Why is the U.S. doing so much deficit spending?

And is this going to hurt us down the line?

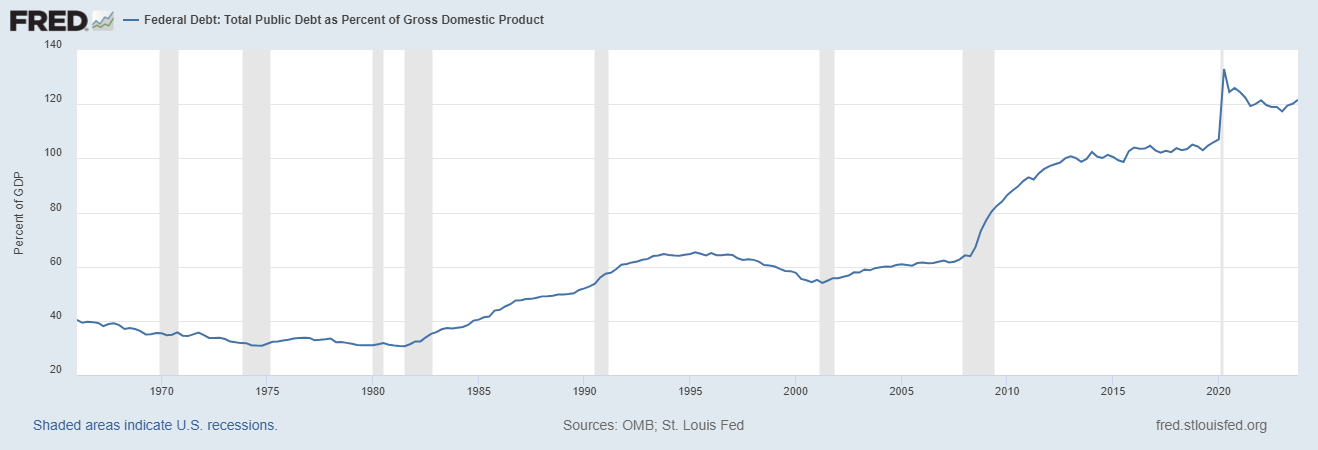

When I was a kid, the nation was in a collective freakout about the national debt — and the deficit, which is the amount the federal government adds to the national debt each year, although people tend to get “deficit” and “debt” mixed up. Either way, people were upset about it. We had that National Debt Clock, which was installed on the side of a building in New York City in 1989. In the 1992 election, the three candidates competed to portray themselves as deficit cutters — and to be honest, all of them were being pretty honest. Bill Clinton won, and the nation celebrated as his combination of spending cuts and tax hikes brought the nation back to a surplus by the end of the 1990s.

Why was the U.S. so austerity-minded in the early 1990s? The country had begun to run persistent budget deficits in the 70s, which had grown in the 80s as a result of Reagan’s tax cuts and defense buildup:

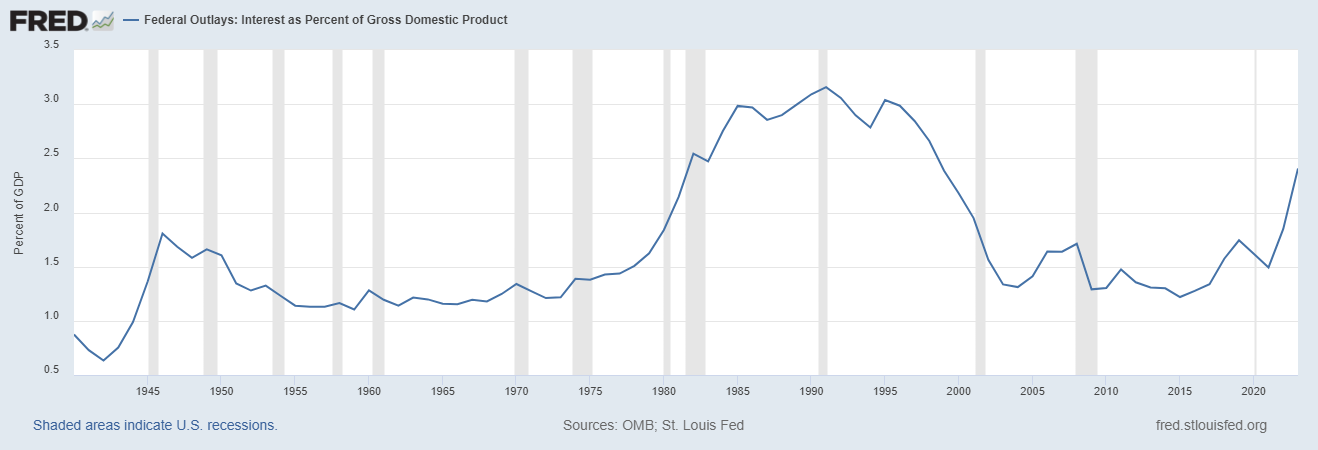

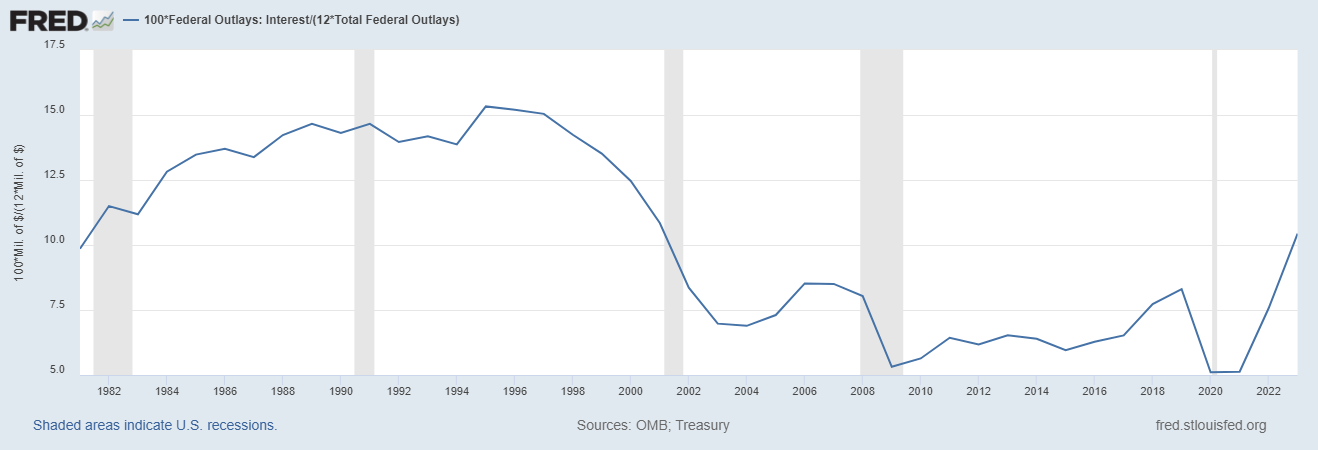

But that wasn’t the only reason. The government was also paying a fortune in interest on the national debt every year. The Fed had raised interest rates in the late 70s and early 80s to fight the inflation of the previous decade, and these higher rates meant that the U.S. national debt was suddenly more of an annual burden:

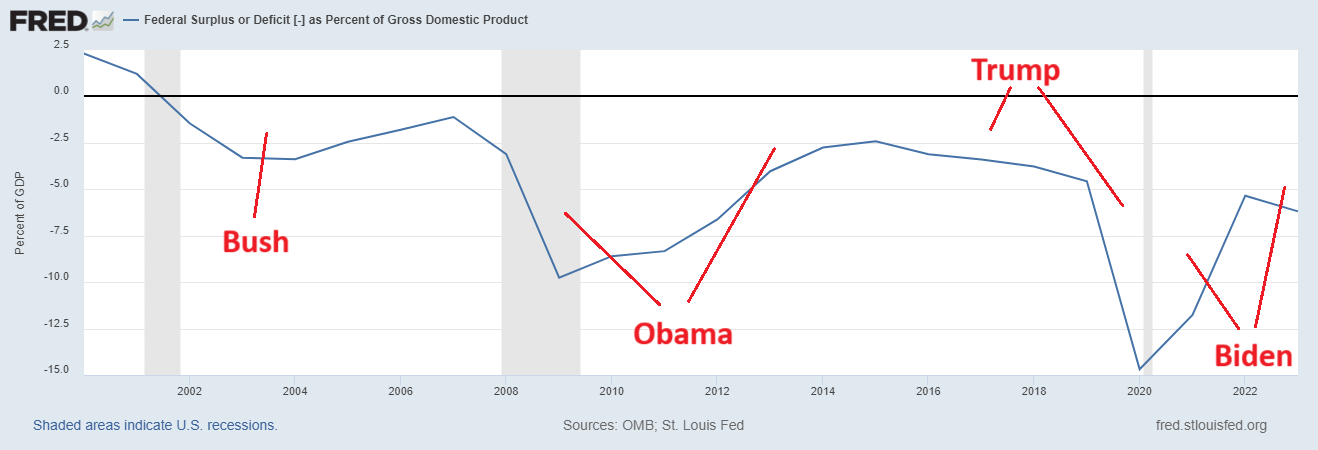

In the years after Clinton’s victory over deficits, the U.S. reversed course again. The federal government went into the red during the Bush years, mainly because of tax cuts. Obama then unleashed a massive stimulus to fight the Great Recession. With some pressure from the Tea Party Congress, Obama cut the deficit somewhat in his second term, but Trump started raising it again. Then Covid hit, and the U.S. did a massive amount of deficit spending to make sure it didn’t wipe out Americans’ finances.

Why was the U.S. so blasé about big deficits in 2002-2020, when we had freaked out so much over comparatively modest deficits in the early 90s? Part of it was that there were a bunch of emergencies that seemed to justify a temporary burst of deficit spending — 9/11, the financial crisis and Great Recession, and Covid. But a lot of it was simply due to the fact that interest rates were really low, so it was a lot easier for the government to carry a larger amount of debt. As you can see from the graph above, even though debt rose steadily in the 2000s and 2010s, interest payments stayed pretty low.

But over the last two years, something ominous has happened. Although the pandemic is long over, the economy is doing great, and interest rates have risen sharply, the U.S. federal government is still borrowing a ton of money. The deficit was over 5% of GDP in 2022, and increased to over 6% of GDP in 2023 — levels not seen since the Great Recession. Part of the increase from 2022 to 2023 appears to have been a one-off, driven by a stock bust and some strange timing of tax collections. But the 2022 deficit is still historically very large as a percent of GDP.

And it’s starting to cost us. As the graph above shows, interest costs on the debt are spiking — they’re not yet back to early 1990s levels, but they’re rising very fast.

So there are two questions here. First, why are we doing this? And second, when will this become a problem for our country? Unfortunately, there’s a huge amount of uncertainty around both of those questions, but it’s not too hard to come up with some scary theories.

What is the purpose of deficit spending in 2024?

Traditionally, the purpose of federal deficit spending is either to buy something we need — the interstate highway system, World War 2 weapons, a bank bailout, etc. — or to counteract an economic downturn like the Great Depression or the Great Recession. The second of these purposes is called “fiscal policy”, “stimulus”, or “fiscal stimulus”. It’s also sometimes called “Keynesian policy” or “Keynesian stimulus”, because it was the economist John Maynard Keynes who thought of the idea. The basic rationale behind stimulus is that when the economy has a lack of aggregate demand — usually due to a financial crisis — the government can step in and fill the gap with deficit spending. Deficit spending raises aggregate demand. (Monetary policy can also raise aggregate demand, but sometimes that’s not enough, such as when interest rates hit zero and can’t go any lower.)

It’s not necessarily the case that either one of these is the rationale behind America’s current deficit spending — because it’s not clear there’s a rationale at all. It might simply be the case that the U.S. government is moved by a variety of interests, and some of those interests favor high spending, and some favor low taxes, and that neither one really thinks about the deficit as such.

But it seems likely that someone in the Biden administration is keeping an eye on the deficit, and they must be aware of the rapid rise in interest costs, since they’re responsible for submitting a budget. And yet we don’t really see the administration sounding the alarm or pivoting to austerity like Bill Clinton did in the early 1990s. Thus it makes sense to ask why the Biden administration is tolerating, or even encouraging, high deficits.

Part of the reason is industrial policy. The IRA and the CHIPS Act together represent a pretty dramatic economic policy pivot, and that pivot is going to cost money, in the form of construction subsidies, government purchases of factory outputs, research expenditures, education and training, etc. If we expect those investments to bear economic dividends in the future, it makes sense to borrow to fund them today — just like a company borrows money to build a factory today in the hopes of making a profit over the next decade. Very much like that, in fact.

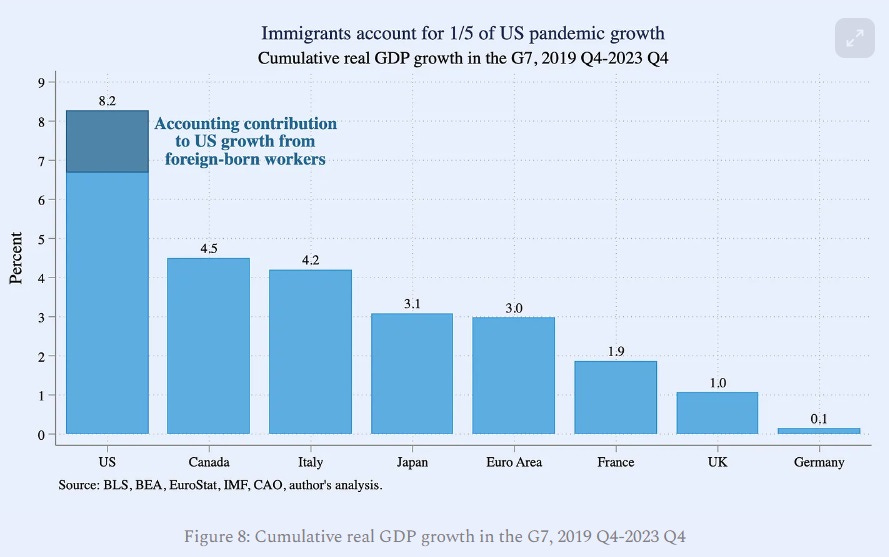

But I think a big part of the motivation for deficit spending is fiscal stimulus. Basically, unemployment is very low right now, GDP growth is fairly rapid, and the stock market is doing great. Compared to the time before the pandemic struck, the U.S. has grown much faster than other major economies, even after accounting for higher immigration:

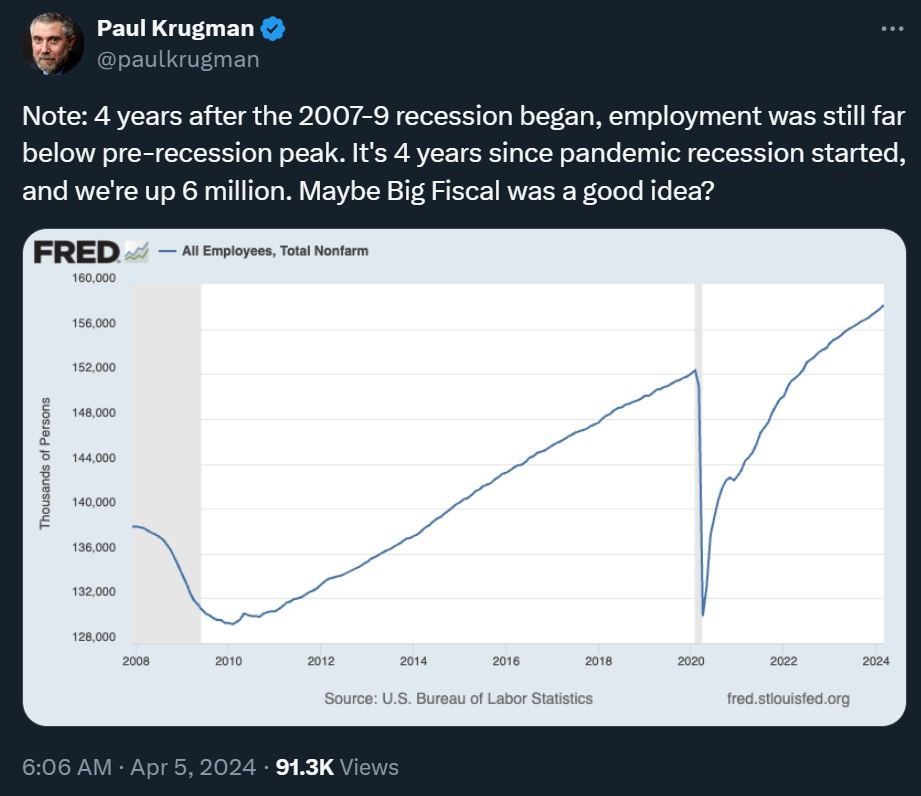

It’s understandable that the administration would want to keep that performance going. America’s big fiscal deficits are only one of many possible contributors to its outperformance, but economists who lean toward the progressive side of the aisle — from which the Biden administration mostly draws its economic team — have taken to giving fiscal policy much of the credit for fast growth and low unemployment. They’ve taken to calling deficits “Big Fiscal”:

As a side note, I think this explanation is likely overdone. The Covid shock simply wasn’t that similar in nature to the Great Recession — it didn’t involve a financial crisis or a large overhang of debt, and thus there wasn’t as much reason to expect the hangover to last nearly as long as it did after 2008, Big Fiscal or no. In fact, when I interviewed Paul Krugman for Bloomberg in 2020, he said as much, arguing that aggregate demand was the wrong framework for thinking about the Covid recession. But he now appears to have shifted his outlook.

In any case, lots of progressive economic commentators repeat the line “Thank you, Big Fiscal” when discussing the strength of the U.S. economy. And it seems likely that behind the closed doors of the Biden administration, many of the progressive economists that Biden has tapped for economic advice are saying much the same.

And in an election year, the administration’s economic team seems especially unlikely to take their foot off the proverbial gas. Easing up on Big Fiscal could risk sparking a recession just as the threat of a second Trump administration looms large. Jimmy Carter, after all, may have been finally doomed by an election-year recession in 1980. Even if there are some officials in the administration who want to pivot to austerity, they’re probably going to wait until after Biden is (hopefully) reelected.

(As for why the GOP Congress is letting Big Fiscal have its way, I can’t say; perhaps they simply realized that fighting deficits tooth and nail with government shutdowns and debt ceiling brinksmanship is a losing battle for them. Or perhaps the GOP’s seeming lack of concern for deficits under the Trump, Bush, and Reagan administrations has now simply become permanent.)

In other words, the U.S. is continuing to run big deficits because things seem to be going well right now, and cutting the deficit is risky and scary. The next question is whether or not this represents a wise choice, or shortsighted behavior that will come back to bite us.

When will the national debt become a problem?

Deficits are only a problem inasmuch as they add to the national debt. And it’s worth noting that the national debt actually shrank as a percentage of GDP in 2021 and 2022, despite all that deficit spending:

Why? Because of inflation. Inflation increases the dollar amount of GDP (and of tax revenues), but it doesn’t increase the dollar amount of government debt. So when you have rapid inflation, one happy side effect is that it shrinks the national debt in real terms (or relative to GDP, as I’ve shown here).

But now that inflation has fallen to around 3%, the debt is growing again. If that continues indefinitely, at some point it’ll become a problem. Basically, there are three possible problems that can result from high government debt:

interest costs

crowding out of private investment

inflation

We’re already starting to see the first of these. Interest costs are rising quickly as a percentage of GDP, and also as a percentage of total federal government spending:

When the federal government has to make higher interest payments on its debt, it can do three things. It can raise taxes (which the U.S. is not doing). It can cut spending on other items, essentially letting interests costs crowd out the rest of the budget (which the U.S. also is not doing). Or it can borrow even more to cover the interest payments. This is what the U.S. is now doing.

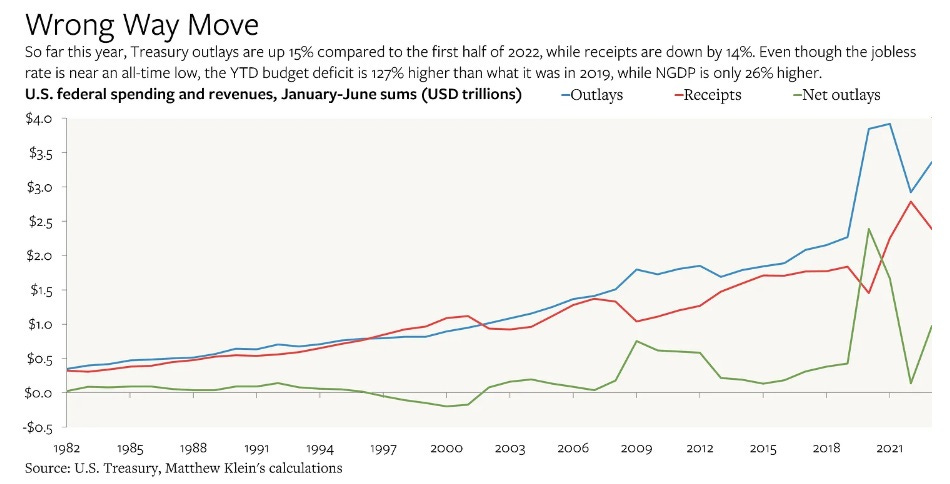

Matt C. Klein has an excellent post that walks us through the various components of taxes and spending. He shows that the increasing deficit is partly due to one-off decreases in tax collection, but that much of it is driven by increased government spending:

He shows that “the increase in outlays is almost entirely attributable to the surge in interest payments on Treasury debt.”

So right now, the U.S. is going on a borrowing binge to cover the increased interest on its previous borrowing binges. You can only do this for so long, before other bad things start to happen. Eventually, investors are going to start getting nervous about a sovereign default, and they’re going to start charging a default premium on U.S. government debt — in other words, interest rates will go up even more. Higher rates will crowd out private investment; instead of aggregate demand being stimulated, it’ll be crushed, and the economy and jobs will suffer.

It will raise U.S. government interest costs even more. And then if the government keeps borrowing at an exponentially faster rate to pay those interest costs, the whole thing just spirals, private banks stop buying government debt, the Fed has to step in, and eventually you get hyperinflation and the whole economy basically collapses. I explained the mechanics of this in a post three years ago:

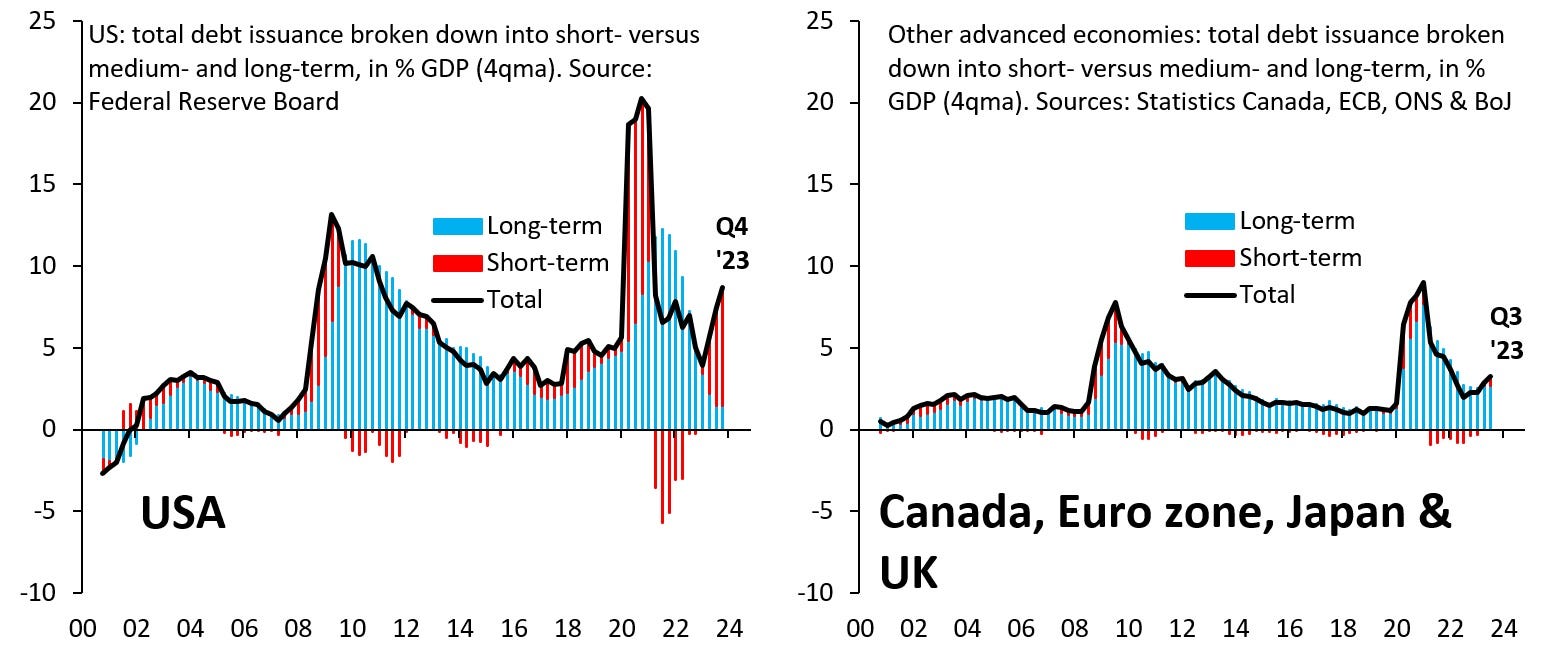

So…uh…that’s bad. But it’s also a doomsday scenario. The U.S. government appears to be betting that the surge in interest costs is a temporary phenomenon. How do we know that? Because the U.S. government is borrowing almost entirely short-term debt right now, instead of long-term debt:

This means the Treasury expects interest rates to go down very soon. If rates go down, the U.S. government will be able to roll over its short-term debt almost immediately, and bring interest costs down very quickly. So all this short-term borrowing is a bet on rate cuts.

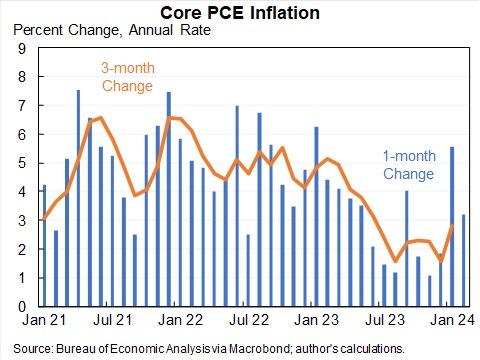

But what if rate cuts…don’t happen soon? Two months ago I thought it looked likely that the Fed would start cutting soon, as did most financial market participants. But that was always predicated on inflation staying low. And in the last two months it has started to rise again:

If inflation stubbornly refuses to stay near the 2% target, the Fed will not cut interest rates, and the government’s fiscal problem will get rapidly worse. We will quickly return to the same level of interest costs as the early 1990s, and at that point the government will start facing some difficult and painful fiscal choices.

What if Big Fiscal is causing inflation?

There’s also another unsettling possibility: deficit spending might be causing inflation to stay above target.

Even if a government’s fiscal position never spirals into hyperinflation, it’s theoretically possible that deficits can be inflationary. In fact, this is how a typical New Keynesian macro model works. It’s also implied by a theory called the Fiscal Theory of the Price Level. So it might be the case that the U.S. government’s big deficits might be causing inflation to remain stubbornly above target.

Now, “possible” doesn’t mean “true”. Those theories are just theories, and none of them has incredibly good empirical support — FTPL, for example, sometimes gets laughed at because it seems like it would have predicted runaway inflation in Japan during that country’s unprecedented government borrowing binge, when what actually happened was deflation.

The Biden administration, for its part, doesn’t seem to be worrying much that its fiscal policies are part of the inflation problem. It seems to have embraced the heterodox idea that corporate power and price-gouging are the main culprit, rather than good old aggregate demand. This would imply that what the President needs to do in order to help the Fed fight inflation is to jawbone companies into lowering prices, take stronger antitrust action, and perhaps implement some kind of price controls.

But if the administration is wrong, and fiscal policy is stimulating inflation, then Big Fiscal could backfire on Biden pretty badly. Americans hate unemployment, but surveys pretty consistently show that they hate inflation even more. And if inflation stays high, it’ll force the Fed to delay rate cuts. There’s some evidence that high interest rates are another force that’s weighing down consumer sentiment. So continued above-target inflation and the resultant continued high interest rates could create a double electoral whammy for Biden.

Big Fiscal thus represents a risky bet. It’s a bet that avoiding even a small rise in unemployment at all costs is worth the risk of potentially keeping both inflation and interest rates uncomfortably high. I don’t know where the correct balance of risk lies, but I worry that progressives over-learned the lessons of the Great Recession. Unemployment isn’t the only thing that makes American voters mad.

In any case, I think that after the election, we’re likely to see increased concern about the federal deficit — no matter who wins. Even if rates do get cut, it seems unlikely they’ll soon return to the near-zero level of the 2010s. 3% rates would likely still be high enough to force uncomfortable fiscal decisions on Congress and the President, given how much debt the government has built up since the days of Bill Clinton. An Age of Austerity — or at least, unpleasant political battles over austerity — is probably on the way.

Isn’t the answer to tax billionaires and multi millionaire?

I've always been sceptical about the idea that borrowing is fine as long as interest rates remain low. Because those interest rates don't remain low forever. I think you alluded to people getting confused between debt and deficit, and this is prime example; interest is paid on the former, not the latter. If you borrow heavily during periods of low interest rates, you can't just stop the borrowing when interest rates climb; you have to pay the interest on that accumulated debt.

In the UK, we spend more on servicing our debt than we do on education. And it's because our debt ballooned after the Great Recession while our economy has barely grown at all. We are now stuck in a fiscal trap.