The Roaring 20s are back on track

A healthy economy, strong productivity growth, and a continuing tech boom.

When I started this blog at the end of 2020, one of the big ideas going around was that we were headed for a “Roaring 20s” decade. Productivity had soared during the pandemic, and some of us predicted that companies were finally reshaping their business models around the internet. The success of MRNA vaccines, combined with the stunning drops in the cost of solar power and batteries, seemed like harbingers of a decade of rapid technological progress. The U.S.’s bipartisan willingness to spend big during COVID, and the bipartisan push for industrial policy, suggested that the government might finally stop sitting on its hands as well. And of course all of that was before the release of ChatGPT and the generative AI boom.

In the years that followed, that burst of optimism was tempered by high inflation, sluggish productivity growth, and the reversal of some of the business innovations that had taken hold during the pandemic. Attention shifted to war, geopolitical tensions, culture wars, and other less pleasant stuff. But over the past year or so, the Roaring 20s have quietly been making a comeback.

Productivity is growing again

First, let’s look at productivity. Labor productivity — just real GDP per hour worked — was in the dumps in 2021 and 2022. But recently it’s been on an uptrend, and last quarter’s productivity growth rate was higher than anything we’ve seen in a decade, other than the pandemic itself:

This rapid productivity growth, along with full employment, is why the U.S. might now be growing faster than the People’s Republic of China, for the first time in several decades.

Why is productivity growing more robustly? In fact, this is always a hard question for economists to answer. One theory is that when an economy is at full employment, businesses invest more in adopting new technologies and improving efficiency — both because they’re flush with cash from the booming economy, and because with workers being very scarce, they need to find other ways to meet high demand. So we might be seeing that now. Some economists argue that remote work is having an impact; more workers now save both time and money on commuting costs, and a few are able to move to cheaper locations. And of course, cheaper oil helps.

Will the productivity boom last? As you can see from the graph above, the quarterly numbers tend to be pretty volatile; the line might go back down in the coming months. But this burst of productivity is encouraging for two reasons.

First, productivity tends to jump up in recessions, because the less-productive (i.e., lower-paid) workers tend to get fired first, and because companies tend to work the remaining employees harder. This explains at least part of the big jump during Covid. That’s not the kind of productivity we really want, though; we want the kind that comes from better technology and better business models. And so what we really want to see is rapid productivity growth and full employment at the same time.

Which is what we’re now seeing.

Second, productivity growth is what allows wages to rise without stoking inflation. If you have wage hikes without productivity growth, eventually those extra dollars in people’s pockets will probably end up bidding up the price of consumer goods (a “wage-price spiral”). Rapid productivity growth means that the Fed can bring down inflation safely without hurting wages.

A disinflationary boom: the Goldilocks economy

And indeed, this is exactly what is now happening; inflation is coming down and wages are rising. Measured month-over-month, headline inflation was just 0.5% in October, while core inflation was 2.7% — pretty normal for the low-inflation pre-pandemic period.

Other measures of inflation look good too.

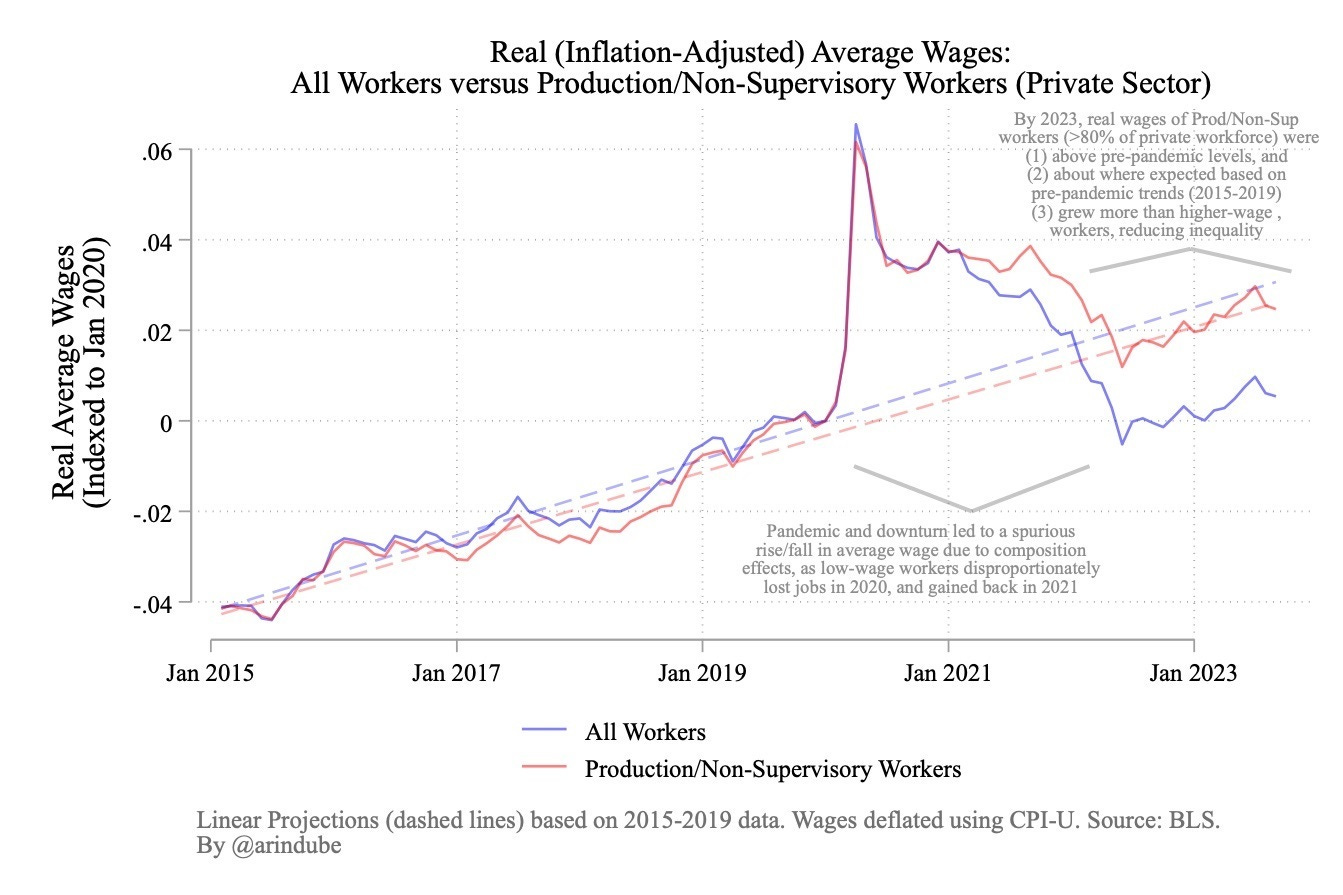

And falling inflation is allowing real wages to rise. Here’s a chart that I posted in my weekly update:

Whether wages are back on their pre-pandemic trend isn’t yet clear, but they’ve definitely been rising for a year now, and we have falling inflation to thank.

Of course, falling inflation doesn’t mean prices go back down to where they were. So it’ll probably be a while before people get used to the new higher numbers, and the fact of falling inflation really hits home. But that said, a few prices actually have gone back down, like the price of gasoline, which is now at about the same level as it was 10 years ago:

Why did inflation fall? The two main theories are:

1) The Fed’s rate hikes lead to lower inflation expectations, which became a self-fulfilling prophecy, and

2) The economy simply worked out the supply-side kinks from the pandemic and the early days of the Ukraine war.

It’ll be a while before we have any idea how much each these two factors contributed, but what we do know is that together, they worked.

It’s also important to recognize the “dog that didn’t bark” here — decoupling from China. Western investment into China has plummeted, but there’s no sign yet that this is causing higher prices. Our dependence on the “China price” to make our consumer goods cheap is a thing of the past.

Anyway, low inflation and full employment together combine to form the most sought-after of macroeconomic beasts: the disinflationary boom. In this Goldilocks situation, the economy faces no tradeoff between stable prices and a great job market. And given the fact that the job market is now about as good as it ever gets, that’s where we are right now.

Oh and by the way, in case you were wondering whether current economic conditions are just a “sugar high” caused by increased government spending: No, that is not what’s going on. If that were true, we’d see more inflation right now (as we did in 2021). Also, note that government spending as a percentage of GDP has fallen back to about where it was in the 1980s:

Biden’s industrial policy might be giving the economy a boost, but if so, it’s doing it by “crowding in” private investment, not by spending the money directly.

Of course, a lot of people are asking: Given these great economic conditions, why are Americans so pessimistic about the economy? And one potential answer is: Just wait, they will be. It probably takes some time and persistent messaging in order for positive economic conditions to make their way into people’s consciousness. For what it’s worth, Biden’s approval rating on the economy seems to be improving steadily, and consumer sentiment has risen quite a bit from its lows a year ago.

The 20s tech boom

The “Roaring 20s” idea wasn’t just about a strong economy; it was fundamentally about a technology boom. And although it’s hard to identify the impacts of technologies on the economy, I think there are signs that some of the things we were excited about three years ago are now having an effect.

First, there’s remote work, which I already mentioned. So far, it looks like fully remote work lowers productivity, but allows people to live in cheaper areas, while hybrid work keeps productivity the same while cutting down on commuting costs. This means work-from-home is already cutting costs, and that businesses have improved their ability to use remote work quite a lot from the early pandemic days.

Also, consider MRNA vaccines. Although vaccines for cancer, malaria, and other diseases won’t start having a macroeconomic impact for a while, Covid vaccination probably did. The percentage of Americans age 18-64 receiving Social Security Disability payments was only 3.9% in 2022, compared to 4.8% in 2013. Vaccination reduces the severity of Covid, which likely prevents long-term disability due to lung scarring.

Then there’s the progress in solar power and batteries. Eventually, this will make electricity a lot cheaper than it was before, allowing businesses to lower costs and liberating them from the notorious wild swings of fossil fuel prices. That will increase productivity. For now, though, solar is only 6% of U.S. electricity generation, so drops in solar costs are, for now, just a percent of a percent — too small to influence overall electricity costs much. And EVs are only 1% of the auto fleet.

But these technologies are cheap enough to influence business investment. U.S. businesses invested $25 billion in solar alone in the first half of 2023. $200 billion of investment in EV manufacturing has been announced in the U.S. so far. That’s helping to support the robust private-sector investment that’s keeping the country at full employment.

Another technology driving rapid corporate investment is AI. AI is rapidly taking over the world of venture finance, with more than a quarter of VC money now flowing into the space. That’s partly a result of more traditional startup categories going bust, but mostly it’s about the boom in generative AI following the release of ChatGPT and various AI art apps. Goldman Sachs predicts that AI investment could be 4% of the economy in just two years. Boardroom chaos at OpenAI seems unlikely to slow the trend much, since the basic technology of LLMs is now pretty widely diffused.

And that’s just today. It’s crucial to note that all of these technologies — new wonder vaccines, solar and batteries, and AI — will almost certainly have a much bigger impact once they’re widely adopted. Generative AI will juice productivity in ways we can’t even imagine right now. Cheap solar and batteries will push down electricity and transportation costs. Using vaccines to treat cancer will reduce disease burden. And further business-model innovations will hopefully allow companies to use work-from-home to greater advantage.

In other words, the Roaring 20s are just getting started.

Much of the country is still mired in the atmosphere of pessimism and malaise that followed the Great Recession, the chaotic Trump years, the pandemic, and the post-pandemic inflation. And of course dire events like the Israel-Gaza war continue to dominate headlines. But already I feel like I can sense the green shoots of excitement about the future, from the online “e/acc” mini-movement to nascent optimism about the economy.

Now all we have to do is quash the NIMBYs, and we’ll be good.

Yeah, you're probably right dude. But it takes a decade to realize the last one was good. Taibbi and Kern were punching against this narrative this week, but it will likely work out like this.

My students now have prospects that were hardly a dream ten years ago, and this is in a D2 school. They're getting snapped up like candy by corps who want to "train to standard", which means they're going to be killers in the market five years from now once they have their legs beneath them. As someone like you who had to knife it out in the early 2000s (pre-crash), I'd trade a whole bucket of my education for their opportunity now.

If you want to be in the office and make connections now, the world is yours for the taking in the USA. If you wanna gripe on TicToc or X about affordable housing and flexible work schedules, then you're entering a seller's market.

The next gen is getting it. America is going to be incredibly strong.

This coming from an unapologetic, apathetic Xer who thinks generation theory is complete BS baked up by some posers who didn't do the math (or the reading) and just needed to rimshot tenure.

Regarless, I'm optimistic. Keep up the good work bud.

Labor shortages and high wages drive productivity growth. It’s actually in businesses long term interests not to have labor that’s too cheap.