Three reasons the Federal Reserve is likely to cut interest rates soon

Any soft landing needs a little bounce.

At this point, there’s really no doubt that the U.S. economy has achieved a soft landing. Even at an incredibly low unemployment rate of 3.7%, the jobs numbers are still surging — payrolls increased by over 350,000 in January, beating expectations, and past numbers were revised upward. The prime-age employment rate — my favorite indicator of the labor market — ticked up to its pre-pandemic high of 80.6%:

And all this is happening while wages are accelerating. In nominal terms, average hourly earnings increased at an annualized rate of 6.6%, which is almost certain to be substantially above the rate of inflation:

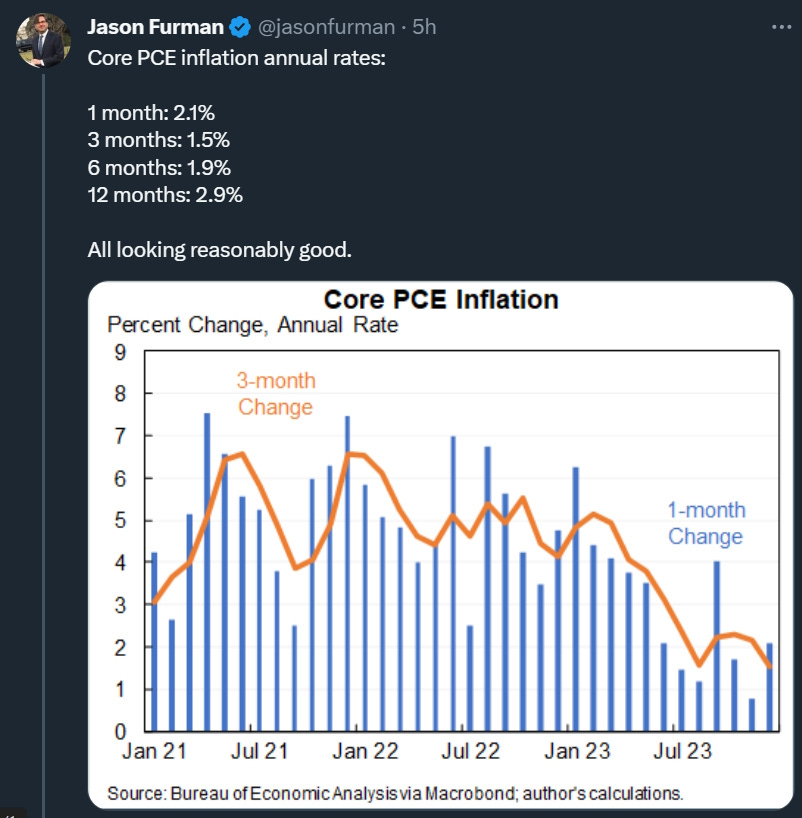

And yet at the same time, inflation has fallen back to the 2% target:

This is a remarkable macroeconomic feat. Very few people thought that the Fed would be able to quell the post-pandemic inflation without throwing large numbers of people out of work, but somehow they pulled it off.

The next big question is: Will the Fed cut rates this year? Great fortunes could hang on that decision, as could the short-term fate of the U.S. economy. But the answer is surprisingly unclear. Jerome Powell recently downplayed the likelihood of a March cut:

Jerome Powell delivered a clear message to traders eager for the central bank to start slashing interest rates: Not so fast…Powell forcefully pushed back on hopes of a first move at the next meeting in March — saying it’s unlikely to act that quickly as it waits for more signs that inflation is pulling consistently back to its target.

The obvious reason not to cut rates soon is that the economy is doing so well. Standard macroeconomic intuition says that when everybody has a job and wages are going up, people are going to buy more stuff, which is going to put upward pressure on prices eventually. So one basic strategy for monetary policy is to lean against a strong economy.

On top of that, there’s just the general intuition of “if it ain’t broke, don’t fix it.” If 5.33% interest rates haven’t hurt the real economy so far, and if they’ve managed to bring inflation back down to target, why would you rock the boat by going back to low interest rates?

That being said, I do think it’s likely that the Fed will start cutting rates fairly soon, if not in March then sometime in the three months afterward. There are basically three reasons why it makes sense. First of all, and most optimistically, we have what appears to be accelerating productivity growth.

Productivity growth looks like it’s accelerating

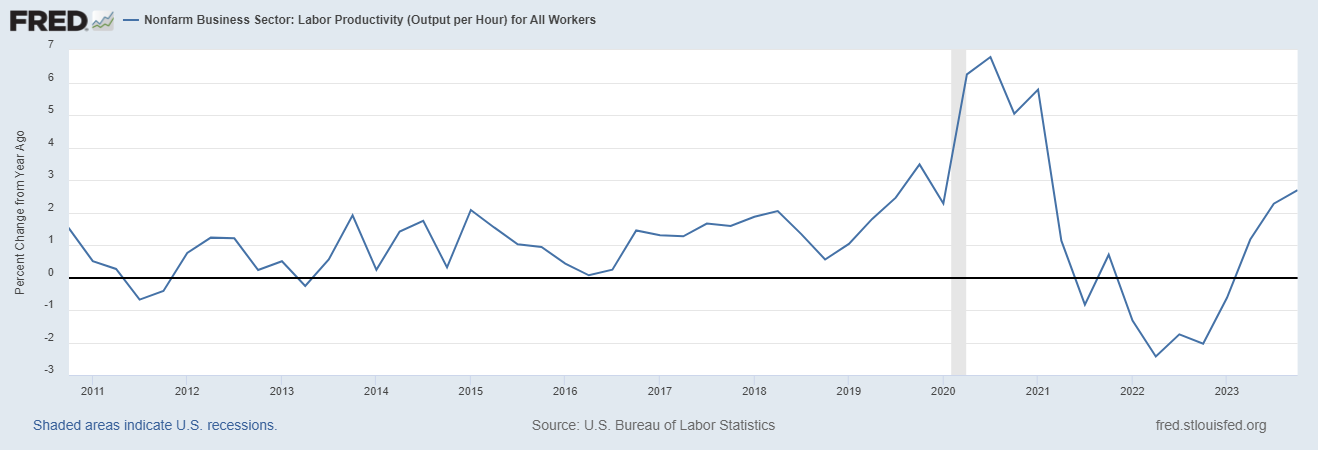

The simplest measure of productivity growth over the short term is labor productivity — total economic output per hour worked, adjusted for inflation. This comes out quarterly, so the most recent data we have is for the last three months of 2023. Here’s the year-over-year growth rate of labor productivity:

As you can see, the growth rate has been positive and rising over the last nine months. It was 2.7% in the most recent quarter, which as you can see is pretty high for the pre-pandemic period.

As an aside, that huge spike during and after Covid, but this was mostly a composition effect — tons of low-wage workers got laid off, making it look like productivity surged. The problem with using labor productivity as a measure is that it gets distorted by recessions.

Anyway, to see labor productivity rising when the economy is booming is very good. It’s not a composition effect. It represents real improvements in technology, business models, policy, trade, and all the other stuff that we want to see improve.

Rapid productivity growth gives the Fed room to cut interest rates. The reason is pretty simple: productivity growth is an inherently deflationary force. It means more stuff is getting produced, which tends to push prices down. The Fed can counteract that by cutting interest rates, which provides positive price pressure, and thus maintains price stability.

Another way to put this is that rapid productivity growth is a positive shock to aggregate supply. The Fed should keep aggregate demand growing at the same rate as aggregate supply, in order to keep the economy in balance. And the way you raise the growth rate of aggregate demand is by cutting interest rates.

A third way to put this is that productivity growth makes wage growth “safer” from a macroeconomic standpoint. During inflationary episodes, economists often worry that rapidly rising wages will increase costs for companies, forcing them to raise prices, which will make employees demand higher wages in order to pay the higher prices, and so on. This is called a “wage-price spiral”. We didn’t see anything like this during the recent bout of inflation — real wages actually fell. But economists tend to worry about this anyway.

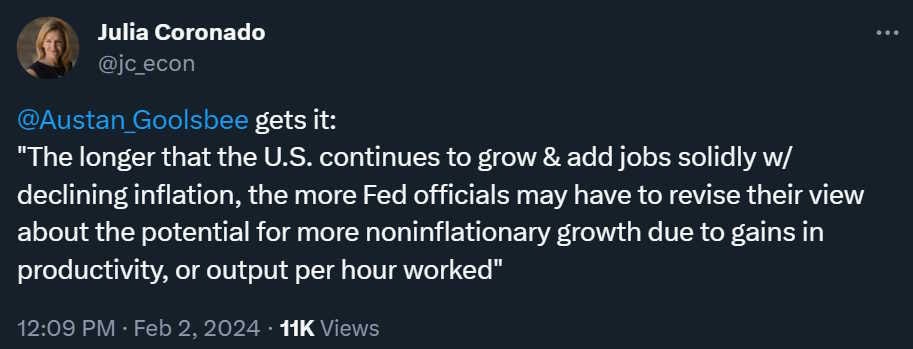

Fast productivity growth means that they don’t have to worry. Higher productivity “justifies” the higher wages in some sense; it means that the cost of producing each unit of output isn’t rising. So the fact that productivity growth is high right now will tend to neutralize the Fed’s worries about rising wages, and maybe its worries about fast growth in general:

In fact, many economists think that Alan Greenspan’s big success as Fed chair in the 1990s was that he kept rates low; he realized that a tech boom had increased productivity growth, and so lowering rates beyond what had prevailed in the 1980s was safe. Some blame this choice for the dot-com bubble, but I don’t think many people would go back and sacrifice the growth of the 1990s just to prevent the stock crash of 2000.

So Powell may now be looking at a situation a bit like Greenspan’s in the mid-90s.

Keeping rates high for a long time increases financial risks

Bringing down inflation without tanking the real economy was an incredible macroeconomic feat. But that success could be in jeopardy if leaving rates high for too long causes a financial crisis and a recession.

Many observers believe that the biggest danger to the real economy is the commercial property sector. Office buildings are already losing some of their value due to the rise of remote work. This puts a lot of businesses at risk — developers who build and renovate the buildings, leasing companies, businesses who own their own office buildings, and so on.

High interest rates are a double whammy for many of these businesses. Real estate companies tend to be highly leveraged — when they have to pay much higher borrowing costs, they tend to go out of business. Many of these companies issued their bonds back when rates were low, before 2022, so they’re safe for now — they’re still paying those low rates. But the longer rates stay high, the more of that debt has to be rolled over at the newer, higher rate.

So the longer the Fed keeps rates high, the more real estate companies will go bankrupt.

The real danger here is that a wave of defaults by dying real-estate companies will hurt the banking system, causing damage to the real economy — basically, a smaller version of 2008. Banks tend to lend to real estate companies a lot, so they’re very exposed here. Already, the commercial property sector is causing major headaches for some banks:

The US commercial real estate market has been in turmoil since the onset of the Covid-19 pandemic. But New York Community Bancorp and Japan’s Aozora Bank Ltd. delivered a reminder that some lenders are only just beginning to feel the pain.

New York Community Bancorp’s decisions to slash its dividend and stockpile reserves sent its stock down…The selling bled overnight into Europe and Asia, where Tokyo-based Aozora plunged more than 20% after warning of US commercial-property losses and Frankfurt’s Deutsche Bank AG more than quadrupled its US real estate loss provisions…

Banks are facing roughly $560 billion in commercial real estate maturities by the end of 2025, according to commercial real estate data provider Trepp, representing more than half of the total property debt coming due over that period. Regional lenders in particular are more exposed to the industry, and stand to be hit harder than their larger peers because they lack the large credit card portfolios or investment-banking businesses that can insulate them…Commercial real estate loans account for 28.7% of assets at small banks, compared with just 6.5% at bigger lenders[.]

The longer the Fed keeps rates high, the greater the chance of a financial crisis, in which large numbers of small and medium-sized regional U.S. banks go bust. Unlike last year, when the government secured deposits at troubled mid-sized banks and thus prevented a crisis, the only way to save small banks in the event of a wave of commercial property defaults would be large-scale bailouts like the ones in 2009-10. But even that would likely not be enough to protect the real economy from a recession, as previous experience demonstrates.

If this happens, it will put an end to the euphoria over the Fed’s successful soft landing. In fact, it will then have been a hard landing. Economists will say that disinflations are never costless — that eventually, you always get a recession. Pundits will question whether the Fed should have raised rates in the first place, or simply waited for inflation to go away on its own. And so on.

But if the Fed cuts rates before most of the outstanding low-interest commercial property debt matures, the companies will be saved from death-by-refinancing. Remote work may still cause some defaults, but the risk of a systemic financial crisis will be much reduced.

Markets are expecting a cut

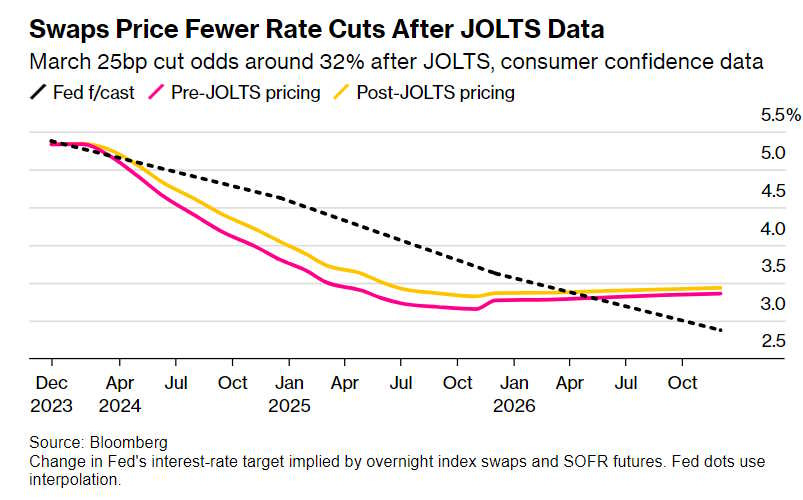

The third big reason for the Fed to cut rates is that markets and businesses are expecting them to do so. Even after Powell’s recent comments, markets expect the Fed to cut rates substantially starting in the spring:

In fact, markets expect the Fed to start cutting even faster than the Fed’s own forecast predicts.

Why should this influence the Fed’s actual policy? Because some part of the current economic boom may be due to these expectations of Fed cuts. Businesses may have made big investments on the assumption that they’d be able to roll over their debt more cheaply in one or two years.

If those assumptions prove false — if the Fed keeps rates higher for longer than markets expect them to — it could cause more businesses to go bust, and thus trigger weakness in the real economy. We could thus end up turning a soft landing into a hard landing.

What about politics?

There are at least two other reasons for the Fed to cut, and they both involve politics.

First, there’s fiscal dominance. When interest rates stay high for a long time, the federal government has to use a lot more of its budget to pay down the interest on the national debt. This is already happening:

This tends to crowd out other spending priorities, as it did in the early 1990s when people were obsessed with austerity. In order to prevent that, the Fed might want to lower interest rates, so the government can refinance the debt cheaply.

The other political factor is Donald Trump, who looks to have a decent chance of getting elected in November. Trump has repeatedly threatened the Federal Reserve’s independence. The Fed values its independence very, very highly. So some (including Trump himself) have suggested that the Fed might cut rates soon in order to keep the economy humming, in order to maximize Biden’s reelection chances. Here’s what John Authers wrote back in December:

If there’s one risk that clouds all others at present, it can be expressed in one word: “Trump.”…Powell needs to defend the Fed’s viability as an institution…Faced with the growing probability of a second Trump presidency, and heading an institution whose legitimacy is also under attack, Powell has a problem…

The risk of “higher for longer,”…is that it could prompt a deterioration in the economy heading into the election and sink Biden’s chances. If this were to happen, he said, “Former President Trump is most likely to be elected president and will have an opportunity to remake the Fed truly in his image this time, which could damage the institution’s credibility more than Powell would have by lowering rates into the presidential campaign.” In the first term, Trump’s nominations of radicals such as Judy Shelton, who favors a return to the gold standard, foundered in the Senate. That’s much less likely in a sequel.

In fact, I think both of these theories are pretty overblown, for the same reason: the incredibly high value that the Fed puts on its independence as an institution. Right now, Trump is going around yelling that Powell is going to cut rates just to sink his reelection. All else equal, that will make the Fed warier of cutting rates, in order not to validate the rumor. On balance, I think that concern probably cancels out the concern that Trump would revoke the Fed’s independence if elected.

As for fiscal dominance, I think that unless the U.S. is in danger of a sovereign default, the Fed won’t use low rates as a way to bail out congressional overspending. Setting that precedent would yoke the Fed to Congress’ spending decisions, effectively compromising the institution’s independence.

So while I think the Fed will start cutting rates pretty soon, I highly doubt that political considerations are going to be a factor in the decision. Instead, I think it just comes down to the fact that A) keeping rates at the current level for a long time increases the danger of a recession, and B) fast productivity growth makes it less likely that rate cuts will lead to inflation. When the risk of keeping rates persistently high clearly outweighs the risk of potentially cutting too early, the decision becomes an easy one.

I guess I'm in the "If it ain't broke, don't fix it" camp. I'm biased because I'm retired, love getting 5% money market rates, and do not have a mortgage. I certainly will not cry a river over real estate developers going bankrupt. They have made a fortune over the past several years, fueled by the low interest rates. If they are so leveraged they cannot function with the current rates, they probably deserve to go out of business. The biggest problem in our economy right now are home prices. Low mortgage rates will just cause another boom that will make home prices even higher, especially in popular locations. People focus too much on interest rates, and forget that the principal is what drives your mortgage payments.

Workers shifted to more productive work during the pandemic. All-time record new-business formation occurred in 2020 and 2021. Fed policy aside, I give most of the credit to American citizens who met the pandemic challenge. Of course, Larry Summers said millions would need to lose jobs to reduce inflation. Summers also declared Bidenomics “the biggest economic policy in 50 years.”

I think when the history of this period is written, the coin-operated Congress missed a rare opportunity to take advantage of real interest rates at zero. Congress’ stupid, petty culture wars were more important because, as always, our elected leaders were laser-focused on raising PAC money for their re-election campaigns. American citizens are of secondary importance to the Congressional clown car.

The Fed will best be served when it ignore Trump. In fact, Trump fatigue will turn off more voters outside the Banana Republican base (maybe 30%, at best). Trump has ridden the Republican Party to three consecutive election-cycle losses, a strong trend the mainstream media likes to ignore because it doesn’t see advertising. The trend isn’t Trump’s and the mainstream media’s friend. Twenty million first-time Gen Z voters, let alone Gens X and Y will show Trump the door in November. Hundreds of anti-MAGA organizers are networking via Zoom. Trump gets beat by high single digits. He will start whining “this election is fixed” by mid-summer. His strategy is to bully and threatened with violence voters at the polling stations. It didn’t work last time. And it won’t work in 2024. Time to turn the page once again on the temporary aberration of Agent Orange.