Japan can be America's arsenal

A guest post by Rie Yano.

{kind=link}

I just came back from Andreessen Horowitz’ American Dynamism Summit in Washington, D.C. It was very refreshing to see so many smart people invested in both American reindustrialization and American defense.

One interesting theme I noticed at the conference — and which I was eager to talk about — was U.S. manufacturers building factories in Japan. Many American manufacturers — both startups and big companies — already do lots of sourcing in Japan, but now some are starting to realize that Japan is a good production base as well. That was the subject of my first book, so it’s a topic near and dear to my heart.

So I thought this would be a good time to publish a guest post by Rie Yano, a friend of mine who is a San Francisco-based partner at the Japanese VC firm Coral Capital. Rie’s very timely post is all about how Japan is the perfect place for the U.S. to do lots of defense manufacturing. In fact, I think there are some advantages of Japan that she didn’t even mention — such as the incredible ease of bringing foreign skilled workers into Japan, now that the country’s immigration policy has been reformed. But in any case, it’s a very good post.

The United States faces a defense-industrial problem that money alone can’t solve. Even though reindustrialization is now supposedly an American national priority, there are hard limits to what the U.S. can actually build, repair, and replenish at scale.

Shipyards are backed up for years. Munitions production is thin. Advanced manufacturing talent is aging out faster than it can be replaced. And even when funding is approved, production timelines don’t move fast enough to match today’s threat environment.

Government reshoring initiatives help at the margin, of course. But new industrial capacity in the U.S. takes years to permit, and remain vulnerable to litigation even after regulatory approval.

Meanwhile, China’s mighty industrial machine is firing on all cylinders. While U.S. reshoring efforts ramp up from a cold start, and while U.S. manufacturing relearns how to produce at scale after decades of neglect and stagnation, China is rapidly surpassing the U.S. in the production of ships, submarines, missiles, drones, and ammunition.

To move faster, the U.S. can’t go it alone. It needs a partner — a place where it can manufacture defense equipment while it ramps up its own industrial base. That partner needs three essential characteristics in order to get started producing right away: industrial depth, political stability, and speed.

Taiwan, under threat of invasion, is increasingly risky as a manufacturing base. Europe is fragmented and geographically distant from the Indo-Pacific, and has Russia to occupy its energies. Canada lacks high-throughput manufacturing scale, while Mexico lacks the precision and complexity that modern defense systems require. India is still early in its technological catch-up phase.

That leaves Japan and Korea — of which Japan is far larger. Fortunately, over the next two years, Japan plans to increase defense and industrial capacity more than at any point since World War II:

Japan possesses world-class manufacturing capability, elite engineering talent, and strong IP protection. And for the first time in decades, it has a political mandate to move fast - especially given Prime Minister Takaichi’s recent landslide victory. Projects like Rapidus and TSMC’s advanced fabs in Kumamoto aren’t isolated investments. They’re signals that US-Japan industrial integration is becoming a strategic necessity.

A deeper industrial partnership between the U.S. and Japan is such a huge opportunity that in retrospect it will seem inevitable. American defense companies that understand how to build with Japan will win.

Japan Is Rearming

For eighty years, Japan effectively outsourced its defense to the United States. The countries leaders have realized that that model has become untenable. First, the regional security environment has tightened fast. China’s military expansion, North Korea’s missile launches, and Russia’s activity in Northeast Asia have collapsed the assumption that the status quo could continue.

Second, the United States is no longer willing or able to carry Asia’s industrial defense load alone. At a moment when the U.S. defense industrial base is straining under production bottlenecks and labor shortages, allies that can actually build things matter more and more.

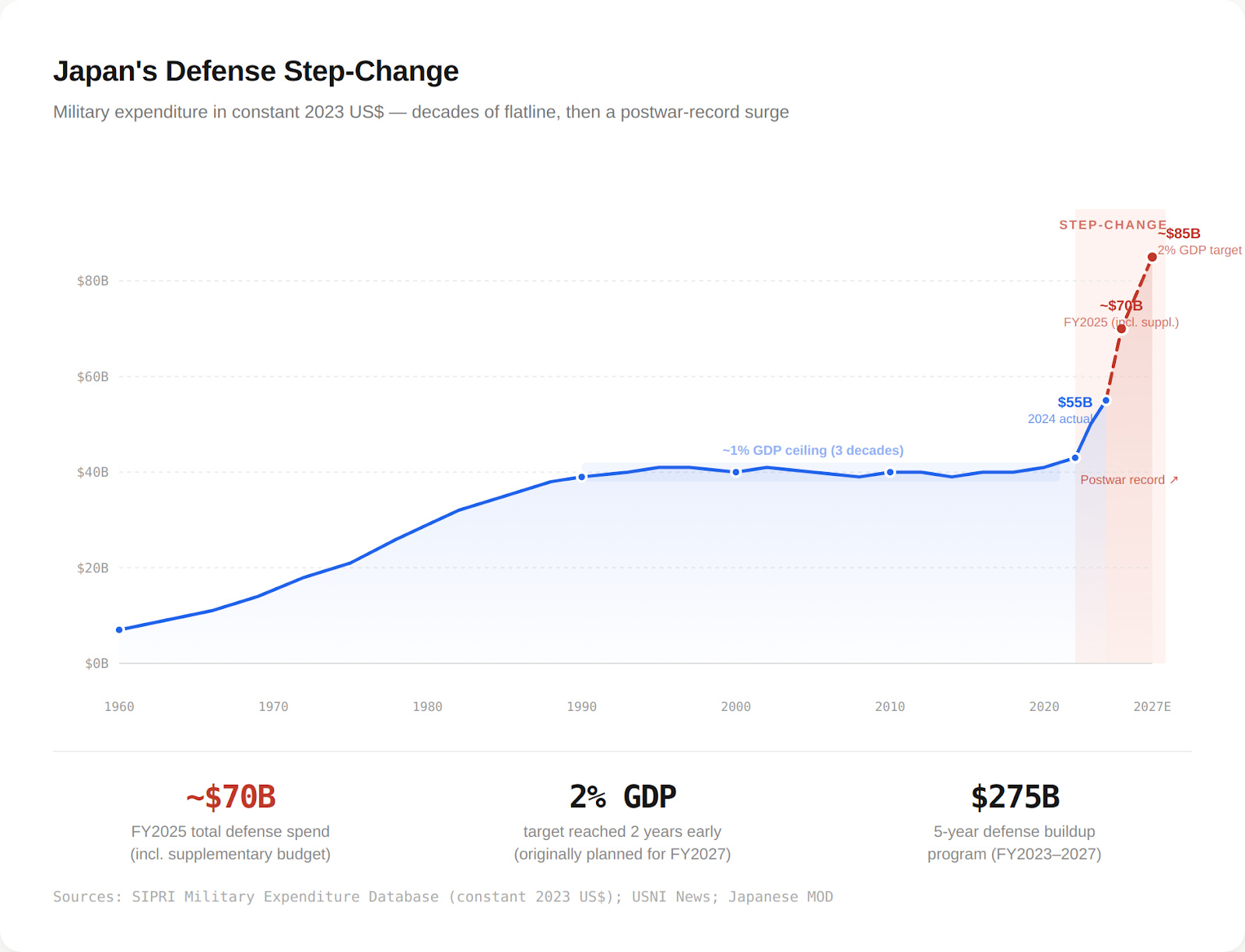

Third, Japan is now in the process of fundamentally changing how it mobilizes capital for defense. Military spending was effectively capped below 1% of GDP for decades. That constraint is now gone — Japan plans to reach 2% of GDP by 2027, putting it among the top global defense spenders by the late 2020s.

But in fact, this is only a piece of the story, and not necessarily the biggest one. Japan’s defense buildup aligns three levers at once:

increased defense spending

explicit industrial policy and subsidies

a willingness to use foreign direct investment as an accelerator

Regulations, procurement reform, and capital allocation are all being aligned to rebuild production capacity, not just fund programs. U.S. defense and deep-tech companies are being invited in as co-developers and co-manufacturers.

Poland is the Closest Playbook

When countries rebuild defense capability under time pressure, everything compresses. Capital deployment, testing, procurement, and industrial scale-up all happen faster than peacetime systems allow.

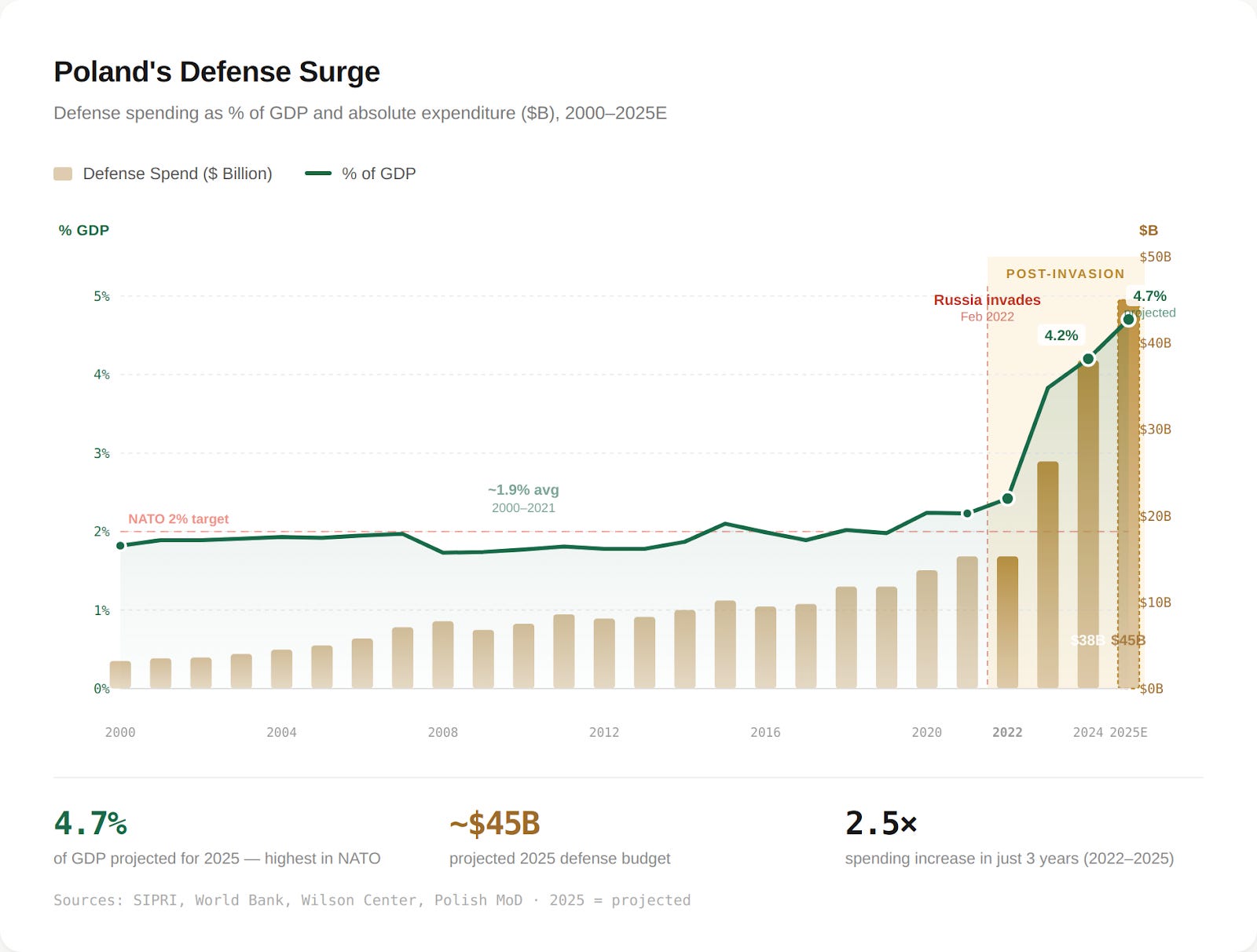

Poland is the clearest recent example:

Before Russia’s full-scale invasion of Ukraine in 2022, Poland was already spending about 2.4% of GDP on defense. Within two years, that figure surged toward ~4%, making Poland one of NATO’s highest defense spenders. Just as importantly, procurement timelines compressed from years into months, and domestic production ramped in parallel with acquisition instead of waiting for long planning cycles to finish.

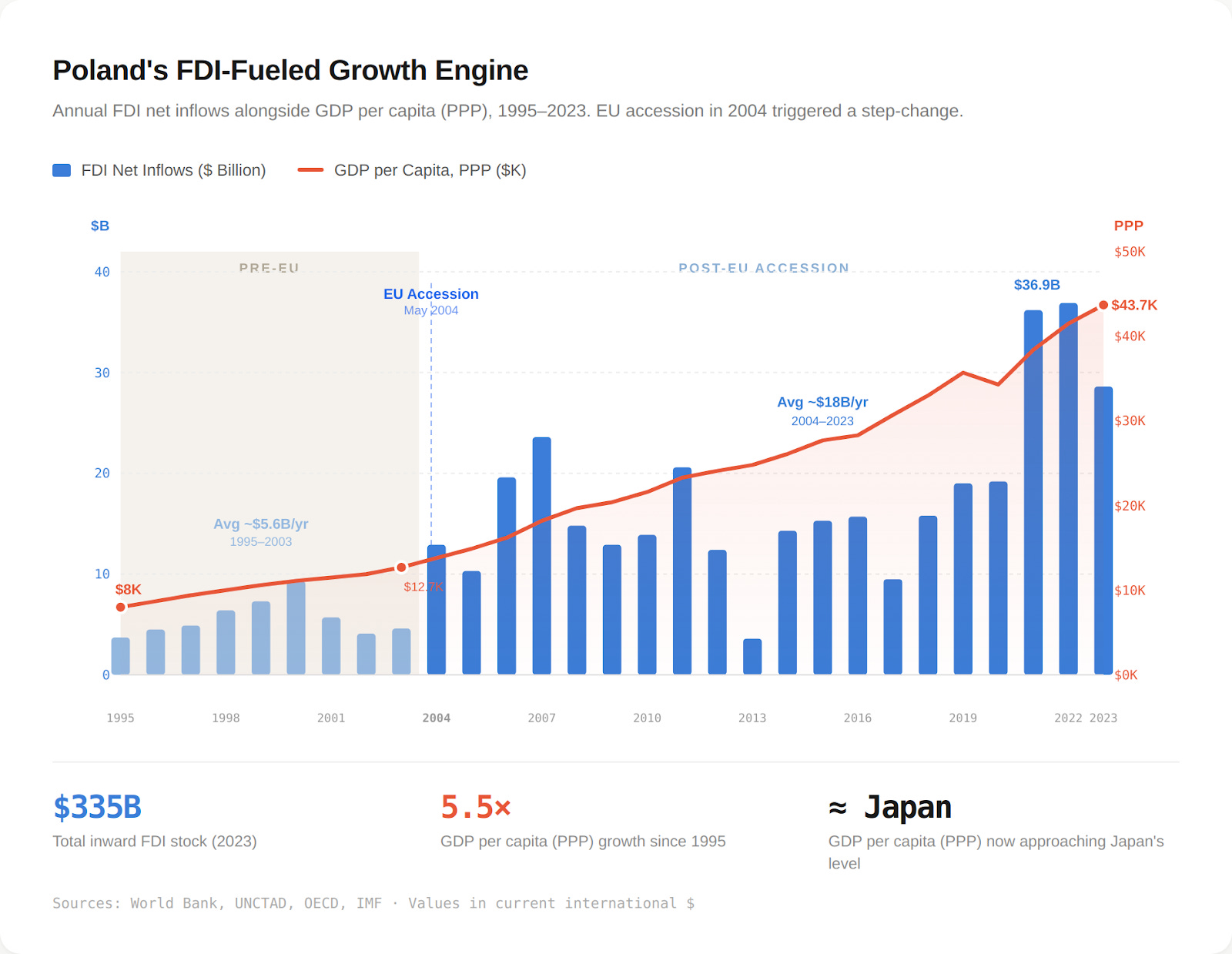

Crucially, Poland paired this with the foreign direct investment that has powered its economy more generally. Over the past two decades, annual FDI inflows exceeded $40 billion at peak, and the total inward FDI stock now surpasses $330 billion. Poland used this FDI not just to create jobs, but to import manufacturing know-how, scale its factories, and integrate itself into global supply chains. The result was rapid economic growth and industrial modernization — today, Poland’s GDP per capita (PPP) sits close to Japan’s, despite starting far behind in the early 2000s.

Japan is now signaling that it wants to do something similar. As of 2023, Japan’s inward FDI stock stood at about $350 billion, which is low for an economy of its size. The government has now set an explicit target to double that figure to $650-700 billion by 2030.

This represents a structural bet that foreign capital, technology, and operating know-how can help rebuild industrial capacity faster than domestic systems can deliver on their own. In fact, this is already happening. TSMC’s $17 billion investment in Kumamoto gave Japan advanced 3-nanometer chips processing technology, the most advanced foundry production outside Taiwan.

Meanwhile, Rapidus, despite being a Japanese semiconductor company, is explicitly designed to pull in global partners, frontier manufacturing tools, and non-Japanese know-how to rebuild advanced chipmaking capability quickly, rather than relying solely on domestic incumbents as Japan tried to do in the past. At Coral Capital, we wrote a piece about why the Rapidus development means that Hokkaido is the new Taiwan.

As the U.S.’ urgency for rearmament rises, Japan’s industrial scale-up matters — it means the U.S. now has a trusted allied capacity in Asia that can shoulder much of the defense manufacturing burden.

Japan Already Powers Critical U.S. Bottlenecks

A U.S.-Japan defense manufacturing partnership won’t be something created out of the blue; it’ll build on an industrial relationship that has existed for many years, to the benefit of both countries.

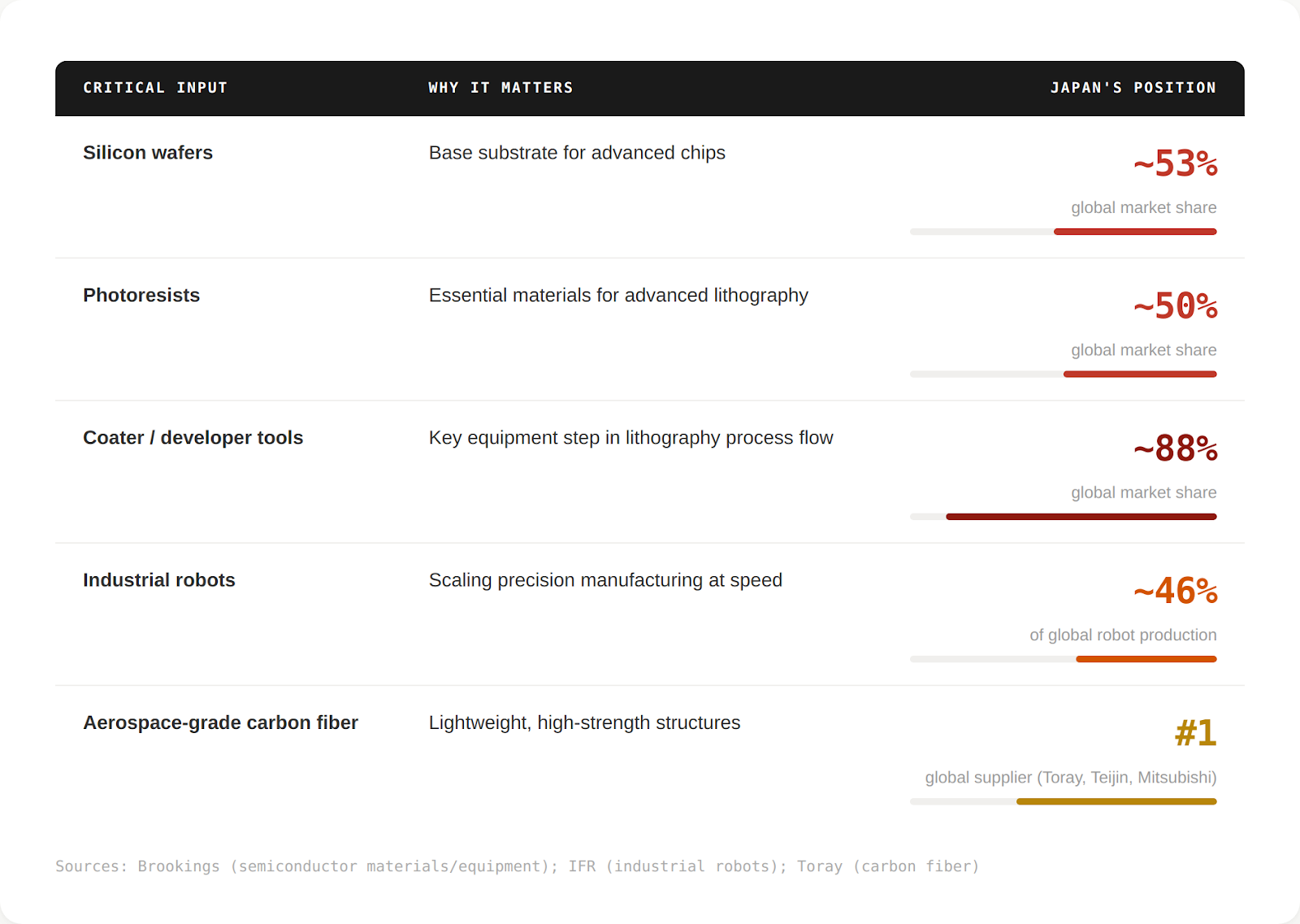

Right now, if you’re building hardware, deep tech, or anything that goes into defense or critical infrastructure at a significant scale, Japan is probably already in your supply chain — you just don’t always see it. Japan specializes in a number of upstream industries that help American companies scale:

Some key examples include:

Semiconductor materials: Japanese firms supply roughly half of the world’s silicon wafers and photoresists used in advanced chipmaking. Companies like Shin-Etsu Chemical and SUMCO sit upstream of nearly every advanced logic and memory fab, including those operated by TSMC, Samsung, and Intel in the U.S.

Advanced composites: Toray’s T1100 carbon fiber is embedded across U.S. defense platforms, including the U.S. Army’s Future Long-Range Assault Aircraft (FLRAA), one of the Pentagon’s most important next-generation aviation programs, and multiple Boeing and Lockheed systems.

Industrial robotics and automation: Japan produces almost half of the world’s industrial robots, led by companies such as FANUC, Yaskawa, and Kawasaki. As U.S. defense manufacturing runs into labor constraints, automation is becoming critical.

Shipbuilding and maintenance: While the U.S. Navy struggles with maintenance backlogs and unfinished repairs, Japan retains dense, high-throughput shipyard capacity with companies such as Mitsubishi Heavy Industries. The U.S. is already using Japanese yards for maintenance and overhaul of U.S. naval vessels in the Indo-Pacific.

Japan’s Surprising Advantages: Regulations and Labor

For U.S. hardware companies, the constraint over the next few years will be throughput - how fast you can stand up new capacity, qualify suppliers, and move from prototype to volume.

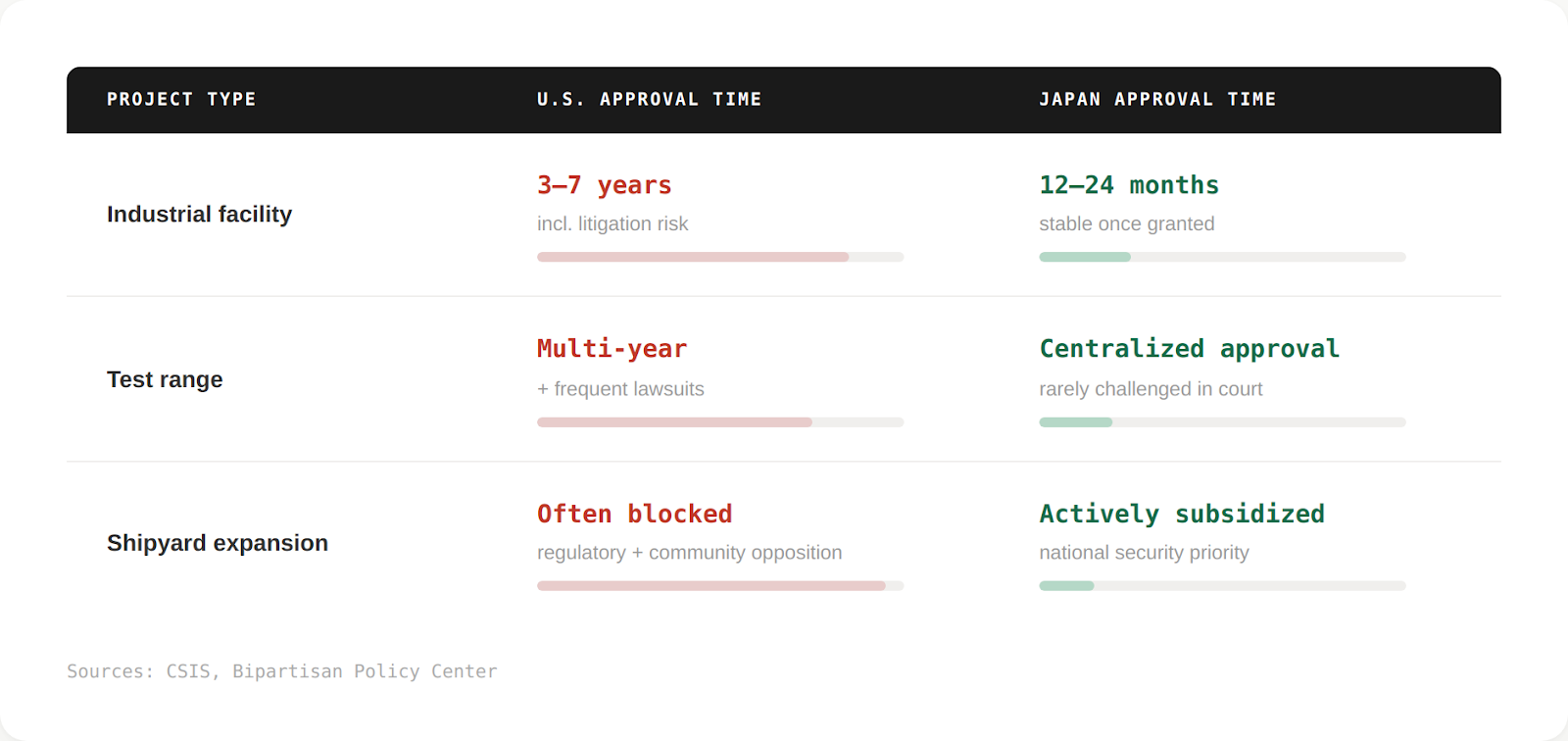

In the U.S., building physical infrastructure is slow and unpredictable. New factories, test ranges, and shipyard expansions often take years to permit and are frequently delayed by litigation, even after regulatory compliance. Three-to-seven year approval timelines are common.

In the long run, policy reforms can fix this situation. But for the foreseeable future, Japan offers a much more favorable trade-off. Japan’s centralized, bureaucratic regulatory approval process gets things built much faster than America’s more legalistic one. In the U.S., permits are often challenged in court, tied up for years in legal proceedings, and sometimes revoked. In Japan this almost never happens — once you get approved to build something, you can go ahead and build it. Capital-intensive infrastructure can thus be built quickly and operated with long-term confidence. On top of that, the government has explicitly defined defense-industrial capacity as a national security priority and is actively smoothing the regulatory path.

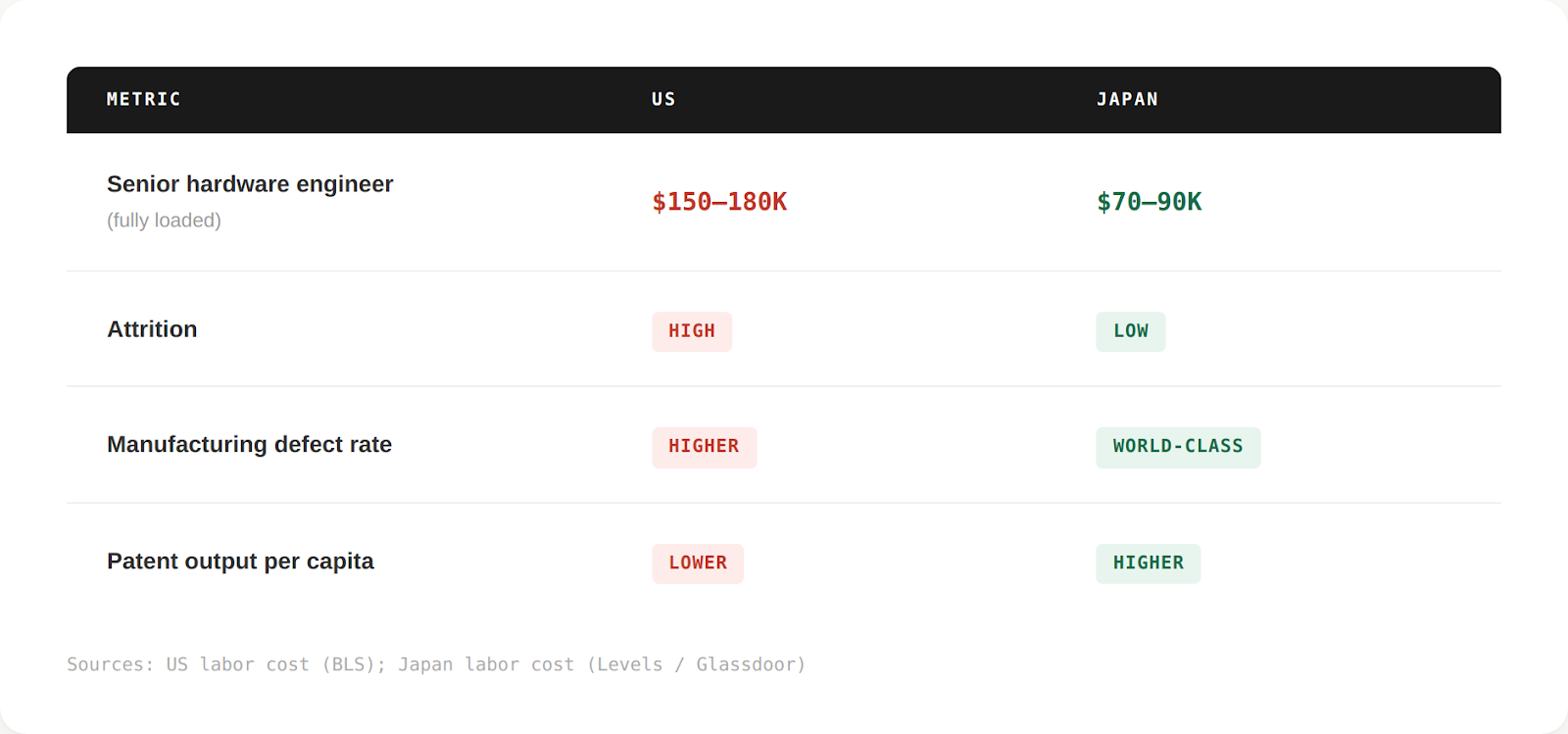

Labor is another big advantage. Senior hardware engineers in Japan often cost meaningfully less than in the U.S., but their real advantage is execution reliability. Lower attrition, tighter process control, a culture of discipline, and deep experience in precision manufacturing, materials, robotics, and systems integration translate into higher reliability at scale.

Japan also offers the opportunity for industrial scale without the strategic IP risk that hurt many multinational companies in China. After years of technology leakage and forced transfer in jurisdictions with weak IP protections, global players are understandably wary. Japan, however, has strong IP enforcement. It’s also a U.S. ally, so there’s no risk that a rival military will end up with American technology. The 2022 Economic Security Promotion Act and the 2023, U.S.-Japan Security of Supply Arrangement formalize that alignment. New institutions under the Ministry of Defense are explicitly designed to move commercial technology into defense deployment faster.

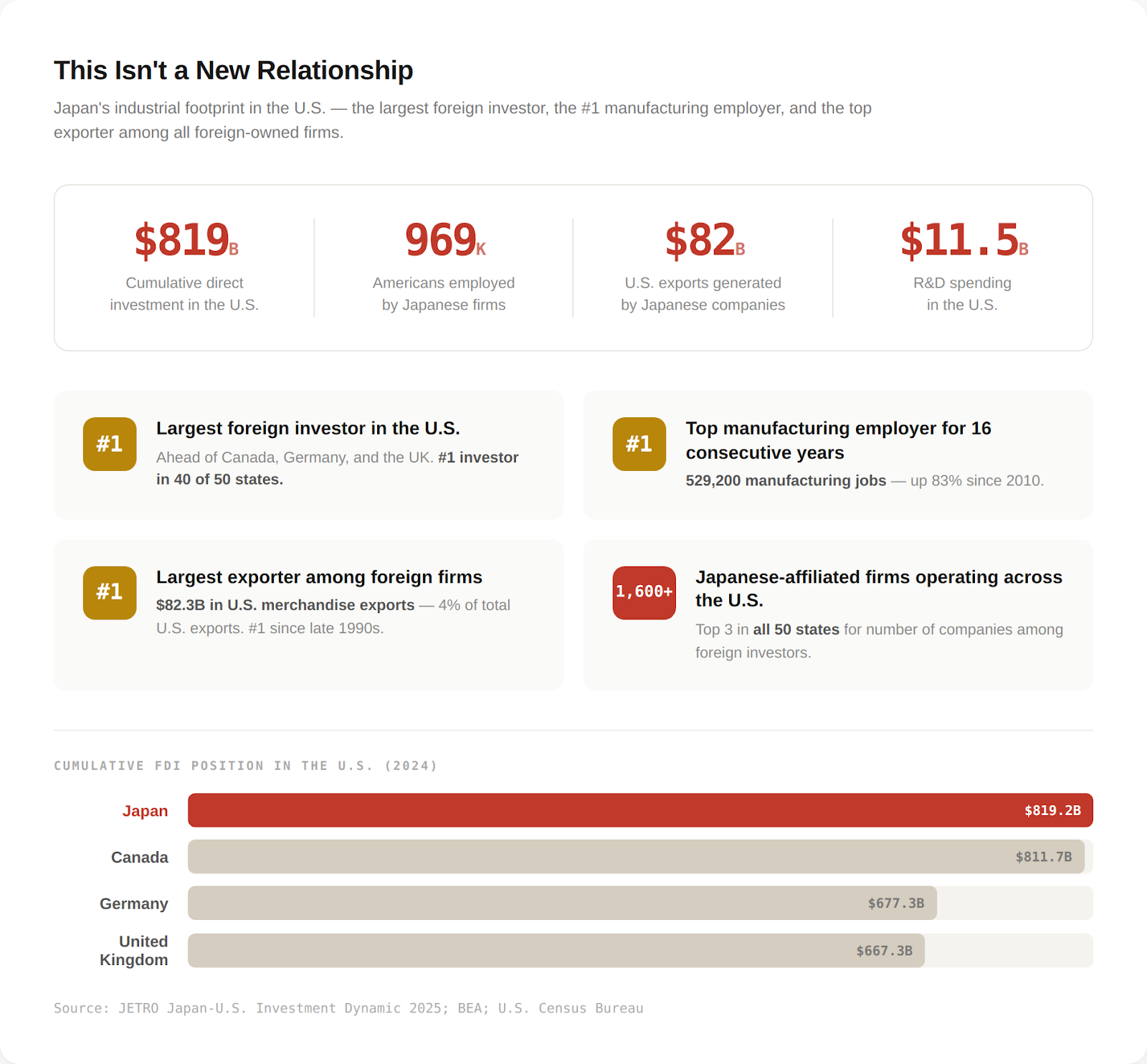

Anyone considering investing in Japan should be encouraged by the deep history of successful U.S.-Japan co-manufacturing. Japanese companies have spent decades building factories in the United States, training American workers, and helping Americans master production systems like Kaizen and the Toyota Production System.

Today, Japan is the largest source of foreign direct investment in the U.S., with roughly $800+ billion in cumulative investment and more than 1,600 Japanese-affiliated firms operating across the country. In roughly 40 states, Japan ranks as the #1 foreign investor.

In other words, the U.S.-Japan alliance has always been an industrial alliance, not just diplomatic. Now that model is being applied to defense manufacturing as well.

For the first time, Japan is treating industrial capacity itself as a national security asset. The 2023 Act on Enhancing Defense Production and Technology Bases formalizes that shift. New institutions under ATLA, including DISTI, are explicitly designed to shorten the path from commercial technology to defense deployment, including coordination with the U.S. Defense Innovation Unit.

In other words, Japan is now deploying the same playbook it once ran in autos, electronics, and semiconductors, now pointed deliberately at defense.

Builders: Seize this Moment

The United States, needs to reindustrialize, but it cannot reindustrialize alone. Japan is its arsenal, already embedded in the most critical layers of the U.S. industrial base, from materials and automation to ship repair and advanced manufacturing. What’s changed is that Japan is now explicitly opening those layers to deeper co-manufacturing and co-development, and doing so under time pressure.

This window will not stay open indefinitely. Early partners help shape standards, procurement pathways, and long-term relationships. Late entrants miss out and are forced to play catch-up.

Some companies already see this. Palantir’s Japanese operations have become one of its strongest international businesses. Anduril’s entry into Japan in 2025 reflects a strategic investment in the U.S.–Japan alliance. Last December, Anduril announced an agreement with a Japanese motor manufacturing company Aster to explore manufacturing and supply chain partnerships. These are early signals, not outliers.

The companies that understand how to build with Japan won’t just participate in the next phase of reindustrialization. They’ll define it.

| A guest post by

|

Tossing off Europe and other alternatives in a single sentence isn't convincing.

Yes, Japan's a great choice. But as Noah likes to point out, competing with China will be an 'all of the above' solution for the US. Europe has great shipyards, and they aren't occupied fighting Russia. Mexico and Canada are the most integrated into the American system, and Canada has shipyards, and mostly needs capital.

Trump pissing off 'all of the above' is of course the worst grand strategic posture the US has had in at least a century.

I'm not opposed to any of this. But the US needs to get our own damn house in order and make it easier to build here