Three holes in the U.S.' economic strategy against China

Legacy chips, drones, and coordination with allies.

It almost feels a little pointless to write this post right now. The Biden administration isn’t going to be able to do much more on the China front before election day, and if Trump wins, all bets are pretty much off in terms of China policy. But I think it’s good to push these ideas into the general discussion anyway.

The transformation of U.S. economic policy is all about China, and it’s all about defense competition. As Greg Ip has written, the new paradigm has three pieces — industrial policy, export controls, and tariffs. Tariffs protect militarily useful U.S. industries from being devastated by sudden waves of Chinese exports, industrial policy builds up the U.S.’ militarily useful industries, and export controls slow down China’s development of military useful industries. There are some other benefits to these policies too — decarbonization, job creation, technological progress, etc. — but ultimately it’s the defense balance between China and the developed democracies that’s fundamentally driving everything here.

As general frameworks go, the Biden administration’s three pillars aren’t bad. Industrial policy has yet to be proven, tariffs can easily backfire and hurt U.S. manufacturing if misused, and the export controls still contain lots of loopholes. But in general this is a reasonable approach.

It’s not enough, though. It’s pretty easy to identify at least three big remaining holes in the new policy approach. As Ip writes, “a fourth leg, a unified economic front with allies, remains unrealized.” Tariffs, meanwhile, aren’t easily able to target Chinese components if the final product is assembled outside China. And while industrial policy in the chip and battery industries is important, the U.S. is still neglecting drones.

Stop Chinese “legacy” chips from powering everything

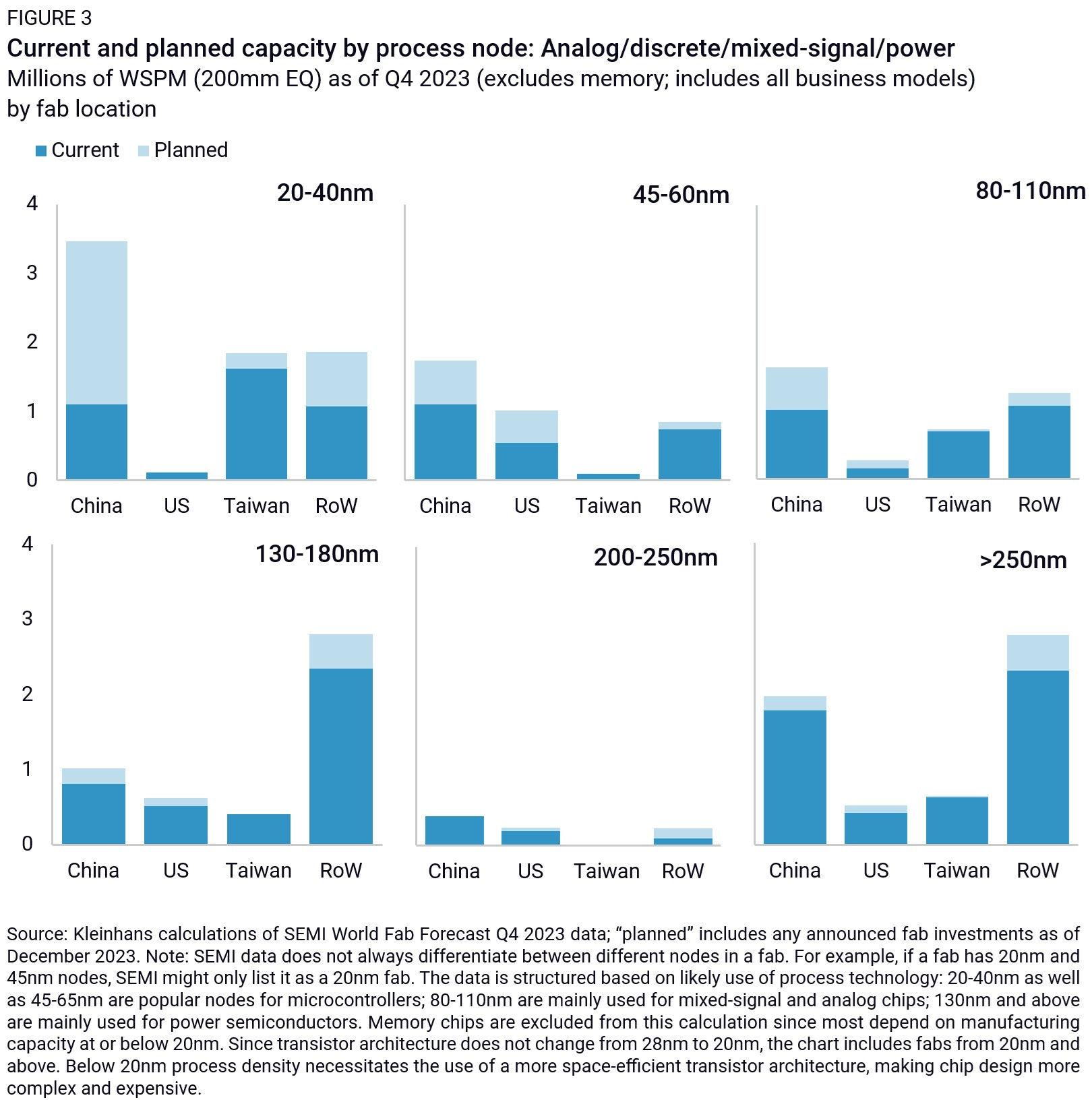

The U.S. export controls on China are meant to prevent China from dominating the manufacturing of advanced cutting-edge semiconductors. There’s little hope of stopping Chinese progress in chipmaking, but the hope is to slow down their progress to the point where the U.S. and its allies can stay ahead. This is why the export controls and some other restrictions were designed with a “small yard, high fence” approach in mind.

But plenty of computer chips are not leading-edge. They are “legacy”, “trailing-edge”, or “foundational” chips (three terms that mean the same thing). They are older tech that’s much simpler to make — China already knows how to make them, and has the tools to make them in large numbers. Export controls have little or no hope of impeding China’s progress in making legacy chips.

But just because legacy chips are technologically less sophisticated doesn’t make them less important. As the Rhodium Group notes, these chips power most of the things in our economy:

Legacy chips are pervasive and therefore essential. Virtually every electronic device—including cars, airplanes and fighter jets, medical devices, smartphones, computers, and agricultural and industrial equipment—is powered by mature node chips in conjunction with leading-edge processors. Pandemic-related restrictions drove home how the absence of a single chip could hold up entire manufacturing assembly lines, leaving consumers in disbelief that their new cars could be stripped of features normally taken for granted, like seats that heat up and adjust automatically.

Currently, a majority of these chips are still made outside China, but China is racing to catch up, building absolutely enormous amounts of new fabs:

Much of this new capacity will be used in China, to make products for Chinese consumers. But much of it will be exported — either directly, or embedded in other Chinese-made products such as cars and electronics. As we’ve seen with autos and batteries, once China revs up its industrial machine and starts showering an industry with subsidies, it can be very hard for companies in other advanced countries to survive in the face of the onslaught. And legacy chips are one of China’s most heavily subsidized industries.

There are several ways this could hurt the U.S. and its allies.

First, competition from China’s legacy chip industry could swamp and destroy much of the chip industries of the U.S. and its allies — Japan, Korea, Taiwan, and Europe, as well as the nascent chip industry in India. This would put supply chains in danger in the event of a war.

It would also deprive chipmakers outside China of the revenues to fund development in leading-edge chips, leaving them more dependent on government subsidies. Destroying the legacy chip businesses of companies like TSMC, Intel, and Samsung could be China’s answer to export controls.

And finally, there’s the cybersecurity angle. Some people fear that Chinese-made legacy chips could come with built-in backdoors that would allow China’s military to spy on Americans, disable U.S. infrastructure, turn a bunch of U.S. equipment and consumer products into bricks, or even take control of vehicles and crash them.

So there are plenty of reasons to try to prevent China from being the country that makes legacy chips for everyone else. But how to do that? The Rhodium Group suggests various types of trade barriers, including tariffs, to keep Chinese chips out of the U.S. supply chain. And Chinese chips were included in Biden’s recent round of tariffs.

But you can’t put a tariff on something you don’t even see coming into the country. Currently, the U.S. government has very little idea where the chips in its imports come from. If a car from Mexico or a laptop made in Thailand has a Chinese chip somewhere in it, the U.S. government simply doesn’t know about it. This means that although it’s pretty easy to block imports of Chinese chips themselves, it’s very hard to block imports of products that contain Chinese chips.

The first task, then, is to get good data on where all the chips in U.S. imports come from. Right now, data on component imports only comes out from the OECD with a lag of several years, and even that does not provide a product-by-product and company-by-company breakdown. The U.S. needs to implement a reporting and inspection regime that gives the government good, up-to-the-minute information on where every computer chip in the country was physically made, which company owned the factory that made it, and which company designed it.

Data is clearly the most important thing here. But there are also some other policy steps we could take, as outlined in a recent Noahpinion guest post by Steven Glinert. These include A) export restrictions on software used to design legacy chips, and B) more CHIPS Act money or similar subsidies for legacy chipmakers. Both of these would probably have only a marginal effect, but they could be a complement to trade barriers.

Really, though, data is the key thing here. You can’t fight what you can’t see, and currently, the U.S. government can’t see Chinese chips at all. I don’t know of any current or planned government effort to identify Chinese chips in U.S. imports.

Build a civilian drone industry

U.S. industrial policy, export controls, and tariffs are aimed at strategic industries — chips, autos, batteries, and so on. But there’s a hugely important industry that seems to have left out of this effort so far: drones.

By now, many, many writers have pointed out that drones have become essential to modern warfare. In Ukraine, vast numbers of drones are used for reconnaissance, artillery targeting, destroying enemy vehicles, and even killing enemy personnel directly. If you can stomach it, I recommend watching a small toy drone armed with a simple explosive chase down and kill a Russian soldier on the battlefields of Ukraine. That drone was piloted remotely by a human, but in the not-so-distant future, drones will be autonomous AI-powered killing machines. At that point, it’s an open question of whether human soldiers will even be able to survive on the front lines of war.

Basically, there are two ways to power a drone: internal combustion engines, and electric motors. Drones powered by internal combustion tend to be larger, heavier, faster, and more powerful. But electric drones tend to be much cheaper and can be manufactured in higher volumes. A Shahed drone, one of the smallest and cheapest internal combustion drones, costs somewhere between $20,000 and $375,000 apiece. In contrast, a DJI Mavic 3 costs around $2,000, while a larger Matrice 300 costs around $13,000. Both types of drones have their uses on the battlefield, meaning any country that can’t build or easily procure cheap electric-powered drones in large numbers is now at a disadvantage in war.

Chinese companies currently have an overwhelmingly high market share in the manufacture of commercial electric drones, with DJI as the dominant player. The second-biggest company is the U.S.’ Skydio, but they’re still far behind DJI, and there are no other big U.S. drone-makers. This means that modern battlefields like Ukraine are being dominated by Chinese-made products. And it means that if China ever goes to war with the U.S. and its allies, the latter will find themselves without a lot of small electric-powered drones.

The U.S. has considered banning Chinese drones, but as far as I know, no one is talking about an industrial policy to build up the U.S.’ own drone industry. The Biden administration seems to be thinking about drones as analogous to missiles or artillery shells — a form of ammunition rather than a type of vehicle, and therefore something that only the military needs to buy. But in a protracted war with China, a civilian U.S. drone industry would provide important surge capacity for the U.S. Military, much like automakers made tanks and airplanes during WW2.

One possible industrial policy to encourage the creation of a U.S. commercial drone industry would be deregulation. The FAA has already loosened regulations on small commercial drones considerably, but allowing drones to be operated beyond visual line of sight (BVLOS) would help considerably, since this is how drones are used in wars. BVLOS deregulation is now in the works in Congress, but it’s not yet clear how meaningful the changes will be.

But although you can encourage drone consumption with deregulation, in the end you’re limited by how many consumers actually want to buy drones. With electric cars and computer chips, this was less of a problem, but drones are kind of a niche market, even in China. Usually, manufacturers need a big consumer market in order to scale up and drive down costs. So how did Chinese companies get so good at making drones?

Glenn Luk had a great post about this back in 2018, where he pointed out that most of the things that are used to make a drone are also used to make a phone. The big exception is the electric motor itself, which is more similar to the motor in a blender or other household appliance.

So a U.S. industrial policy for drones would simply entail incentives for manufacturing drone components — electric motors, displays, cameras, etc. — in the U.S. or select allied countries. This would be similar to the way the Inflation Reduction Act incentivizes domestic manufacturing of batteries, rather than the way the IRA incentivizes the manufacturing of EVs themselves. The final demand for the consumer products that these components would go into — phones, electric appliances, and so on — would already be there (and in fact, some of that demand is already subsidized by the IRA).

This industrial policy wouldn’t cost nearly as much as the IRA or the CHIPS Act, since electronics components other than chips and batteries are pretty cheap. But it could help resuscitate a domestic consumer electronics industry that could be quickly repurposed as a drone industry if needed. So although no one seems to be talking about subsidizing the electric motor industry or the display industry, it seems like a useful hole to plug.

A united front

It’s important to remember how much bigger China is than the U.S. It has four times the population and twice the manufacturing capacity by value-added. Any protracted conflict between the two countries would see the U.S. badly outmatched, despite its modest remaining advantages in some areas of technology. In other words, U.S. national security relies crucially on alliances — in order to be able to stand up to a much bigger opponent, you need a gang.

While the U.S. is pretty good at military alliances, it’s not as good at economic alliances. To be fair, no one really is — economic relationships are much more multifaceted than defense cooperation, so there’s no standard template for exactly how they’re supposed to work. But there are a few areas where the U.S. could cooperate more closely with allies in the quest to build a multinational economy capable of matching China’s.

The most obvious area is export controls. The U.S. needs countries like the Netherlands, Japan, Germany, South Korea, and Taiwan to cooperate if it’s to have any chance of keeping cutting-edge chipmaking technology out of China’s hands. So far, the Biden administration has done a pretty good job of this.

Second, the U.S. should immediately pursue defense manufacturing collaboration among all its allies. The U.S.’ withered defense-industrial base and lack of a commercial shipbuilding industry means will take time to fix; in the meantime, America should be relying heavily on partners like Japan and South Korea to make the military materiel needed to deter China. Fortunately, there are already some moves in this direction:

The U.S. and its allies in the Indo-Pacific are moving toward establishing a de facto "common market" for the defense industry, setting the same industrial standards and reinforcing each other's defense industrial base…The recent loosening of export controls among AUKUS partners…for building nuclear-powered submarines has created an opening for more region-wide defense-industry collaboration among allies, economist and defense analyst William Schneider said…

Schneider said that Japan in particular was ripe for such defense collaboration at the industry level, citing the country's substantial shipbuilding capacity.

Undersecretary William LaPlante, the Pentagon's top official for acquisition and sustainment, will start meeting with Japanese counterparts…to discuss collaboration. He will convene in Tokyo the inaugural meeting of the U.S.-Japan Defense Industrial Cooperation, Acquisition, and Sustainment Forum, inviting representatives from American and Japanese defense contractors to discuss joint development, production and maintenance of weaponry…

"One of the things that Undersecretary LaPlante is promoting is the concept of an alliance industrial base," Schneider said.

A second area, which the U.S. has done much less on, is trade. I wrote about this a couple months ago:

China’s strategic companies — Huawei, BYD, and the rest — have access to one gigantic market. By some measures, that market is even bigger than that of the U.S. But the U.S., Europe, Japan, Korea, etc. would be an even bigger combined market. Unifying those markets would give American and allied companies — Intel, Boeing, Samsung, Toyota, Airbus, Tesla, Hyundai, and so on — the ability to scale more and to drive down costs. If India were added, the bloc would be even bigger and more powerful.

So to the degree that the U.S. can forge its alliances into a unified trading bloc, it should. The challenge, however, is that most other countries are not as willing to cut China out of their supply chains. Forging an anti-China economic bloc is kind of useless if the other members of that block are just acting as conduits for Chinese goods. The Biden administration has made some efforts to get other countries to come along on Biden’s tariffs, but these efforts will inevitably be very sparse and of dubious effectiveness.

One idea here would be to reward strategically important companies in allied countries with access to the U.S. market in exchange for harmonizing their China trade policies with America’s. Those companies would effectively be offered a choice — do business with the U.S. or do business with China. Meanwhile, the U.S. could ask allies to offer similar deals to its own companies in strategic industries.

Alternatively, if the U.S. can manage to get good data on component sourcing throughout the supply chain, it could just enact free trade agreements with all its allies and then tax Chinese components. But this would require both A) much better data collection on imported components, and B) the American public agreeing to something called a “trade deal”. In the wake of the bipartisan crusade to sink the TPP, prospects for the latter look dim. So the real trick here is to get the benefits of a trading alliance without triggering a protectionist backlash.

In general, though, I think more rhetoric about economic alliances, and the differences between trading with allies and trading with enemies, would help prepare the American public for all of the policies listed above. The U.S. facing a rival bigger and more powerful than any we’ve ever faced, and there’s just no way we can go it alone. That’s a message I don’t expect Trump or his followers to be receptive to, which is why Democrats need to stand up and lead here.

"Which is why Democrats need to stand up and lead."

Noah's conclusion says it all. The Trump GOP is, sadly, not up to the task. Despite their political rhetoric to the contrary. Their latest natsec betrayal was Speaker Johnson's six month obstruction of a $90bn investment in American munition manufacturing capacity. That's SIX months. At Trump's urging. With friends like that, who needs enemies?

I built radio control airplanes 30 years ago. 6 ft wingspan. 20lbs. And I worked with the auto industry for 20 years. Been in every plant that makes everything you can think. Steel. Dies. Stamping. Copper smelt, wire drawing, wire coating. Motors. Actuators. Glass to optics. Every plastic. Aluminum. Forging, progessive die stamping. Die casting. Blow molding, extrusion.

So like a car system, a drone needs a few basic things in high volume.

Mechanics and structure - light weight injection molded plastics. Fuselage .empennage

Electrical system:

Brain - CPU - make or ask Samsung. Buy a million Androids. Use them

Sensors. CMOS - cellphones

Optical lenses- cellphones again. Injection

molded or high volume glass molding

Actuators- motors- high speed, small servos. Moog & auto electronics

Gyros- well ..develop that here

Flight. Sense. Compute. Act-actuate.

Basics -

A. This is absolutely not forever something low volume, high cost defense industry can do..

B. This is not good for VC startups. They dont make many things. Too much learning curve

C. Between teams from Detroit, a bit of current DoD drone experts, Mexico or US volume assembly, and Samsung - you have your China beating DDT - Drone Dream Team.

14 months - 100,000 6ft drones a week. 1 million 1 ft drones a week. 100 20ft strategic drones a week

Book it.