Inflation is forgetting

When dollars shrink, so do debts.

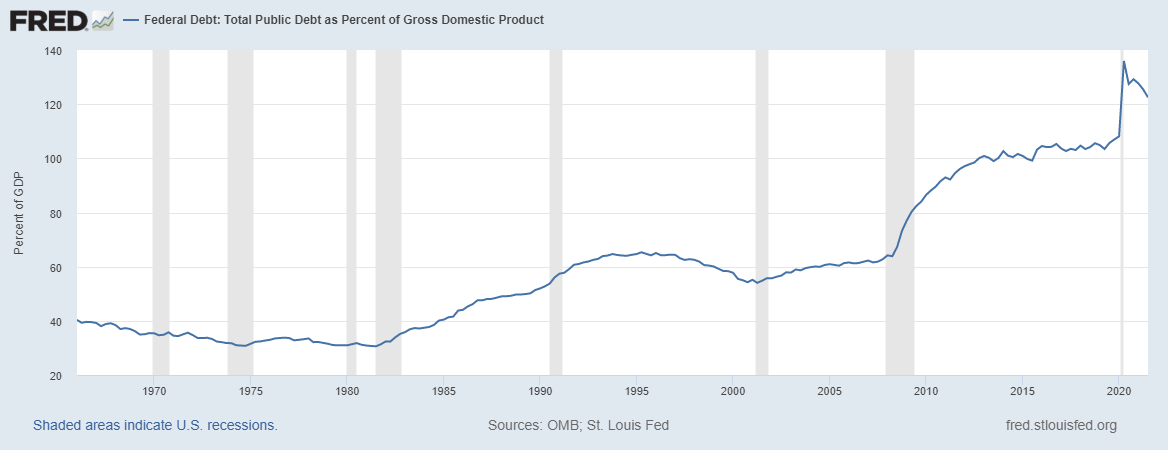

The other day, I was writing about inflation and the national debt, and a commenter asked me whether inflation had caused the debt to go down in real terms. I checked, and to my surprise, I found it had! From the first quarter of 2021 to the third quarter, despite two huge Covid relief bills — the $0.9 trillion bill in December 2020 and Biden’s $1.9 trillion bill in March — the national debt actually fell in inflation-adjusted terms:

I’ve talked a lot about the effect of inflation on wages, and the danger that it could explode and damage our economy. But there’s one other important effect of inflation that I haven’t talked much about. Inflation erodes debt. And this has important implications for the distribution of wealth in our society.

The monetary economist Narayana Kocherlakota once said that “money is memory”. If so, inflation is forgetting. By reducing the value of a dollar, inflation makes every economic transaction that happened in the past mean less. When inflation happens, every dollar you owe, and every dollar someone owes you, means less in terms of the real physical things that matter — in terms of months of rent, loaves of bread, hours of labor. And thus the record of the financial past — of the dollars you accumulated, borrowed, and lent out — gets gradually wiped away.

It’s not clear whether this is a bad thing or a good thing, overall — obviously it depends on your point of view. To conservatives, inflation may seem like a cheat card, allowing the spendthrift to avoid ever paying back the full value of what they consumed. To progressives, inflation’s erosion of debt might seem like a blessing — a wealth tax for the rich and a partial debt jubilee for the poor.

And there are subtler effects on the economy’s productive potential — effects we don’t entirely understand yet. If inflation can be contained, it could help make the national debt more sustainable over time, actually reducing the chance of a future hyperinflation. And by eroding the overhang of private-sector debt built up before the Great Recession, it could eventually prime us for faster growth. But neither of these is very certain.

So let’s think a little more about how inflation erodes each type of debt, and what this means for the economy and the various actors in it.

How inflation erodes government debt — and what that means

How was a little bit of inflation — less than an 8% annual rate — able to drive down the real value of government debt in just two quarters, despite the fact that we spent almost $3 trillion on Covid relief during that time? Part of the answer is that the economy was recovering quickly, so tax revenues were pouring in and the government didn’t actually have to borrow that much money. But at the same time, inflation was eroding the value of the entire stock of national debt. By the time we hit the current price acceleration, our federal government had borrowed about $28 trillion overall, and this entire base was getting eroded at a more rapid rate.

Now, you may ask, why do price increases for stuff like rent, gasoline, and food make the government’s debt less onerous? The answer is that the government’s ability to pay back a dollar of debt depends on its ability to tax a dollar from the economy. And its ability to tax the economy depends on the number of dollars in the economy. When the dollar prices of rent and gas and food go up, the companies that sell rent and gas and food make more dollars of profit, and their employees and suppliers make more dollars of income. Eventually those dollars get taxed (usually multiple times).

In fact, an alternative way of looking at the government’s real debt is to look at it as a fraction of nominal GDP. And this has gone down even faster than inflation-adjusted debt, thanks to the rapid economic recovery! In fact, relative to GDP, by Q32021 we had already erased almost half of the amount that we added to the national debt in the early days of Covid:

And that amount is sure to be greater now. Thanks to continued rapid inflation and the V-shaped recovery in real economic activity, we could conceivably erase all of the Covid debt and start working our way into the debt we took on during the Great Recession.

Meanwhile, someone is on the losing end of this. Inflation doesn’t substantially increase the number of dollars government owes to the people who hold government bonds — the Fed, China, private banks, and so on. Crucially, the U.S. government borrows most of its debt at a fixed nominal interest rate, denominated in dollars. So these bondholders are getting stiffed, because they’ll be paid back in dollars that are now worth less. (There is a small amount of U.S. debt that does get adjusted for inflation, and this does increase.)

So what does this mean for the economy? First of all, paradoxically, the erosion of government debt probably reduces the danger of hyperinflation. Most economists believe that hyperinflation usually happens when the public starts to believe that the government is going to borrow without limit, financed by the central bank. This means that an increase in the size of government debt can act as a warning sign to the public — a signal that we’re getting closer to that invisible cliff when everyone loses confidence in the system. By the same token, a reduction in the size of debt means we’re further from the cliff. By making our big stock of existing national debt easier for the government to pay off, inflation is actually increasing confidence in the system.

Of course, we have to weigh that against the decreased confidence from higher inflation itself. But if the Fed can keep inflation expectations contained without damaging the recovery — which it currently seems to be doing — a period of sustained 5 to 7 percent inflation might actually be a good thing for the sustainability of our national debt!

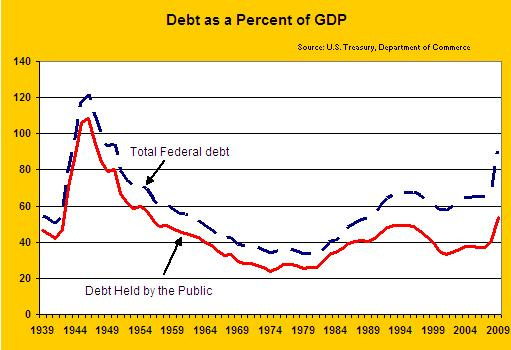

In fact, inflation is part of the reason the U.S. was able to reduce its national debt after the huge borrowing binge of WW2. Economists Joshua Aizenman and Nancy Marion have a nice article about how this worked, with the following graph:

They write:

In a recent paper (Aizenman and Marion 2009), we examine the role of inflation in reducing the Federal government’s debt burden. We conclude that an inflation of 6% over four years could reduce the debt/GDP ratio by a significant 20%.

In other words, people who are very worried about the national debt might actually breathe a sigh of relief when they look at the inflation numbers!

How inflation erodes private debt — and what that means

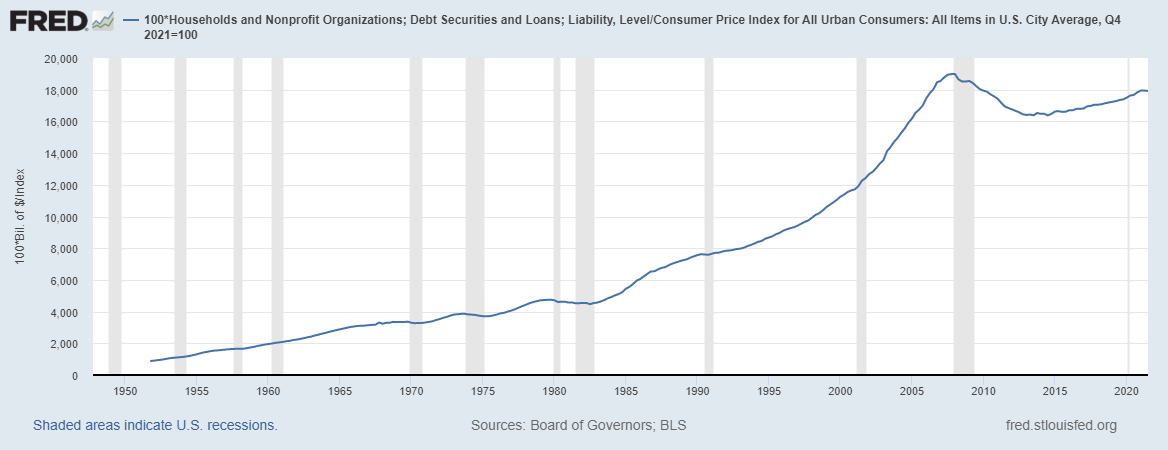

Meanwhile, inflation is also reducing the real value of private debt. Let’s look at household debt:

As you can see, Americans borrowed a huge amount over the years, and then worked mightily to pay off this debt after the housing crash and the Great Recession. They did this with relatively little help from the government, which spent a lot of money but pointedly avoided a big bailout of homeowners or consumers. (That thriftiness probably prolonged the recovery from the Great Recession by reducing aggregate demand, btw.)

Now, inflation is helping to erode household debt further. Borrowing has accelerated in dollar terms since Covid hit, but it’s flat in real terms in 2021. If inflation continues and borrowing cools off, the stock of household debt will be eroded further.

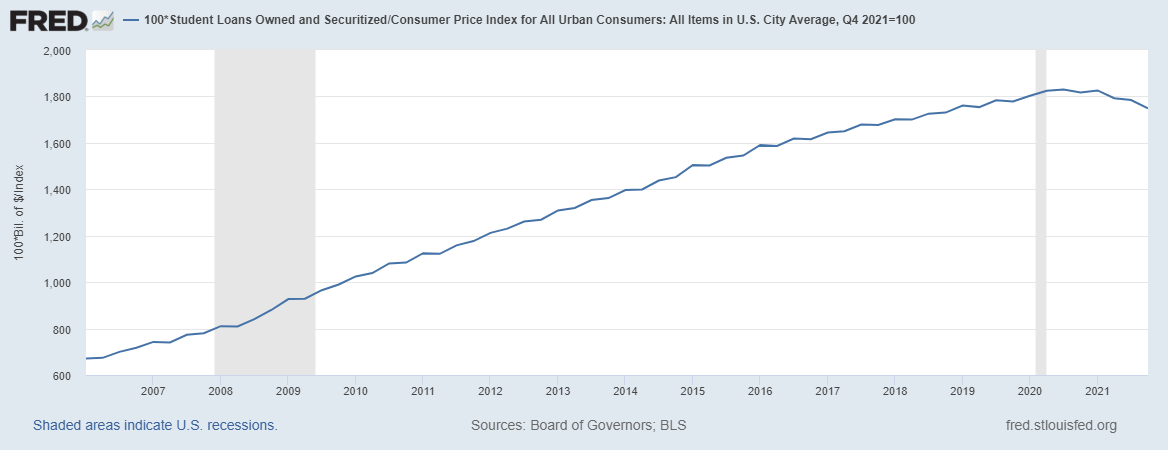

Let’s look at the impact on some specific types of debt. Student loans, the big bugaboo of the post-Great Recession era and the thing that people are always screaming about on Twitter, are now going down in real terms:

Now, this erosion might be less impressive in terms of ability to pay. Just as we measure government debt against GDP, we should measure student debt against the nominal income of people who hold that debt. And that ratio may not look as nice, since wages in the upper part of the pay scale are failing to keep pace with inflation:

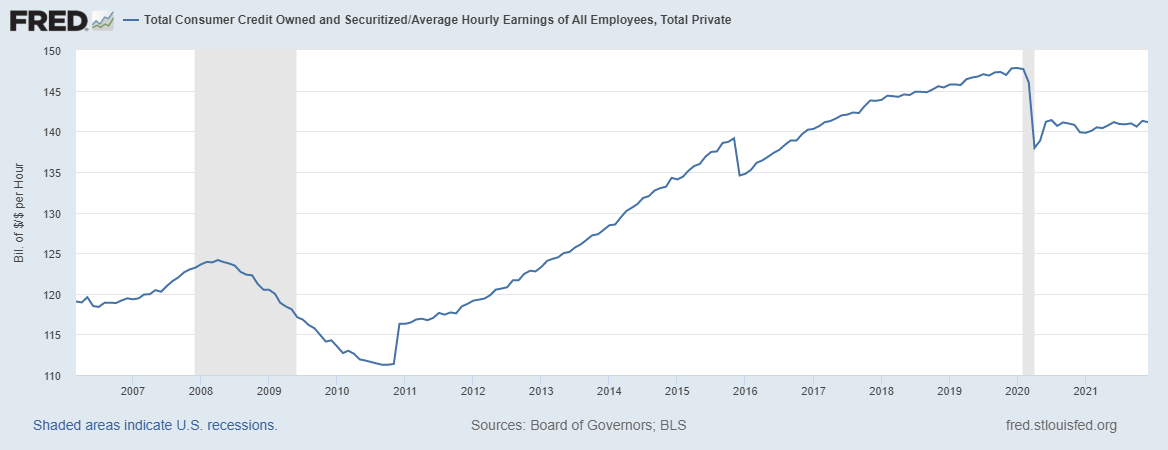

For people at the lower end of the pay scale, however, wages are zooming up even faster than inflation, and their debts are getting eroded accordingly. Consumer credit relative to average hourly earnings is lower than it was before the pandemic; Covid relief spending helped people pay off their debts, and now inflation is canceling out the new debts they’re taking on:

So while highly educated leftist types will gnash their teeth that the burden of student debt isn’t going down more, progressives who worry about the debts owed by the poor to the rich can rejoice in the partial redistribution represented by this inflation.

As for homeowners, the effect is uncertain, but people with mortgages will probably come out ahead. Inflation erodes the value of fixed-rate mortgages very mechanically, but home values probably do rise somewhat when prices rise (because rent rises, and because rising incomes creates higher demand for real estate).

So you see that the effect of inflation on household balance sheets is pretty complex, and depends on what kind of debt you have and how you make your money.

Of course, private debt is also credit; for every dollar that’s borrowed, someone has to lend a dollar. Just as households’ liabilities are getting eroded by inflation, their assets are getting eroded as well. But there are multiple reasons why this doesn’t mean inflation is just a wash for households.

First, poorer people tend to be net debtors and richer people tend to be net creditors, so inflation redistributes from richer people to poorer people. For a nation whose wealth inequality has skyrocketed in recent decades, inflation will act as a partial countermeasure. People whose wealth is mostly in stock — e.g. entrepreneurs — will not see nearly as much of a hit to their real wealth, since stocks are an OK long-term hedge against inflation — as prices rise, so do the profits that give stocks their value. Indeed, the wealthiest people, who are mostly founders, have seen their total wealth increase much faster than inflation over the last year. The wealthy people who are hit most are those who have more of their wealth in bonds. Statistically, this means older people, so inflation will also act as redistribution from the Boomers to Millennial and Gen Z borrowers.

Now, if you’re a an old person with lots of bonds, this probably makes you mad. Young people and poor people are getting a freebie at your expense. And if you’re a conservative, you might be mad that people who didn’t save their pennies are now getting a partial bailout for their irresponsible behavior, at the expense of the thrifty responsible people. But if you’re a progressive or a young person or a poor person, you’re probably a lot less mad.

The second way household debt erosion matters is that having a lot of private-sector debt can endanger the economy. Imagine if you and I owe each other nothing — we’re definitely not going to default, because there’s nothing to default on. But imagine if you and I each owe each other $100,000. Now, a shock to either of our incomes may cause us to default (since we might not be able to call in the other person’s debt right away). So even though our debts still net out to zero, now the economy is more fragile because of the default risk.

And after a big shock like the housing crash and the Great Recession, people often become more cognizant of that default risk, and start paying down their debts to each other all at once. This can reduce aggregate demand and lead to a slower recovery — what economist Richard Koo calls a “balance sheet recession”.

So by eroding the stock of private debt and credit, inflation may make our economy more robust to future shocks. That’s good.

What about interest rates?

Anyway, we’ve seen that the effects of inflation — which we might call “monetary forgetting” — are complex and subtle and not completely understood. And in fact, there’s another wrinkle: Interest rates. Erosion of the stock of debt is one thing, but inflation also affects the amount borrowers have to fork over each month.

Inflation, if it lasts, eventually causes nominal interest rates to rise. One reason is because lenders now expect higher inflation going forward, and raise the interest rates they charge borrowers in order not to continue getting screwed. A second reason is that the Fed will typically raise interest rates to contain inflation (as indeed it is expected to do this year).

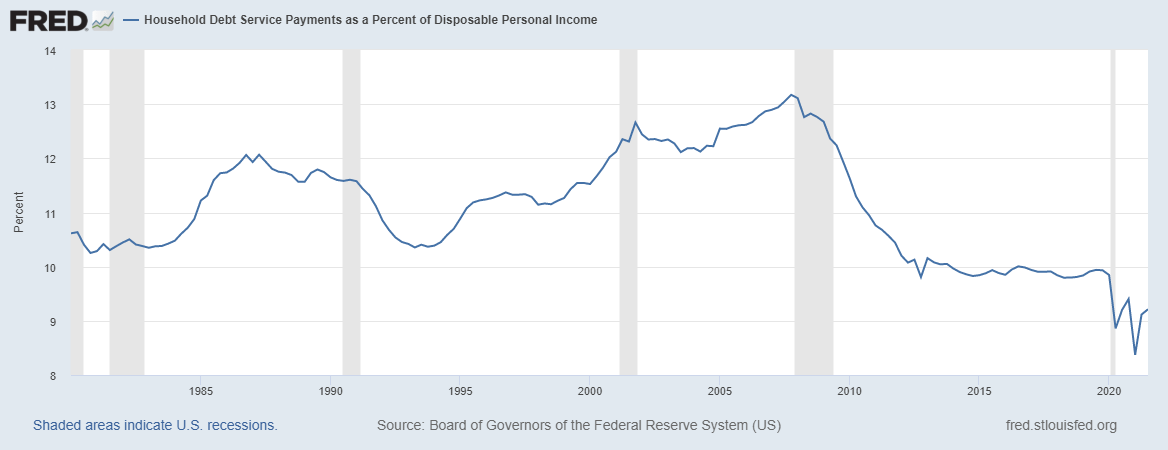

This can affect borrowers’ costs in the long run. If you were thinking about refinancing your mortgage or your student loans, or if you needed to roll any of your debt over on an ongoing basis, then higher interest rates will increase your borrowing costs. Since the Great Recession, household debt service costs have been at low levels thanks to low interest rates:

Rate hikes will probably reverse some of that decline; debtors will owe less overall, but the monthly payments will get more burdensome.

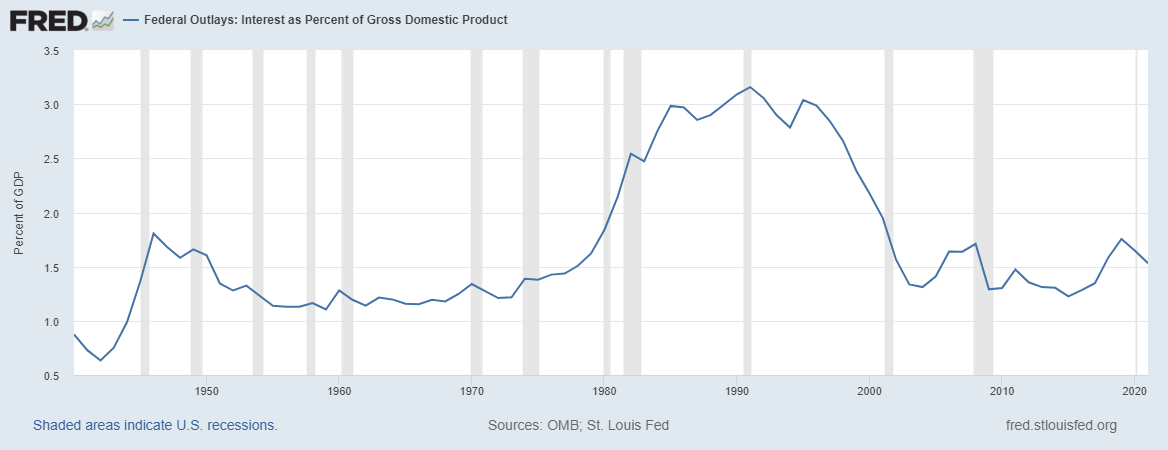

The same is true of government, which has been able to sustain higher debt levels quite easily thanks to low rates:

Rate hikes could force the government to either borrow more to cover interest payments, or engage in economically painful austerity (tax hikes and/or spending cuts).

So while inflation does cause a great forgetting of financial history, that forgetting eventually comes at a price. The hope is that that price will not be too large. Since inflation was probably ultimately driven by Covid relief spending (exacerbated by supply chain fragility and other factors), the end of that big spending plus the Fed’s rate hikes means inflation will probably calm down in the next year or two:

So the pain from rate hikes will hopefully be temporary and limited. But the erosion of government and household debt represented by this burst of inflation will be permanent, just as it was after World War 2.

We are erasing some of the financial memory of the 2000s and 2010s. And though that’s not all good news, I think in general this is for the best. There are a lot of things about the financial history of the last two decades that I think most Americans would like to forget.

The gains of debtors needing to pay less than expected, will likely be balanced by the losses of the debtors of the future, who will be less likely to get a loan whatsoever. That is the biggest cost of inflation, in my view.

The article by Aizenman and Marion didn't mention this (unless I missed it in my skimming) but one reason inflation helped so much with the post-WW2 debt was that Treasuries had a maximum cap of 2.5% interest. There was no market at work and basically nobody wanted to buy bonds and the Federal Reserve was left holding the bag.

The whole thing led to a civil war between the Federal Reserve and the Treasury which wasn't resolved until a detente in 1951.

(This whole 1942-1951 era is probably my favourite weird Federal Reserve trivia.)