Xi Jinping vs. macroeconomics

Macro will not be mocked, sir.

I haven’t written about China’s economy in a while, so let’s take a break from constant election-blogging to talk about that.

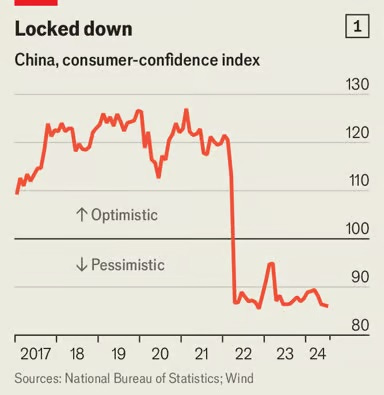

Recently, most of the discussion about the Chinese economy in the English-language media has been about the Second China Shock — the flood of Chinese manufactured imports. But inside China, there’s an entirely different story playing out — a protracted economic slowdown. China’s online boosters may gush about how high-tech and modern China is, and how wonderful its products are, but Chinese people themselves are very unhappy about how their economy is doing right now:

Chinese people have good reason to be glum here — despite all the shiny new EVs and delivery robots, the country’s economy is not doing great overall. Good data on the Chinese economy is hard to come by nowadays, and official numbers are probably even more iffy than usual, but what we can see looks underwhelming:

China’s economy probably failed to turn the corner on its worst stretch in five quarters, with an uneven recovery in July held back by consumer spending…Data due Thursday will show retail sales remained sluggish…And in another sign of growing weakness, the official manufacturing purchasing managers’ index indicated a third straight month of contraction in July, while a private survey on manufacturing PMI shrank for the first time in nine months…A rise in inventory levels at Chinese steel mills, alongside weak production, also points to frail demand.

Forecasts for China’s growth are inching downward, with government rhetoric growing less confident. (Recall that official growth numbers can be greatly overstated, particularly in bad economic times.) Youth unemployment, which had gotten so bad that the Chinese government changed the methodology to show a lower number, has nevertheless increased again to 21%.

The Chinese stock market, meanwhile, is very much in the dumps:

A deepening selloff in Chinese stocks is exacerbating a crisis of confidence…Down almost 7% this year, the CSI 300 Index is staring at an unprecedented fourth annual drop, while an MSCI Inc. gauge of Chinese stocks is heading for its longest stretch of underperformance versus global equities since the turn of the century…China’s poor performance is in stark contrast to a bull run in global stocks this year, underscoring investors’ skepticism towards Xi’s vision of China.

Stocks are not the best predictor of future economic activity, but in the absence of more reliable economic data from the government, they’re a useful proxy.

So what’s wrong with China’s economy? If you don’t live in China, your answer might be “Who cares?”. But I think it’s both interesting and important to think about the causes and the cures of problems like the ones China is having now. And China’s maroeconomic weakness is also one reason why its companies are dumping cheap products in markets around the world.

So anyway, let’s dive in. First, let’s talk about the two fundamentally different theories of why recessions happen, and why Xi Jinping has probably latched onto the wrong one.

Two theories for why China’s economy is doing badly

As everyone knows by now, the fundamental driver of China’s economic malaise is a real estate bust that has been going on since 2021:

But why would a real estate bust make the whole economy do badly? Stories about the problem cite massive ghost cities and vast inventories of unsold homes. But why should unsold homes reduce economic activity? GDP is a measure of current economic activity, not a measure of stuff that was built in the past. The existence of an unsold house doesn’t physically stop workers and companies from producing something today or tomorrow. Just tear it down, or ignore it, and go produce something else!

There are basically two stories about how this could work, and they correspond to two different understandings of what a '“macroeconomy” even means. These two ideas have basically been at war for a hundred years.

The first story is that there basically is no “macroeconomy”. You have various industries — autos, real estate, food, etc. Each of those industries has its own supply and demand, its own costs and technology and productivity levels, etc. The economy will just produce the sum of whatever all those industries can produce, and people will buy it for some price.

If that’s how things work, why would problems in the real estate industry hurt the rest of the economy? Well, one possibility, suggested by “Austrian” economists like Friedrich Hayek and Ludwig von Mises, is that there’s some real cost to reallocating resources from one industry to another. If real estate is 29% of your economy, and people decide they don’t want as many houses as you thought they would, then it takes time and money to shift workers and capital over to manufacturing. Those costs are big enough that they show up as an economic slowdown.

A second possibility, suggested by “Real Business Cycle” theorists like Ed Prescott, is that the slowdown in real estate is part of an economy-wide “productivity shock”, where technology and institutions start improving more slowly, or even get worse. In China, the obvious cause for that would be Xi Jinping himself, who crushed the startup industry, cracked down on real estate, and generally increased Chinese state control and interference in the economy by quite a bit.

You could call explanations like this “supply-side” theories (if that name hadn’t already been taken by something considerably less serious). But I think it’s a bit deeper than that. These theories basically say that there is no macroeconomy as such — that you’re really just dealing with the microeconomics of a bunch of individual industries. In fact, Ed Prescott famously refused to use the word “macroeconomics”, instead calling it “aggregate economics”, in order to express his belief that there was nothing special happening at the level of the overall economy.

My impression is that Xi Jinping and his followers believe in something along these lines. Xi’s response to China’s growth slowdown has been to try to shift real resources out of the “bad” sector (real estate) and into a sector he thinks is “good” (manufacturing). The Economist has a good description of what he’s trying to do:

China’s response [to its economic slowdown] is a strategy built around what officials call “new productive forces”. This eschews the conventional path of a big consumer stimulus to reflate the economy (that’s the kind of ruse the decadent West resorts to). Instead Mr Xi wants state power to accelerate advanced manufacturing industries, which will in turn create high-productivity jobs, make China self-sufficient and secure it against American aggression. China will leapfrog steel and skyscrapers to a golden era of mass production of electric cars, batteries, biomanufacturing and the drone-based “low-altitude economy”.

If the Chinese economy’s problem is that it’s having trouble figuring out what to do instead of real estate, well, Xi will simply resolve that dilemma, by telling everyone to go build cars and drones and other high-tech manufactured goods. If the problem is a negative productivity shock, well, Xi thinks his industrial policies will turbocharge productivity.

This isn’t the kind of policy that Friedrich Hayek or Ed Prescott would have recommended — they were libertarians and strong opponents of central planning. But if you believed in a Hayekian or a Prescottian story of recessions, and also believed in the wisdom and vision of the Chinese Communist Party, then this is exactly the kind of policy you’d try. Xi Jinping Thought, at least as it applies to recessions, is basically the fusion of an Austrian diagnosis with a communist cure.

But there’s a second theory of why recessions happen, which Xi seems to be completely ignoring.