An Age of Austerity is probably on the way

It's not the 2010s anymore.

I still remember watching the 1992 presidential election as a kid — the first election I was really aware of. The biggest issue was the federal budget deficit; Bill Clinton and independent candidate Ross Perot were demanding fiscal austerity after 18 years of persistent government borrowing. Incumbent George H.W. Bush lamely called the Democrats the party of tax-and-spend, but his protests rang a bit hollow after 12 years of don’t-tax-but-spend-anyway (Bush had tried raising taxes, but faced a revolt from within his own party). In the end, Clinton won, and enacted an austerity budget in 1993 that raised taxes and cut spending, and by the end of the decade the federal budget was in surplus. Most of the country and the national news media hailed this as a great victory. Progressive economists who worked for the Clinton administration, such as my podcast co-host Brad DeLong, argued that austerity lowered long-term interest rates and helped fuel the economic boom of the 90s.

It’s pretty crazy to think back to a time when austerity was such a popular policy. By the early 2020s, popular thinking had undergone a dramatic reversal. The Great Recession made “austerity” a dirty word. When we say “austerity” now, we think of the huffy Germans who deepened the Eurozone crisis by refusing to bail out Greece, or the misguided conservatives who railed against U.S. stimulus spending in 2009. More than a decade spent in a liquidity trap, where austerity only compounded the shortfall in aggregate demand, taught many of us that government deficits are something to be welcomed rather than feared. And when Covid came around, we applied that lesson, taking out unprecedented amounts of government debt in order to protect people and businesses from economic ruin in 2020 and 2021. The strong recovery that began in 2021 seems to vindicate that decision. Big Deficit won the day.

But what changed once can change again. And there are two big reasons to think that the Age of Stimulus we’ve been living in since 2008 is going to give way to a new Age of Austerity fairly soon. These reasons are 1) higher interest rates, and 2) the aging of the U.S. population.

Borrowing isn’t free anymore

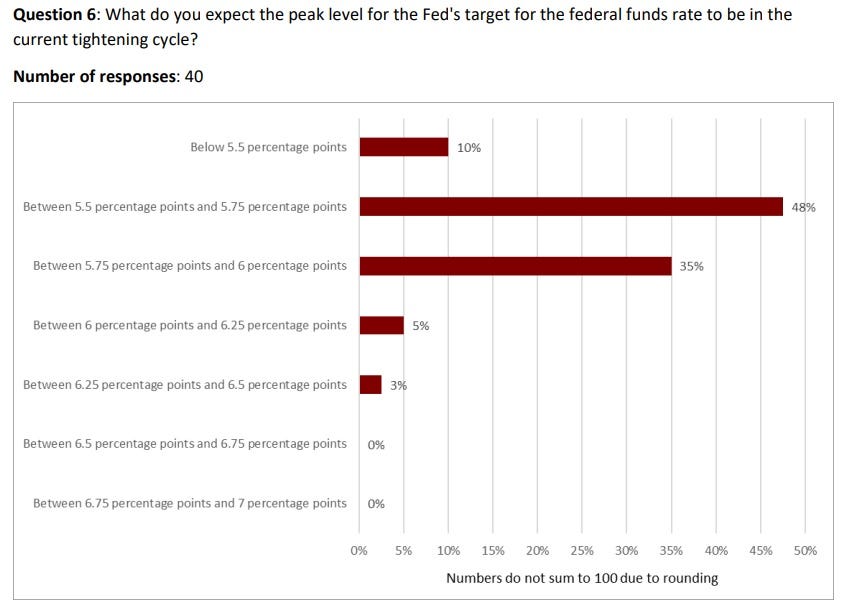

Interest rates are the most immediate worry. The Fed has raised rates from around 0% to over 5% in order to combat the post-pandemic inflation. That’s starting to raise the interest costs that the federal government has to pay on its debt every quarter:

Looking at this chart, you can pretty easily see why Americans wanted austerity back in 1992; interest payments were devouring a historically large percent of the federal budget. By the 2000s and 2010s, thanks to Clinton’s austerity, continued economic growth, and low interest rates, interest was much less of a burden.

Now the line is shooting up again, thanks to rate hikes. It’s not yet nearly as high as it was in 1992, because many of the bonds that the U.S. government is paying off were issued back when rates were low. But the average maturity of U.S. government debt is only a little over 6 years, meaning it has to be rolled over fairly frequently. So if rates don’t drop back to a low level very soon, we can expect the federal government’s interest costs to continue to rise steeply.

In fact, the line could go much higher than it was in 1992. The reason is that the federal government’s outstanding stock of debt is about twice as high now as it was then, relative to the size of the economy:

Notice that the line has been going down a little bit since the pandemic; that’s because inflation has been eroding the federal debt. But since inflation has come down, that accelerated erosion is mostly over. So a much bigger federal debt plus interest rates at mid-90s levels mean that interest costs could eat up a very big portion of the federal budget in just a couple of years.

The big question, of course, is whether rates will come down now that inflation seems to have mostly subsided. It’s possible that the Fed will keep rates high for a while, just to make sure inflation has been quelled. In fact, macroeconomists tend to think this is the likeliest possibility (and the Fed listens to macroeconomists and largely comes from the same academic background):

It’s also possible that the persistent threat of supply shocks from war and trade decoupling will cause the Fed to keep rates high for a long time. If rates don’t go down, interest costs will soar, and the federal government will come under enormous pressure to cut deficits or even start running surpluses like in the late 90s. In other words, austerity.

A rule of thumb for whether government borrowing is sustainable is whether the interest rate r is less than economic growth g. Intuitively, r is the rate at which the debt naturally grows, and g is the rate at which the tax base grows. If g > r, then you can run a deficit forever without increasing the ratio of debt to GDP, because you’re always growing out of your debt. But if r > g, you have to run a budget surplus in order to stop debt from growing as a share of GDP.

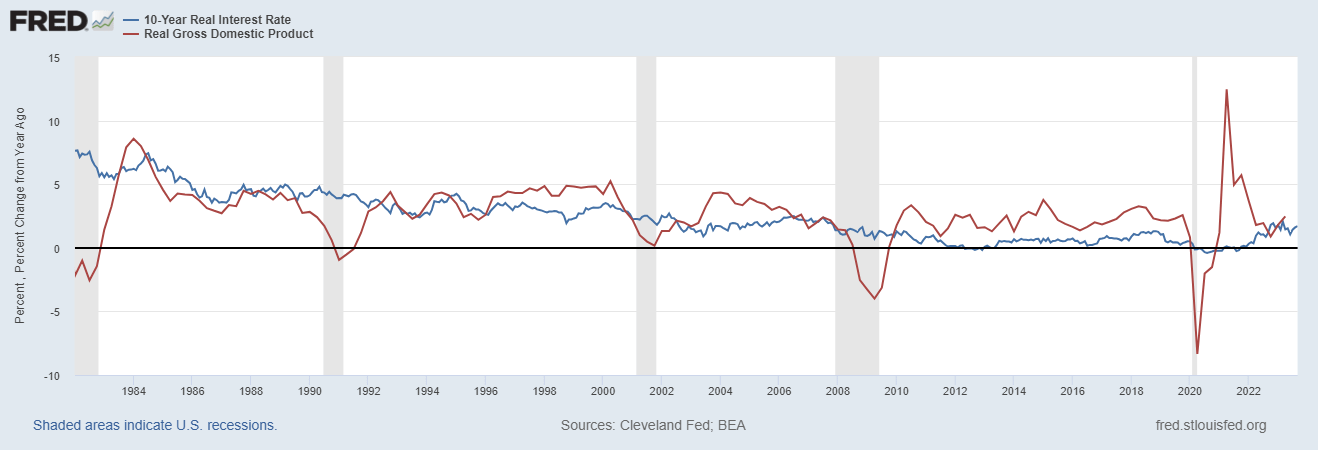

Now, growing the federal debt as a share of GDP isn’t necessarily the end of the world — after all, we’ve done it for half a century now, as have many other rich countries, and it hasn’t spelled economic doom. I’ll talk about that in a bit. But that simple rule of thumb — whether r is greater or less than g — can tell us a lot about whether a society is going to come under pressure to cut the government debt. Let’s compare the Cleveland Fed’s estimate of 10-year real interest rates to the U.S. real GDP growth rate:

You can see that in the Reagan and H.W. Bush years, real interest rates were above the rate of growth; the debt was becoming less sustainable. In the years leading up to the 1992 election, the gap was especially big. But the relationship flipped in Clinton’s second term thanks to a productivity boom. And even when that boom faded, r stayed below g throughout the W. Bush, Obama, and Trump years thanks to low interest rates. And during the Great Recession and the pandemic, when growth briefly dipped well below interest rates, increasing the debt-to-GDP ratio was considered an acceptable temporary expedient for getting the U.S. through a crisis. So perhaps it was no surprise that Americans were less concerned about government borrowing in the 2000s and 2010s than they had been in the early 90s.

But real interest rates have been creeping up, and now r and g are approximately equal, as they were in Clinton’s first term. We’re approaching the point where government debt is about to grow on its own even without federal budget deficits. And that will make it politically harder to run big deficits.

Aging means entitlements don’t pay for themselves anymore

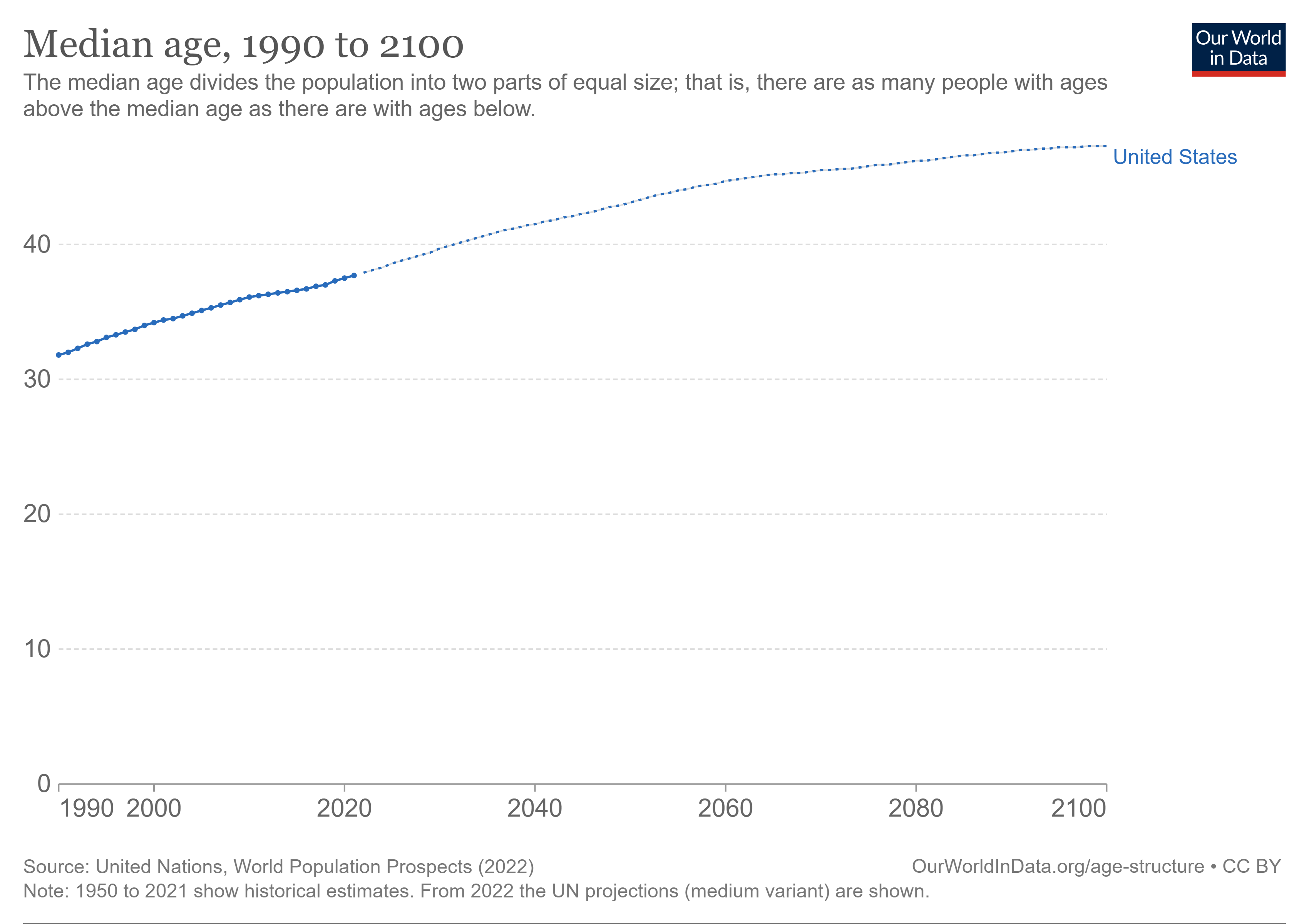

There is a second reason the federal budget will be under increasing pressure, and that’s that the U.S. is getting older:

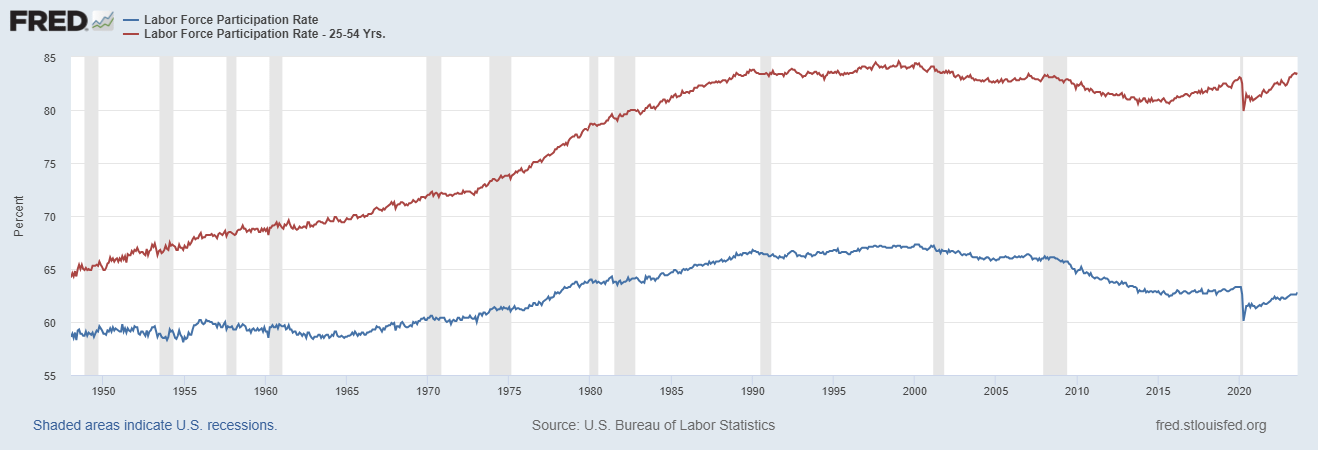

Another way to see this is to look at the difference between prime-age labor force participation rates, which are near record highs due to the strongest labor market in a generation, and total labor-force participation rates, which have fallen by about 5 percentage points due to the Boomer retirement:

And because of the recent fall in the fertility rate, this is only going to get worse over time.

This puts our entitlement system under pressure, because Social Security and Medicare both work via young working people paying payroll taxes to support the needs of the old.

For a long time, entitlements basically paid for themselves. When population is growing rapidly, programs like Social Security and Medicare are like sustainable Ponzi schemes — young working people pay into the system via taxes, and then during their retirement they get more out than they put in, because a new bigger crop of young people is now paying in. But when population growth slows down, this becomes less sustainable. Fewer young people to pay into the system, plus more people who depend on the system, means that we will either have to cut benefits, raise payroll taxes, or start paying Social Security benefits from general revenue.

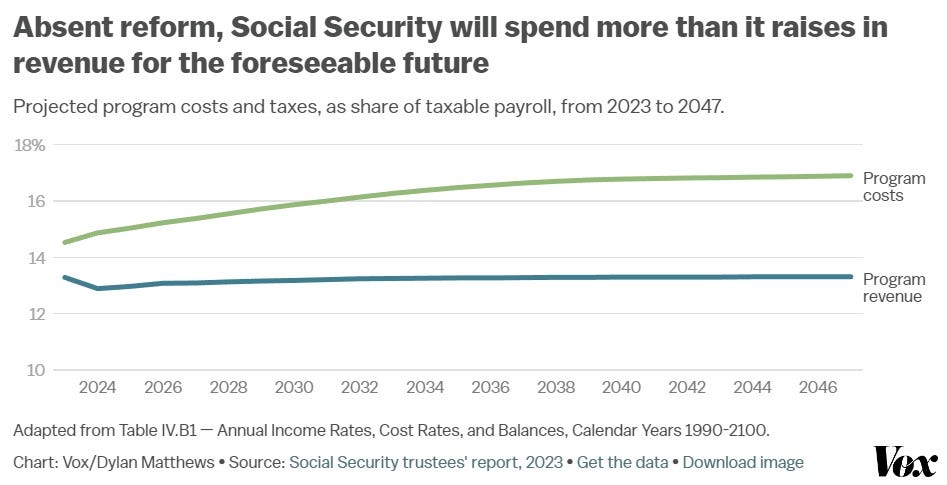

Fifteen years ago, Medicare was the big worry; Social Security was still a long way from being under pressure, while rising health care prices were raising Medicare spending rapidly. The good news here is that Medicare spending has basically flatlined since the early 2010s. The bad news is that Social Security is now much closer to the day when we’ll have to make some hard choices. Vox’s Dylan Matthews had a great post about this back in April:

The Congressional Budget Office projects the OASI fund, which funds old-age benefits, will run out of money in 2032; the Social Security trustees project this will happen in 2033. At that point, the program will only be able to pay out benefits based on the taxes it’s collecting — and it’ll be collecting about 20 percent less in taxes than it’s promising to pay out in benefits…

“The system is, in effect, projected to go off a cliff,” Paul Van de Water, a senior fellow at the Center on Budget and Policy Priorities who worked on the 1977 Social Security amendments in the Carter administration, told me. “There’s a much larger deficit in relative terms.”…This is not a temporary blip; the US’s low birth rates have fundamentally altered our demographic balance in a way that will make current taxes inadequate to pay promised benefits for the indefinite future.

And here is his chart:

Matthews states that we can deal with this either by cutting benefits or raising taxes — both of which are forms of austerity.

There’s a third option he doesn’t really discuss, which is to start paying Social Security from the government’s general revenue. This would allow the government to run deficits to fund Social Security benefits. But in an environment where interest rates are approximately equal to GDP growth rates, that will necessarily cause the federal debt to keep growing and growing.

What if we the government just keeps borrowing more and more forever?

It’s worth taking a moment to discuss the question of what happens if we just have the federal government keep borrowing more and more without regard to fiscal sustainability. If your debt grows and grows as a percent of GDP, so what? Interest costs might go up and up, but can’t you just borrow even more in order to fund those interest payments? Alternatively, can’t the Fed just buy a bunch of long-term Treasury bonds to keep interest rates at zero, so that interest costs never become a problem?

In fact, I wrote a post about this back in early 2021, explaining the sequence of events that happens if the government just ignores the idea that it has a borrowing constraint, and just keeps borrowing ever-increasing amounts for all eternity:

Basically, if the federal government does this, interest rates go up and up, because private and foreign lenders worry that this borrowing spree will eventually end in either sovereign default or hyperinflation. This leads to a spiral where the government needs to borrow even more. At some point runs out of people who are willing to lend it the amounts of money it needs, at any interest rate.

At that point either the government defaults, or the Fed has to step in. The Fed can lower interest rates to zero, or even fund government borrowing directly. In the 2010s, thanks to a persistent aggregate demand shortage from the financial crisis, we were able to keep rates at zero without sparking inflation. But at some point — no one knows when — keeping rates too low for too long will lead to spiraling prices. Most macroeconomists agree that hyperinflation is the endgame of runaway government borrowing. When this happens, it is swift and devastating; the result is wholesale economic collapse.

That would be very very bad. Of course, this doesn’t mean that any amount of borrowing that increases the debt-to-GDP ratio is putting us on a path to hyperinflationary ruin. Obviously, the U.S. has managed to increase its debt-to-GDP ratio fairly steadily since the early 1980s without running off an economic cliff, as have other advanced countries like Japan. But the more we bake continuous increases in the debt-to-GDP ratio into our long-term economic policies, the greater the risk of ruin becomes.

What an Age of Austerity will be like

I expect most Americans to start worrying about this risk well before we actually run off the cliff. Already, progressive writers like Annie Lowrey are starting to worry about deficits:

Whether America’s debt becomes unsustainable depends on dozens of factors…But there are trillions of reasons to be worried about the country’s financial situation now, and even more reasons to worry about Washington’s capacity to address it in the years to come. Yet nobody cares.

This is a near-perfect inversion of the situation during the Obama administration, when Washington was obsessed with the country’s finances at the wrong time for the wrong reasons…

The scariest thing is not the debt itself…It’s the government’s inability to do anything effective about it. Republicans keep taking the debt ceiling hostage while running up huge deficits themselves…Democrats are less hypocritical. Still, the Biden White House won’t raise taxes on “middle class” families, meaning the 99 percent of households making less than $400,000 a year.

If interest rates stay well above zero and productivity fails to experience a late-90s-like boom, expect more articles like this. As interest costs rise and start squeezing the rest of the budget, expect Democrats to call for higher taxes and Republicans to call for cuts to Medicaid and other social programs. Expect to see analyses from think tanks detailing all the wonky little ways we could restrain federal spending. In other words, expect somewhat of a return to the intellectual and political climate of 1992.

A new Age of Austerity will put pressure on progressive plans to transform the economy via industrial policy, as well as increasing welfare benefits. Jeff Stein, who leans strongly toward the progressive side of things, recently published an article warning about increasing deficits in 2023:

After the government’s record spending in 2020 and 2021 to combat the impact of covid-19, the deficit dropped…But rather than continue to fall to its pre-pandemic levels, the deficit then shot upward. Budget experts now project that it will probably rise to about $2 trillion…

Jason Furman, who served as a top economist in the Obama administration and is now an economics professor at Harvard, said the current jump in the deficit is only surpassed by “major crises,” such as World War II, the 2008 financial meltdown or the coronavirus pandemic…

“To see this in an economy with low unemployment is truly stunning. There’s never been anything like it,” Furman said. “A good and strong economy, with no new emergency spending — and yet a deficit like this. The fact that it is so big in one year makes you think it must be some weird freakish thing going on.”

A pro-austerity attitude will also put political constraints on the U.S. government’s ability to engage in a military buildup to deter China from starting a war in Asia. I’ve called for such a buildup, but I recognize how politically difficult it will be with higher interest rates and an aging population.

In other words, an age of austerity will force everyone in the country to tighten their belts and lower their expectations. The last 15 years pushed us to imagine what more the U.S. government could do if only it had the political will to open its purse-strings. Unless a productivity boom and/or a return to near-zero interest rates with low inflation saves us from having to make hard choices, the next 15 years will force us to curb our imaginations and put a damper on our fiscal dreams.

It all comes back to housing. Lower housing costs, give daycare support, and productivity will be boosted and fertility rates increased.

I'm a millennial in the northeast and people here wait to have kids until their mid 30s because daycare and housing is so expensive , so they want to feel financially secure before parenthood. It's a rational decision with bad implications for society.

Housing is literally a silver bullet for so many of the US' issues it's a bit weird it's only ever discussed at a local level. I believe other countries like Japan have national zoning laws and agencies to deal with those conflicts.

How about we finally require the wealthy to pay their fair share of taxes including upping the income level for Soc Sec taxes? How about we let these immigrants work and also allow them to work towards citizenship. Every immigrant or refugee who is allowed to have a job also pays into Soc Sec. Why are low tax rates for the wealthy still allowed and the working class are the only ones considered for tax hikes?