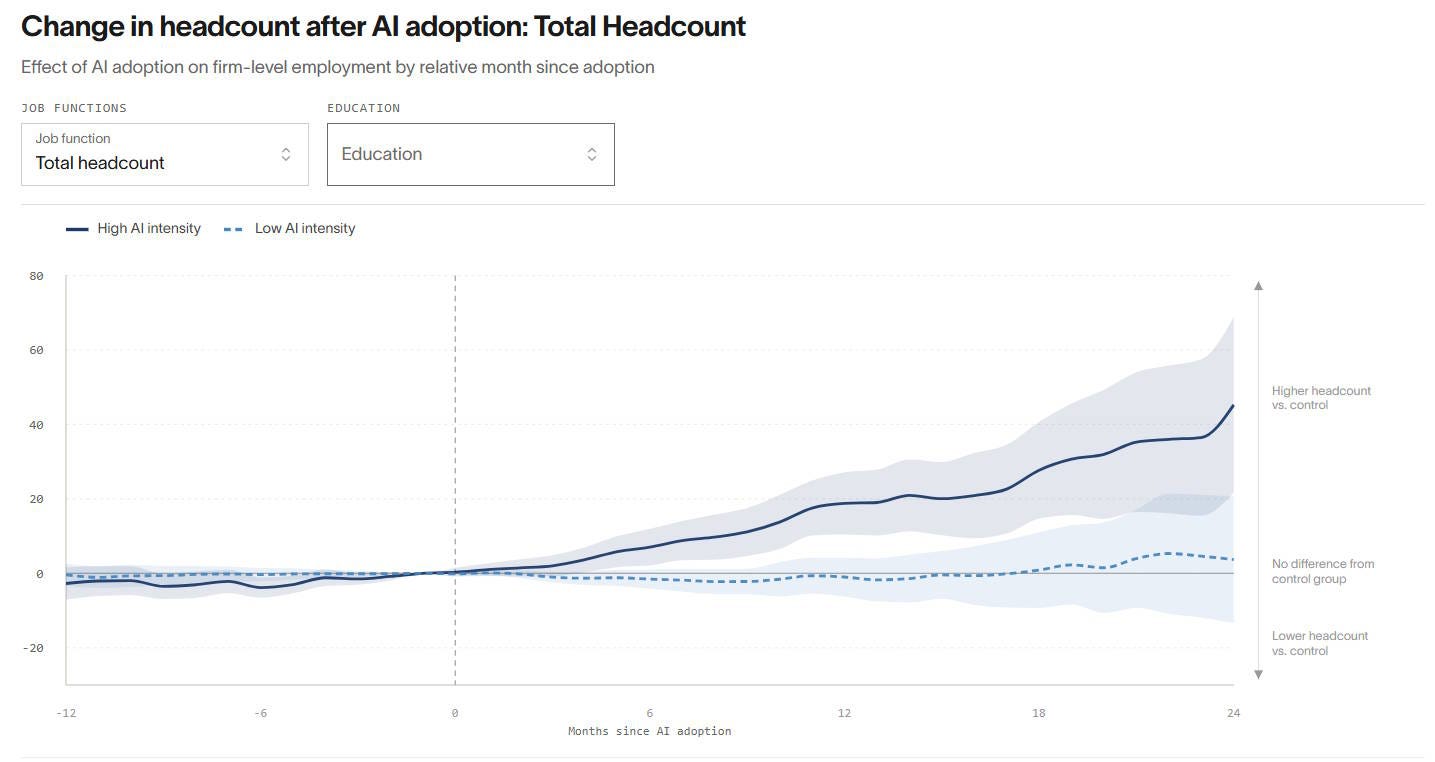

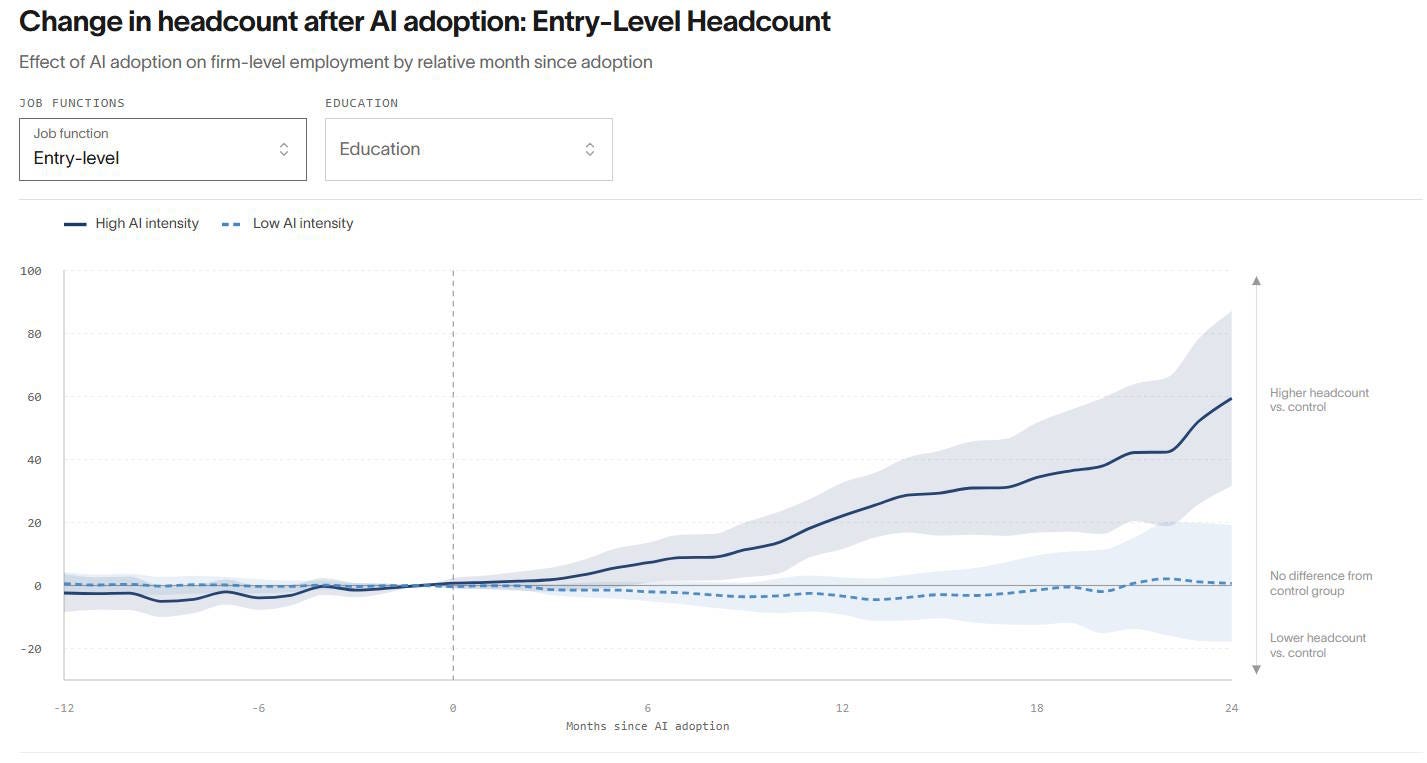

Everyone’s favorite subject (except for bears on bikes, of course) is AI taking jobs from humans. I’ve tried to use these roundups to keep abreast of the most recent evidence in this area. This week, we have a study by Kharazian, Simon, and Stevens using private data to examine what happens when companies start using generative AI.

The authors find that when companies start using generative AI, they hire more humans, not less:

It’s not just total headcount, though. Entry-level headcount rose too!

This flies in the face of the typical story that the current “no-hire, no-fire” economy is due to companies adopting AI instead of hiring entry-level workers.

That doesn’t mean that AI isn’t reducing job churn, of course. Uncertainty about how to use AI, or uncertainty about how AI might affect their industries, might be keeping companies from hiring new workers, even if they don’t adopt AI. That’s a research direction worth looking into, and basically no one’s talking about it.

Anyway, Kharazian wrote a blog post about the new findings:

The simplest story here is that AI is still mostly a complement to human labor rather than a substitute. That could change, of course, as the technology advances further. But for now, AI is behaving pretty much like a normal technology.

Basically, we want fewer bicycles, and more vertical short-form videos of bears riding bicycles.

For whatever it's worth, I've been trying to get a job all year and have had only a pile of rejection letters to show for it since January, the last time I managed to get an interview. And I have a Ph.D. in applied mathematics!

So at least as far as I can tell from where I am, the hiring market is still quite bad.