Debt ceiling brinksmanship is terrible, but it is time for austerity

Raise taxes, focus spending on what matters.

Debt ceiling brinksmanship is pretty much the worst, most insane way to make fiscal policy. As Josh Barro points out, legislatively, there’s no point to it, since if Republicans want to stop the government from spending money, they can just refuse to approve government spending. They don’t need to also threaten to refuse to raise the debt limit. So it’s pretty bad that the GOP has gotten into the habit of taking this unnecessary step. At the very least, it makes the U.S. look like a dysfunctional, unstable, declining nation at exactly the point when countries all over the world are looking to us to provide a stable, dependable alternative to Chinese and Russian power. And if the threat turns out not to be an empty one, it puts us in danger of real, serious economic consequences — ultimately, not being able to keep borrowing would cause a U.S. sovereign default, which would throw the country into a very deep, years-long recession, wreak havoc on the entire global financial system, and result in a dramatic and permanent collapse of U.S. global economic clout. Banks are now predicting that the ceiling will be reached this June or July; that’s way too close for comfort.

In other words, whatever meager benefits Republicans think they could win from using debt ceiling brinksmanship to force spending cuts instead of just voting on a budget like normal legislators in a normal country, those benefits aren’t worth it. The next debt ceiling bargain should abolish the debt ceiling completely, or at least change the policy to make debt default no longer the…um…default outcome.

That said, the Biden administration absolutely should be negotiating with Republicans over spending cuts. The fact that debt ceiling brinksmanship is bad isn’t a good reason to treat the GOP like terrorists; that might feel like it’s tougher and more principled than Obama was in 2011, but really it just compounds the impression that U.S. governance is shaky. In fact, the U.S. does need some major fiscal policy changes, and these should be done in a bipartisan manner. It’s time for austerity, and for austerity to have legitimacy, it needs to involve things the Democrats would like (tax increases) and things the Republicans would like (spending cuts).

Why now is actually a good time for austerity

During the long recovery from the 2008 financial crisis and the Great Recession that followed, “austerity” became a dirty word — and rightly so. When a country is in a deep recession — and when interest rates are at the zero lower bound — fiscal stimulus becomes a much more effective and much more important policy tool. The idea that cutting deficits could fight a recession, called “expansionary austerity”, turned out to be very wrong. The U.S.’ embrace of fiscal stimulus in 2009 was part of what allowed it to recover from its crisis more quickly than Europe, where the memory of post-WW1 inflation made Germany and France reluctant to open their purse strings. The failure of austerity and the success of Keynesian policy was so clear that even the IMF, which had long been austerity’s chief cheerleader, experienced a sea change in its thinking.

That history is understandably going to make many people, especially Democrats, wary of calls for austerity now. But it’s not 2010 anymore. Macroeconomic conditions change, and that means that policy needs to change too.

Why is now different than the early 2010s? Well, to start with, inflation is high-ish now, and it was low back then:

In 2010-2015, core PCE inflation (which is what the Fed targets) was below the 2% target, while now it’s way above target.

In general, fiscal deficits are inflationary. Economists argue a lot about why this should be true. Some people argue that it’s just a Keynesian demand effect — when the government borrows money and gives it to people, either by spending or by tax cuts, people go out and spend some of that money, which boosts demand, which raises prices. Other economists endorse something called the “fiscal theory of the price level”, which basically says that people assume the government will inflate its debt away, so more debt means higher inflation expectations, which become a self-fulfilling prophecy.

People also argue about how big this effect is — in general, deficits seem to affect inflation much more in developing countries than in developed ones like the U.S. We all remember the example of how Japan’s government borrowed an unprecedentedly huge amount in the 1990s and 2000s, but remained mired in deflation. On the other hand, economists like Olivier Blanchard and Larry Summers correctly predicted that the deficits associated with the Covid relief spending of 2020 and 2021 would generate significant inflation in 2021.

So cutting deficits might have a significant effect on inflation, and it might not. And I should also mention that inflation is a less pressing worry than it was a year ago — the collapse of oil prices, and the looming effect of bank failures, mean that it’s not urgent to use austerity to help the Fed restrain inflation right now. But it’s far from clear that inflationary pressures have been defeated. And I think most economists would agree that if you’re going to cut deficits, you want to do it when inflation is high.

Austerity would also help the Fed do its job without hurting the banking system. Currently, deposits are being pulled out of banks in a “slow bank run” that may cause more banks to fail. A lot of mid-size and smaller regional banks are looking shaky:

Recall that banks are weak because interest rates are high. High rates lower the value of banks’ assets (bonds and loans), making it harder for them to pay depositors. And high rates also lure depositors away from banks, toward money market funds. Thus, the longer the Fed has to keep rates at 5% or higher in order to make sure inflation goes back to target, the more damage it will do to U.S. banks.

Congress can help the Fed out of this dilemma by doing austerity. Lower deficits would give the Fed more space to lower interest rates and save the banks without inflation bouncing back up.

The third reason to do austerity is because it’s now clear that at some point we’re going to have to. 15 or 20 years ago, it was easy to dismiss worries about Social Security “running out of money”, but as Vox’s Dylan Matthews reports, we’re finally reaching the point where slower population growth is going to force cuts in benefits:

[S]tarting in 2010, the program’s expenses began exceeding its tax revenue. Since then it has relied on the trust fund to pay benefits…The Congressional Budget Office projects the OASI fund, which funds old-age benefits, will run out of money in 2032; the Social Security trustees project this will happen in 2033. At that point, the program will only be able to pay out benefits based on the taxes it’s collecting — and it’ll be collecting about 20 percent less in taxes than it’s promising to pay out in benefits.

So in order to avoid major benefit cuts, we’re going to have to either raise taxes, cut other spending, or accept a long-term ever-rising structural budget deficit in order to pay for Social Security. And we’re not going to accept a long-term ever-rising structural budget deficit, because eventually that will lead to unsustainable inflation.

In other words, because Social Security is based on young people paying old people, and because we have fewer young people now, we’re eventually going to have to do austerity in order to make the system sustainable. So we might as well make those plans now.

There’s one other consideration regarding when to do austerity, which is interest rates. Ideally, the government wants to lock in low rates when it issues long-term debt. But 10-year Treasury yields aren’t actually that much higher than they were in 2010, and in inflation-adjusted terms they’re only a little over 1%. So rates aren’t forcing austerity yet.

Still, elevated inflation, a weak banking system, and a shaky long-term government fiscal position seem like reason enough to cut deficits somewhat.

What an austerity bargain might look like

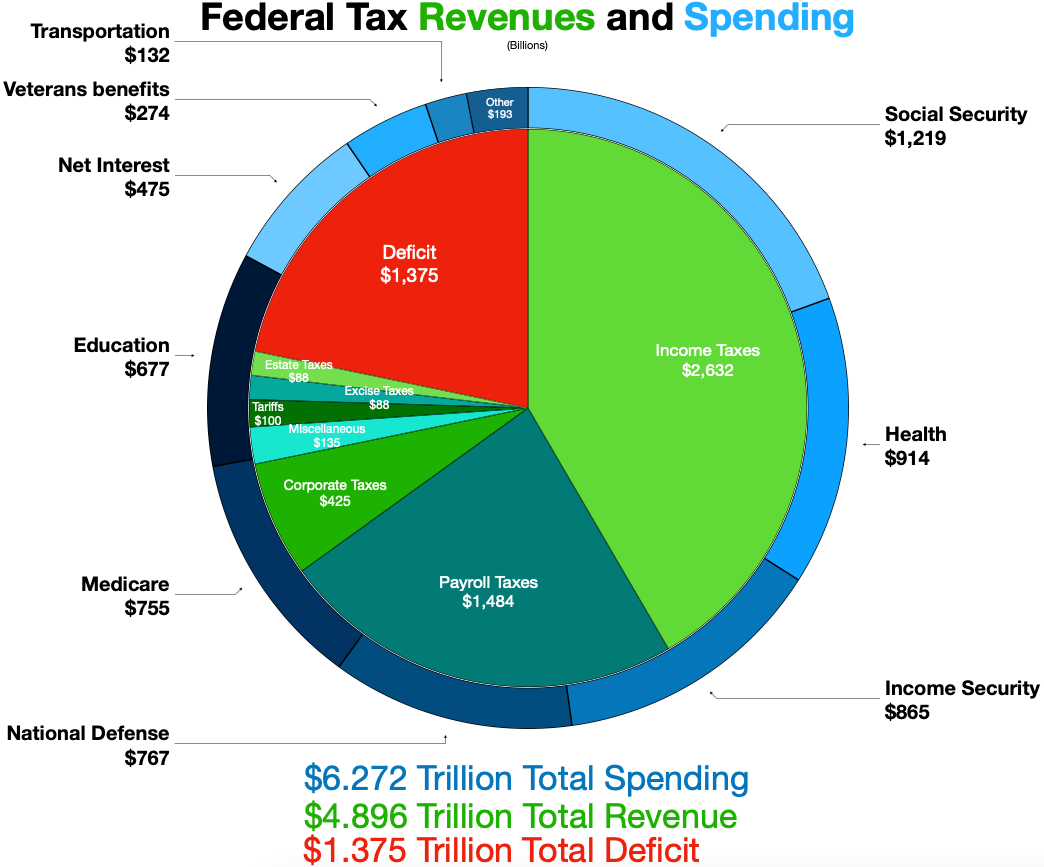

The U.S. budget deficit has come down since the pandemic emergency, but it’s still substantial — about 5%, which is more than twice as high as Russia’s 2022 deficit, and is higher than our deficit in 2012. And it’s projected to be even higher in 2023. In fact, it’s bigger than any deficit that we ran at any point between 1947 and 2009. Only in the depths of WW2, the Great Recession, and the pandemic years have we borrowed more than we did in 2022.

Austerity doesn’t mean taking that deficit all the way to zero, but tightening it up to, say, 3% or 2.5% of GDP seems reasonable. That would mean cutting the deficit by about $400 or $500 billion.

Most people assume that “austerity” means spending cuts, and these are indeed what the Republicans have in mind. But there’s also another way to do austerity: raise taxes. Given that Dems control the presidency and the Senate and the Republicans control the House, it seems reasonable that an austerity deal should include both tax hikes and spending cuts.

First, let’s talk about taxes. Tax revenue is actually unusually high as a percent of GDP right now, thanks to the booming economy:

But there’s still room to make some hikes here, especially because that’s what we’re eventually going to have to do to sustain Social Security benefits. One idea is to repeal the pass-through tax break that Trump enacted (and which I personally have benefitted from substantially). Another is to raise the cap on the SALT deduction, which allows rich people in high-tax states like California to get a federal tax break. In other words, raise taxes on Noah Smith! Other good ideas include closing the carried interest loophole (which mostly enriches private equity firms), implementing a value-added tax like the one Europe uses (basically, a national sales tax), and ending the step-up basis loophole on the estate tax. Of course, in a pinch, raising income taxes on the top brackets always works, with few if any economic downsides.

As for spending cuts, this is tricky, since there are obviously a lot of things we want to be spending more money on right now — in particular, industrial policy and the green energy transition. That spending is especially good because it’ll eventually partially pay itself back in the form of higher tax revenues.

As for military spending — a perennial target of progressives — it seems like a bad idea to cut that right now, given the need to produce munitions for Ukraine while also arming Taiwan and modernizing our military to be able to resist China. There probably are some military items we should cut — big expensive legacy platforms like aircraft carriers — but this will be politically tough. Probably the best option for saving on defense costs is to cut down on operating expenses — i.e., have our military do fewer things around the world, and instead have it focus on preparing for the few conflicts that really matter.

That still leaves the vast bulk of federal spending, which is social spending — health care, income security, and education.

Progressives aren’t going to like it, but spending on some of these social items can be reduced by simply limiting the amount they grow each year. I would especially look at curbing spending on health and higher education, as this tends to pump up the prices of those services, which just ends up making people angrier in the long run. Income support and other benefits for poor people, of course, should not be cut.

In any case, off the top of my head, that’s what a good austerity compromise would look like. There’s really not an emergency in our country that requires borrowing 5% of GDP right now, and the best solution is just to spread the pain out evenly — raise a bit of taxes here, slow a little bit of spending growth there, etc.

But in exchange for a bipartisan austerity budget, they really should abolish the debt ceiling — or at least neuter it so that it can’t threaten to blow up the entire U.S. economy every few years.

But Republicans are terrorists (literally, not figuratively). The majority of Congressional Republicans endorsed terrorist attempts to overthrow the US government, and are backing the leader of the terrorist movement as their next presidential candidate. Saying "US governance is shaky" is being generous.

If you really want to increase tax revenue, none of your proposals do much. There simply aren't that many people in the top tax brackets.

If you want a dent in GDP, you're going to have to notice that the median taxpayer is paying <8% income tax (12% marginal, but after the increased standard deduction and 10% initial bracket...). This is SIGNIFICANTLY lower than it was back in the late 90s.

Raise taxes on everyone, that's the only way.