Sizing up the New Axis

The stiffest economic competition we've ever faced

I wish I didn’t have to live through an era of renewed great power conflict. I wish the end of the Cold War had meant that such destructive episodes were forever relegated to the history books. But unfortunately, those wishes did not come true. The Ukraine war means that we are now definitely in a long-term Cold War type struggle with Russia. And the substantial chance of a Chinese invasion of Taiwan sometime in the next few years — as highlighted by the furor over Nancy Pelosi’s planned Taiwan visit — means that there’s a high likelihood that we’ll also soon be enmeshed in a contest with China as well.

Hopefully neither of these conflicts will result in direct war between great powers (especially because all the great powers now have plenty of nuclear weapons). I am not arguing that we are headed for World War 3 here. But a sequel to the Cold War — a protracted geopolitical struggle in which both sides prepare for the possibility that they might have to fight each other — seems extremely likely at this point. So likely, in fact, that we can’t afford not to plan for it.

That’s what the concept of the War Economy is about. As Anduril founder Palmer Luckey says, “current year is too late to care about current thing”. We began to prepare for a possible conflict with the original Axis several years before World War 2 broke out, and in the Cold War we prepared for a World War 3 that fortunately never came. We must prepare again now. And that means far more than just spending money on defense; it means reorganizing our economy to promote certain industries, build or rebuild certain capacities, and reorganize supply chains.

The scale and nature of the task is determined by the capabilities of the opposition. In World War 2, the Axis powers had advanced manufacturing prowess, but small populations and a lack of access to fuel. In the Cold War, the Soviet bloc had a lot of fuel and a population similar to ours, but had a small and dysfunctional economy and struggled with advanced manufacturing. In contrast, a potential “New Axis” of Russia and China would control enormous population, vast fuel resources, advanced manufacturing capabilities, and a combined economy of enormous size. Except for the fuel part, this is all just China.

So today’s post is about how the U.S. and its likely allies stack up against the New Axis in economic terms.

Is there actually a New Axis?

Before we compare the two potential blocs, we should ask whether the New Axis is a real thing. “New Axis” is just a term I made up to refer to the combination of China and Russia (and whatever other allies and fellow-travelers they can muster). The idea that these two powers are de facto allies against the U.S. is based on the joint statement they released before the Ukraine war.

When I use the tern “New Axis”, though, people occasionally scoff, arguing that China and Russia have too few common interests and too much mutual suspicion to form any kind of close alliance. And maybe this is true. So far, China has been reluctant to offer substantial support to Russia for its invasion of Ukraine:

Chinese companies, afraid of sanctions, aren’t even investing much in Russia.

But it’s worth remembering that the original Axis wasn’t that close of an alliance either. Germany and Japan signed some agreements and both fought against the U.S., but they didn’t work together much at all during the war. They also didn’t team up against the USSR — Japan signed a non-aggression pact with the Soviets (which the Soviets themselves broke only in the very last days of the war), and notably failed to come to Germany’s aid in Operation Barbarossa.

In order to be comparable to the original Axis, a New Axis of Russia and China wouldn’t even have to work together militarily or give each other arms. Russia would have to sell China fuel, but other than that, they really could just ignore each other and focus on fighting the U.S. and its allies in separate theaters.

Even in this “minimal New Axis” case, the U.S. and its allies have to prepare to oppose both Russia and China at the same time. As long as Russia and China don’t fight each other and Russia provides China with fuel, they might as well be allies in the new Cold War.

Who would the two blocs include?

To size up the two blocs, we have to assign countries to them, and this is highly speculative. Even in World War 2, the final composition of the Allies wasn’t determined until Hitler invaded the USSR; indeed, during the early days of the conflict, it looked as if the USSR might even join the Nazis, or at least sit things out. So there’s a lot of guesswork here.

On the New Axis side, I’m just going to include China and Russia. North Korea is also included, but it’s very small and really all it can do is fight South Korea, so I’ll ignore it. Then there are a couple of wild cards like Pakistan and Iran, but these have generally low capabilities and little reason to get involved with a global great-power conflict, so I’ll leave them out too.

The harder question is which countries would be on the U.S.’ side in this new Cold War. Putin’s invasion of Ukraine has united most of Europe against Russia and deepened transatlantic cooperation, which puts a lot of people and GDP and manufacturing capacity in the U.S.’ corner. And Japan will likely be the U.S.’ main partner in a conflict with China over Taiwan. So I’ll include the EU, the UK, and Japan in the “New Allies”. I’ll leave out South Korea, assuming it will be tied down by North Korea. I’ll also leave out some smaller countries like Canada and Australia that would almost certainly be part of the New Allies; this is at least partially balanced by the fact that some EU countries like Hungary wouldn’t really cooperate.

The really big wild card here is India, which has a huge population and a reasonably hefty economy. The USSR was India’s protector during the Cold War, and much of India’s military equipment still comes from Russia (though this is starting to shift). So India can’t be expected to enter into any conflict against Russia. But China is a very different matter. China is India’s main military threat, and the two countries have come to blows recently over a disputed border. They are also rivals for influence in the Indo-Pacific region. This is why India has joined the Quad, forging a loose quasi-alliance with the U.S., Japan and Australia whose purpose is obviously to hedge against China.

Thus, because India’s status is still pretty uncertain, I’ll do two comparisons: one with just the New Allies of the U.S., EU, UK, and Japan, and one with the New Allies + India.

Because of the uncertain nature of the coalitions (and because of my omission of smaller coalition partners on both sides), these comparisons should be taken as rough and indicative rather than definitive. All numbers are the most recent available.

The tale of the tape: Population, GDP, and manufacturing output

“Quantity has a quality all its own.” - Joseph Stalin

First, let’s just talk about population. Obviously that’s only one input to national power, but it’s worth looking at anyway:

What this chart really just shows is that China and India are really, really, really big compared to every other country, and even compared to the EU. That’s a fact worth remembering.

Now let’s look at GDP. GDP is important for military strength because unless you’re operating a command economy, you have to pay for your army somehow, and GDP determines the available tax revenue. There’s a debate as to whether it’s more appropriate to use nominal GDP or purchasing power parity adjusted GDP in these comparisons. So I’ll just sidestep that debate by showing both, because they really don’t tell that different of a story:

Numbers here are in millions of dollars.

The basic story here is that the New Allies have a substantially higher GDP than the New Axis, with or without India on board. The difference is a bit narrowed when we use PPP, to a ratio of 1.7 instead of 2.3 (without India). The other thing we see from this comparison is that in economic terms as well as population, the New Axis is mostly just China.

Of course, we could expect these figures to change in the result of a war, as a result of sanctions, disruptions to supply chains, financial market changes, war production, and a variety of other things. So this is just an indicative measure of where we stand.

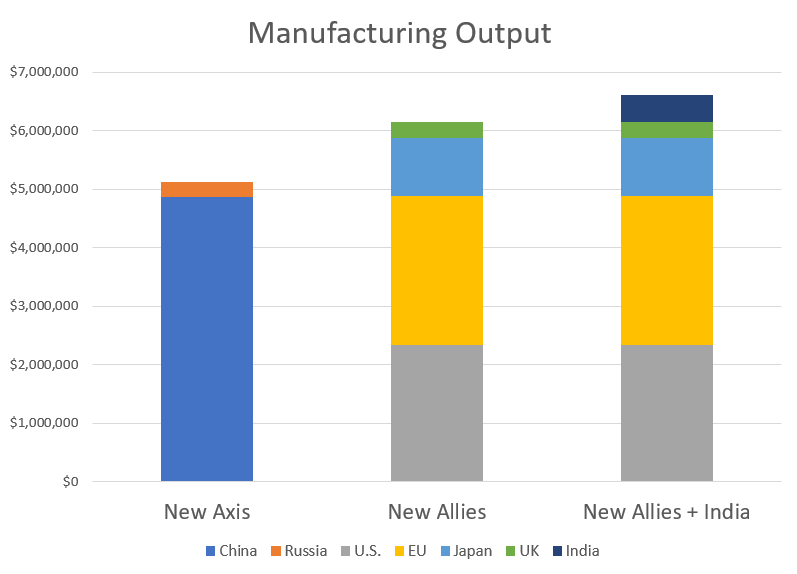

But anyway, paying for your army is one thing, but if your alliance can’t actually make the things you need to fight a war, then having a bunch of dollars is not so useful. Modern warfare requires making a lot of stuff — missiles, drones, ships, tanks, trucks, ammo, and so on. So manufacturing output is probably important, above and beyond simple GDP; when a war rolls around, dollars that come from tourism, or from selling fancy wine, are going to be of less use than dollars of factory output. Anyway, here’s the comparison, again in millions of dollars:

Here we see it’s a much closer-run thing. India doesn’t manufacture a ton, so with or without India, the New Allies just barely out-manufacture the New Axis.

The reason, as before, is China. As Damien Ma says, China has become the “make everything country”. Before the turn of the century, a very large percent of the manufacturing in the world, in terms of value, was done in the old industrialized economies of the U.S., Europe, and Japan. But in the last 20 years, China has emerged as a second center of manufacturing that rivals all of the old industrialized nations combined. On some deep level, I suspect this shift is why we’re seeing the revival of great-power conflict.

What this means is that while Russia itself can’t manufacture the materiel for a protracted local conflict with Europe, China can manufacture enough to sustain both itself and Russia in a conflict between the two blocs I’m envisioning here.

Specific economic capabilities

“The North can make a steam engine, locomotive, or railway car; hardly a yard of cloth or pair of shoes can you make.” - William T. Sherman

The manufacturing comparison in the previous section was pretty broad; the total value added figure leaves out lots of important stuff. It doesn’t tell us how technologically advanced a country’s weapons systems are. It doesn’t tell us what percent of manufacturing capacity could be repurposed to military uses.

And most importantly, it doesn’t show how complete a country’s supply chains are. If you go into a war with manufacturing companies that depend on the enemy countries for critical components, it doesn’t matter how much value-added you produce in peacetime — your factories will grind to a halt. Value added is calculated on the margin, in peacetime, while wartime manufacturing capability is inframarginal — it’s the amount you can make after wrenching changes close you off to your peacetime supply chains. During the early Covid pandemic, the U.S. painfully rediscovered this principle when it found itself unable to make enough masks, Covid tests, or ventilators. But later in the pandemic, the U.S. had the advanced biotech supply chains to pump out huge amounts of mRNA vaccines, while China was the one to struggle.

Thus, it’s very hard to tell which supply chain pieces will end up being the choke points in a conflict. This is why the Biden administration is working feverishly on this problem, and I’m sure the Chinese authorities are doing the same. But there are a few things we can probably predict will be important.

First, fuel. (At this point I’ll stop doing the stacked bar charts and just show a map.) We can see that both of the posited blocs would have ample access to oil:

Coal is a similar story — China and Russia have plenty, but so do the U.S. and Australia. Gas is also roughly similar.

So on paper, both blocs have enough fossil fuels. For the New Axis, the question would mainly be whether Russia can get enough oil and gas to China — it would involve either moving a lot of tankers through potentially contested waters, or building a ton of very expensive difficult pipelines across the vast expanses of Eurasia. Of course, the U.S. would face a similar problem getting oil, coal and gas to its allies in Europe and Asia.

Of course, fossil fuels aren’t the only type of energy out there. There’s also renewables. Carting around the energy from renewables requires a lot of batteries (and maybe some electrolyzers), which requires a lot of minerals. David Roberts has a good breakdown of mineral requirements for alternative energy, with some good charts showing where the minerals are located. Graphite and rare earths are concentrated in China, while cobalt and platinum are concentrated in Africa:

Of course, this is just current production. The U.S. and its allies will probably be able to develop domestic supplies of rare earths and graphite if they have to, just as Japan started mining rare earths when China cut it off. But finding and exploiting these resources takes time, so the New Allies should probably be looking at this right now.

Then there’s the question of where the minerals are processed. Here we see that the answer is mostly “China”:

This seems like a real vulnerability for the New Allies. My suspicion is that there are a lot of other basic, “primary industry” type of tasks that developed countries have lazily let migrate en masse to China because they aren’t very high up the value chain. But in a conflict situation, “high up the value chain” suddenly means a lot less.

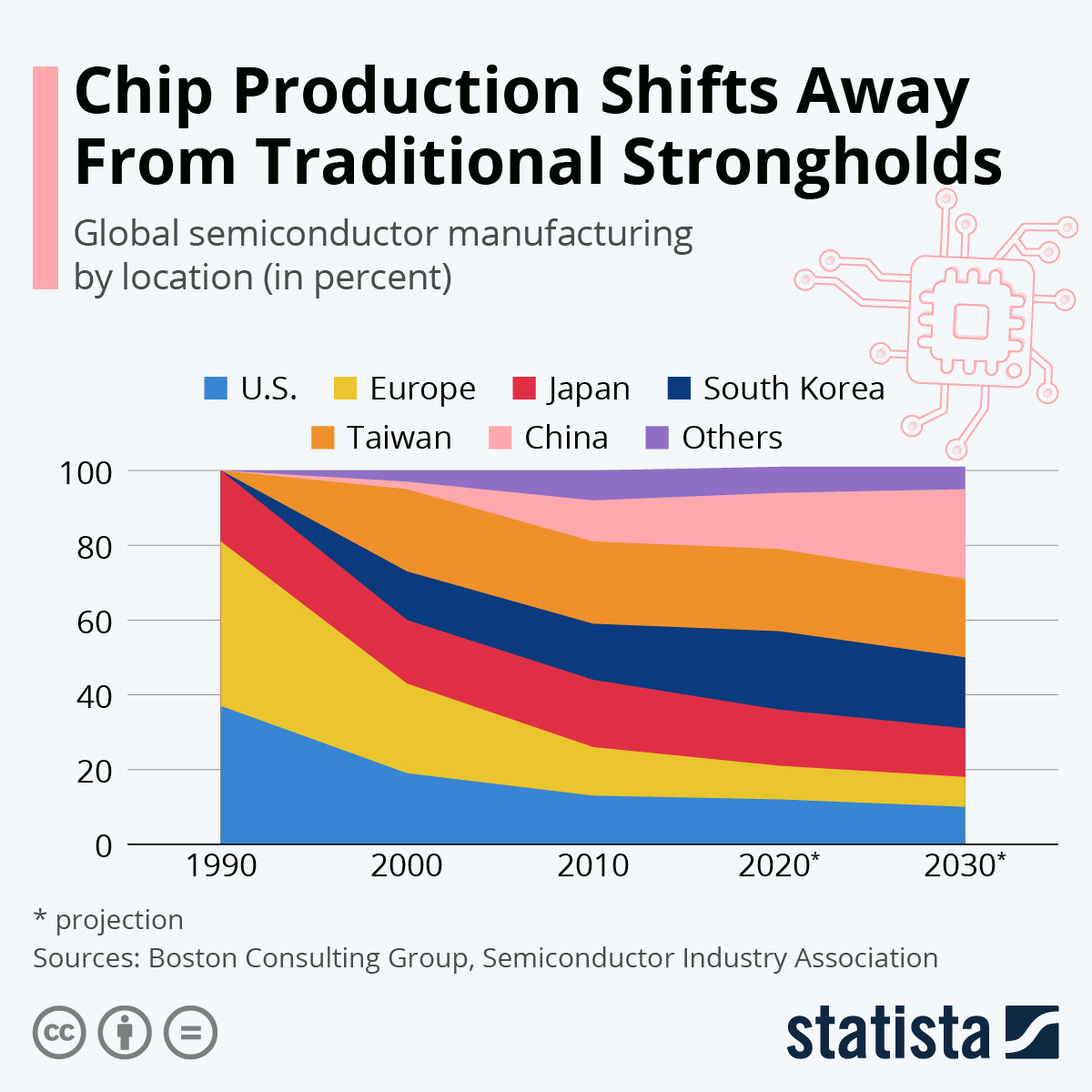

Semiconductors — i.e., computer chips — are an additional consideration. “Chips are the new oil”, as they say, which means that semiconductors are used in pretty much every piece of machinery. That includes all the machines of war and war production. Currently, the New Allies produce most of the semiconductors in the world, though China is racing to catch up:

But despite China’s mightiest efforts, this looks like an area where the New Allies will maintain a decisive advantage over the next decade.

In general, what looking at supply chain choke points shows us is that neither the New Axis nor the New Allies represents a fully self-contained, integrated economic machine that can make everything it needs for a major conflict. The past 20 years have seen China and the old industrialized nations develop a symbiotic relationship — they are deeply intertwined. (One would hope this would be enough to prevent a conflict, but that’s almost certainly wishful thinking given past experience.)

What that means is that in the event of a conflict, each bloc would be scrambling to shore up its weak points — China scrambling to build more chip fabs and secure more oil from Russia, the U.S. and Europe and Japan scrambling to rebuild the low-value primary industries that they outsourced to China.

The stiffest economic competition ever

I can’t say whether or not the New Axis is the most formidable military competitor that the U.S. and its allies have ever faced. The original Axis was certainly fearsome, and the USSR had tens of thousands of nuclear weapons ready to roast the world at the touch of a button. But I think that the comparisons above show that the New Axis certainly represents an economic competitor like none the U.S. and its allies have ever faced. And the reason is simply China. Russia is mainly a gas station with nukes. But China has three things going for it:

{kind=link}

China has far, far more workers than the original Axis or the Soviet bloc.

China has advanced manufacturing technology that probably rivals the original Axis in relative terms, and far exceeds the Soviet bloc.

China has the world’s largest manufacturing cluster, making it the “make everything country”, which neither the Axis nor the USSR managed to be.

This is simply a unique situation in modern history. The Industrial Revolution began in Europe and spread to the U.S. and the East Asian rim. The aftermath of WW2 saw central Europe and the East Asian rim incorporated into a U.S.-led alliance that dominated global manufacturing in a way that the communist powers could never threaten. Now, with the rise of China, world manufacturing is divided roughly in two.

Much of the War Economy in the U.S. (and its allies) will therefore be about rediscovering the manufacturing capabilities they neglected during China’s meteoric rise.

In the short run, Russia is important. In the long run, Russia is China's gas station.

Ironically, I think the Ukraine invasion has hurt China's strategy almost as badly as Russia's. Yes, Ukraine currently distracts our attention from China. But it's also taught everybody, especially Europeans, that dictators still launch stupid wars, and democracies still have to deter them from trying.

Thanks to Putin, a Chinese invasion of Taiwan no longer sounds like a ridiculous hypothetical to Europeans, a catastrophic Chinese stranglehold on a key economic resource sounds awfully familiar to them, and Europe doing their part to deter China isn't a crazy idea that has to be killed in committee.

In other words, by legitimating fears of a "New Axis," Putin may have done more for anti-Chinese unity and deterrence than any American President.

1. Reshore as much as possible

2. Much more immigration, especially STEM

3. 1 billion Americans

That will win. Can we do it ?