Yes, reshoring American industry is possible

Americans can make stuff, after all.

Reshoring American industry has become a bipartisan policy objective — it has always been part of Donald Trump’s agenda, and Biden cared a lot about it as well. The idea has always been met with skepticism from a number of directions. Many economists and free traders are skeptical of anything that involves tariffs and/or industrial policies. And partisanship being what it is in America, both Republicans and Democrats have naturally doubted the others’ ability to follow through on their promises. But in addition, I often encounter a natural skepticism about America’s ability to do manufacturing at all.

Americans can be forgiven for having this impression. Most of our lived experience has either been the Rust Belt era of the 1980s, or the supercharged offshoring of the 1990s, 2000s, and 2010s. America has not had a factory building boom in a very long time. On top of that, most people who take economics in America learn only one theory of international trade, which is the theory of comparative advantage — basically, the idea that countries specialize in whatever they’re best at. It’s easy to believe that America specializes in software and services instead of making physical stuff, because that’s the way things were trending for decades.

If you believe that, then you probably think that reshoring manufacturing will always be an uphill battle, if not downright impossible. Sure, with enough tariffs and subsidies we could force Americans to buy more expensive stuff made in America, but this will make us all poorer. Why not just leave manufacturing to the East Asians, and maybe the Germans, and focus on what we seem to be good at?

And yet the simple way to think about trade isn’t necessarily the right one. There’s another theory that says that since America has lots of capital and technology, we can do a lot of automated manufacturing. And there’s yet another theory that says that because the world loves variety, the U.S. can manufacture close variants of the things the Asians and Europeans make. The deindustrialization of the U.S. since the turn of the century might be more about an overvalued exchange rate, deliberate Chinese competition, and U.S. industrial policies that favored the financial sector over the manufacturing sector.

The common belief that Americans just aren’t good at making stuff seems contradicted by areas in which we are startlingly good at making stuff — for example, SpaceX, which is pumping out the world’s best rockets from U.S. factories in stunningly high volumes. The American South has also become a hub of high-quality auto manufacturing, with the help of Japanese and South Korean investment:

If that’s true, then reshoring has a chance. The uncompetitive dollar will remain a major problem, but Chinese competition can be blocked with tariffs and other trade barriers, and U.S. industrial policies can shift from a pro-finance to a pro-manufacturing orientation. In fact, this approach is already bearing fruit in a number of strategic industries.

Take solar power, for instance. For years, the main story in that industry was the collapse in U.S. manufacturing, and the overwhelming dominance of China. In an article in Bloomberg last September, David Fickling lamented:

The fall of America as a solar superpower is a tragedy of errors where myopic corporate leadership, timid financing, oligopolistic complacency and policy chaos allowed the US and Europe to neglect their own clean-tech industries. That left a yawning gap that was filled by Chinese start-ups, sprouting like saplings in a forest clearing.

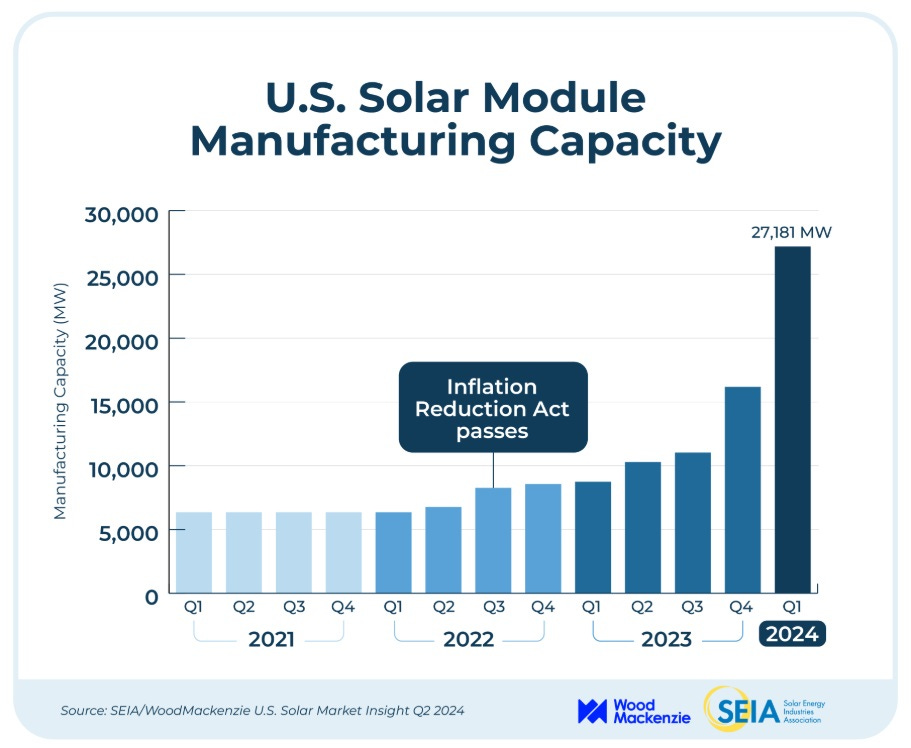

But even before that story hit the presses, things had already begun to change. In December, the Solar Energy Industry Association reported that U.S. solar manufacturing capabilities are on the rise:

In 2017, the U.S. ranked 14th in the world for solar panel manufacturing capacity. Starting in 2018 and then accelerating in 2022, additional factories started springing up left and right throughout the country, with a focus in the South…Major investments poured into building factories and expanding existing facilities. Today, the U.S. has leapfrogged competitors and ranks 3rd in manufacture of solar panels, passing large solar manufacturing countries like Malaysia, Thailand, Vietnam, and Turkey…A new report by SEIA and Wood Mackenzie found that the industry had reached a critical threshold:

After a record Q3, U.S. solar manufacturing has reached a critical threshold. At full capacity, American solar module factories can now produce enough to meet nearly all demand for solar in the U.S.

As more solar deployment happens, more manufacturing will come online…Companies are investing billions of dollars to produce American-made solar panels in states like Georgia, Ohio, Texas, Washington, South Carolina, and Alabama…[T]here are more factories on the way, either announced or under construction.

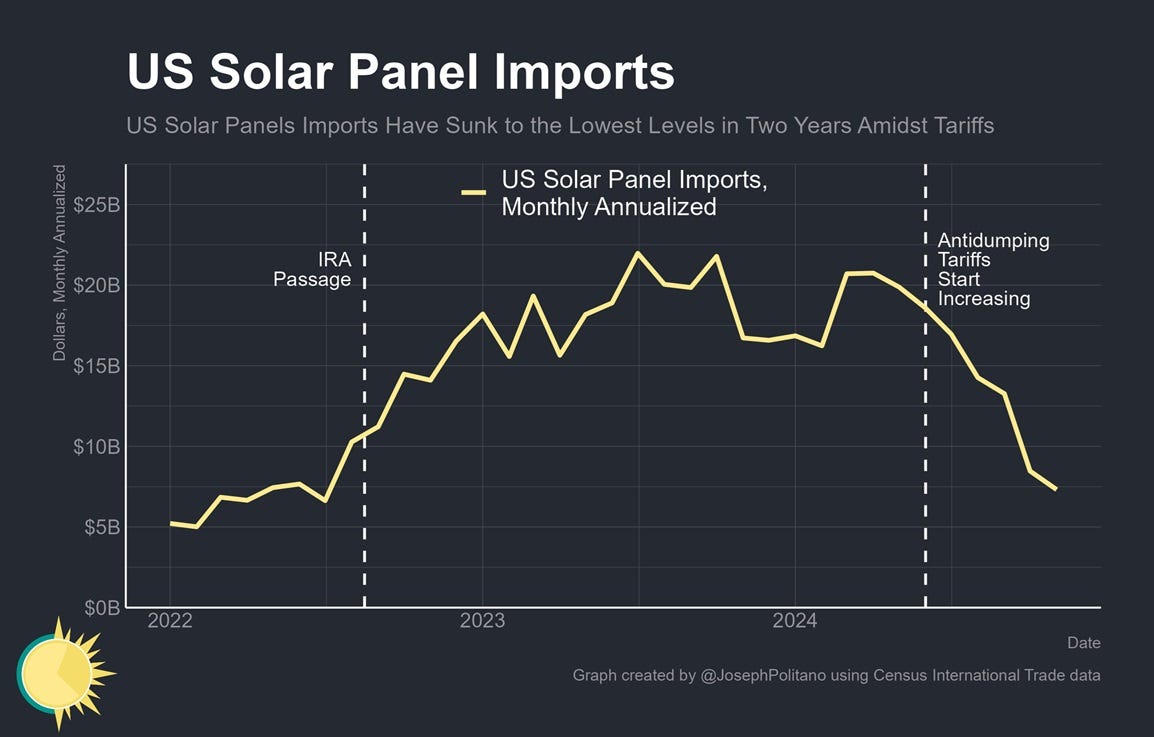

Obviously the U.S. is still way behind China, but this rising trend of production and self-sufficiency is very different from the typical story you hear. As the article notes, the reshoring of solar began in the late 2010s, under Trump, and may have had something to do with Trump’s tariffs on solar panels. A second round of tariffs, courtesy of Biden, went into effect near the end of 2024, and definitely seemed to have an effect on solar imports:

But it was Biden’s Inflation Reduction Act that really kicked solar reshoring into high gear:

For another example, look at semiconductors. I’ve written a lot about how the CHIPS Act has galvanized U.S. production in this most strategic of all industries, including major investments from Taiwan and elsewhere. This is from a recent report by the CHIPS Program Office:

The United States has seen more investment in electronics manufacturing over the last four years than in the previous three decades combined. Planned investments are now nearly $450 billion, marking the largest wave of semiconductor manufacturing expansion in U.S. history. This includes the two largest domestic investments in semiconductor manufacturing by U.S. companies in history (Intel and Micron), as well as the two largest foreign direct investments in new projects by any company in history (TSMC and Samsung)…Perhaps most significantly, for the first time, all five of the world’s leading-edge logic and dynamic random-access memory (DRAM) manufacturers (Intel, Micron, Samsung, SK hynix, and TSMC) are building and expanding in the United States. By contrast, no other economy in the world has more than two of these companies manufacturing on its shores…

The United States is projected to produce at least 20 percent of the world’s leading-edge logic chips by 2030 (up from zero percent in 2022) and ~10% of its leading-edge DRAM chips by 2035 (also up from zero percent)—both technologies that are essential to the future of artificial intelligence (AI), high-performance compute, and advanced military systems. TSMC’s Arizona facility has already begun volume production of leading-edge chips, marking the first time in roughly a decade that a new fab is making these technologies domestically.

And The Economist, certainly no friend of industrial policy in general, has grudgingly admitted that U.S. reshoring of the semiconductor industry is succeeding:

Early returns are impressive: the [CHIPS Act] programme has catalysed about $450bn of private investments. And this money is spread across much of the industry, from high-tech packaging to memory chips. One marker of success is the production of the most advanced chips, measuring less than 10 nanometres in size. In 2022 America made few such chips. By 2032 it is on track to have a share of 28% of global capacity.

As in the case of U.S. auto manufacturing a generation earlier, foreign direct investment — especially from Taiwan’s TSMC — has played a crucial role.

In early 2024, some poorly informed pundits were writing stories declaring that “DEI killed the CHIPS Act”, while others were wondering whether Americans had a culture capable of making chips. Those articles were spectacularly ill-timed — obstacles were quickly overcome, and the factory is now pumping out 4nm chips. Those are, by at least some measures, the most advanced semidconductors ever made on American soil.

And what’s more, those chips are being made with yields (i.e., quality) that are comparable to, or even higher than, what Taiwanese factories get. The idea that American workers are unable to produce high-quality products turned out to be wrong. The chips made in the U.S. are a bit more expensive (around 30% more right now), but that cost differential will probably come down as volume ramps up and as chipmaking experience spreads throughout the country.

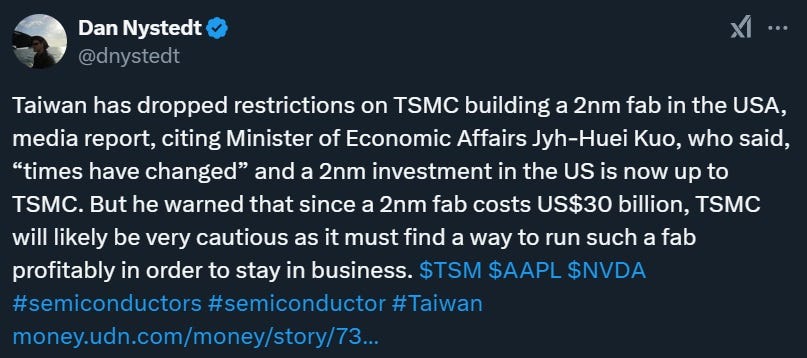

In fact, the reshoring effort is going so well that TSMC is now planning to build even more cutting-edge chips at its U.S. plants:

So far, the effort to reshore semiconductors is turning out to be a big success.

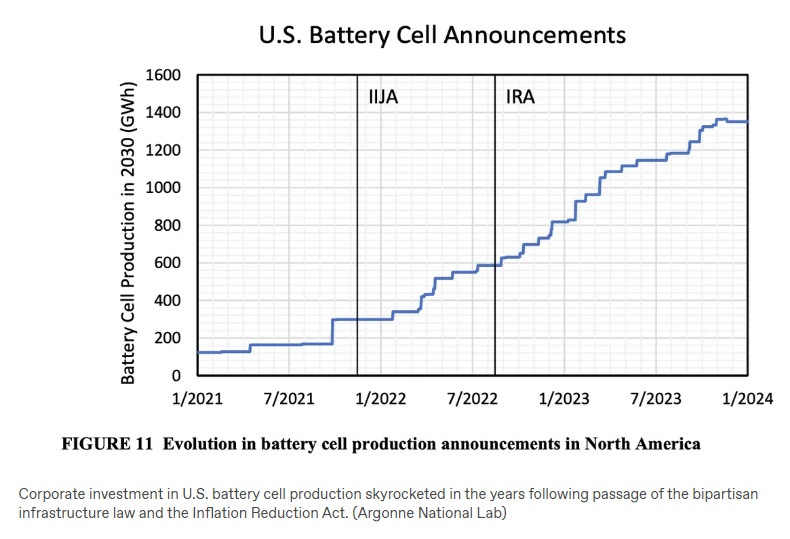

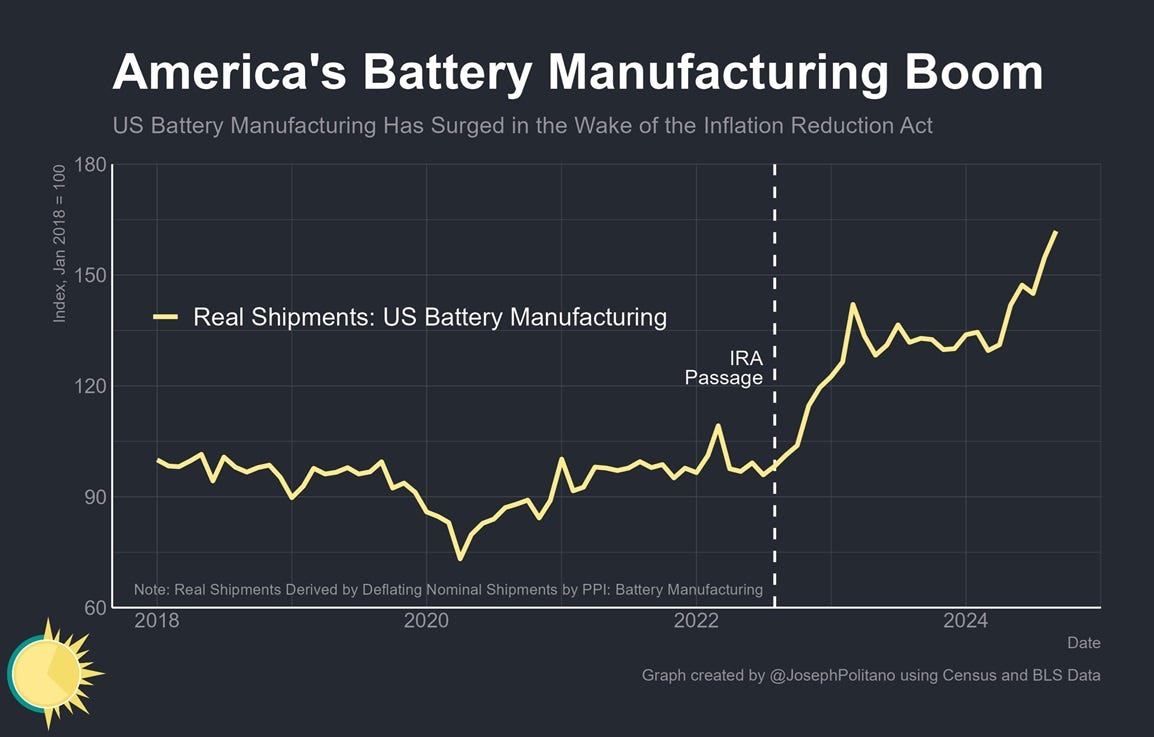

Batteries look like a third reshoring success. Currently, most batteries are produced in China, but the Inflation Reduction Act may be starting to turn things around:

It’s not just factories being announced, either; production in the U.S. is way up:

The reshoring of the solar, chip, and battery industries is a direct rebuttal to the naysayers, and proof that American manufacturing can succeed.

Although these are only three industries, they will inevitably facilitate the reshoring of related industries that either supply these manufacturers or consume their output. American reindustrialization isn’t just about a few key tentpole industries — it’s about a whole web of suppliers, customers, related industries, and talent. Fortunately, we can already see this web starting to form in the U.S. SEIA reports that America’s solar manufacturing boom isn’t just limited to the panels themselves, but related industries like solar tracker, solar inverters, and upstream materials production like wafers and ingots.

Meanwhile, the CHIPS Program Office reports that the semiconductor boom also includes downstream activities like packaging and testing. The Economist points out that this ecosystem, as well as the talent that gets developed for the CHIPS Act’s projects, will reduce costs and help sustain future expansion of chip manufacturing in America:

The subsidies have helped to shrink a gap of roughly 30% in the cost of building and operating fabs in America compared with in Asian countries. In part costs are lower in Asia because Asian governments lavish handouts on companies. But Asian producers have also reaped the benefits of dense manufacturing clusters, with well-trained workforces and plenty of suppliers nearby. The hope is that CHIPS has started this process in America. “It’s enough to get the flywheel going,” says [outgoing Commerce Secretary Gina] Raimondo.

At this point, whether reshoring continues is largely a matter of political will and smarts. If Donald Trump keeps attacking the solar industry, or follows through on his earlier threats to cancel the CHIPS Act, it could shift production decisively back to China. It would be ironic if a President who rose to power promising to restore American industry ends up being the person responsible for strangling our industrial revival in its crib.

These reindustrialization successes almost look too easy. At this rate, focused tariffs might be outright profitable. You just have to assume there are positive externalities to new business clusters in your country. Spillover benefits in new industries seem real enough - just look at Silicon Valley.

It's the same logic as the old "Dutch disease" or "resource curse", except America's distorting resource export isn't oil but Treasury bonds.

I think Michael Pettis' reasoning makes a lot more sense when you think about how resource exporters often underperform, and then apply the same logic to American exports of sovereign bonds.

We've been deindustrializing ourselves as a favor to China and the other surplus countries' employment policies. It's time to start growing our own industries again.

I wonder how much that we could achieve the same outcome, at far less expense and deadweight loss to the US economy, by reducing the federal budget deficit and rebalancing the tax code away from consumption. Part of the reason that US manufacturing is uncompetitive is due to cheap imports because the dollar is strong due to capital inflows for US Treasuries. If domestic savings and investment were more balanced, would you see the same effect without having to play political favorites with industries? While I'm happy that US battery, semiconductor, and solar panel industries are doing well, is there a flip side to this where other kinds of manufacturing is down in industries that aren't politically favored?