Will China, Inc. be zombified?

A question surprisingly few people are asking.

{kind=link}

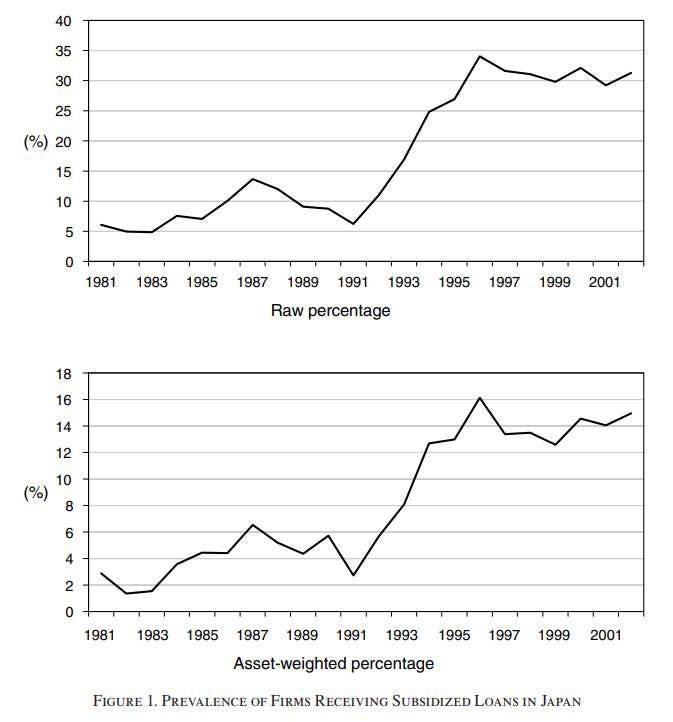

The photo above is not from China; it’s from Japan. In the 1970s, Daiei was Japan’s top retailer. But after Japan’s asset bubble burst around 1990, it became Japan’s most famous “zombie” company — staggering along unprofitably, kept afloat by a constant stream of below-market-rate loans from UFJ Bank and other big Japanese banks. Eventually the company was acquired by Aeon, a more successful retailer, and its once-storied brand is slated to be retired for good in the next few years.

I tend to be very skeptical of comparisons between post-1990 Japan and post-2021 China, because there are just so many differences between the two economies (and between the global economic environments at the time). Their industrial policies are different, their trading relationships are different, their bubbles and busts happened for very different reasons, and so on. But in the case of “zombie” companies, there may be some important parallels.

What’s important about Daiei is not how it failed, but why it didn’t fail much sooner. Caballero, Hoshi, and Kashyap wrote a paper in 2008 arguing that “zombie” companies like Daiei held the Japanese economy back during the 1990s (and, in some cases, even beyond the 1990s).

The basic story is that after 1990, the Japanese economy slowed down, and lots of companies that used to be profitable — especially in the construction, retail, and trading sectors — were no longer profitable. These companies owed a lot of money to banks. If they stopped being able to pay back their loans, the banks would be forced to recognize bad debt on their books. This would get them in trouble with regulators (because of capital requirements), and it would also get them in trouble with the Japanese public.

So what the banks did was to lend even more money to the failing companies that already owed them a lot of money, at very cheap interest rates. The new loans were used to pay back the old loans, and the new loans would be classified on the bank’s books as “good” debt. This process — known as “evergreening” — kept banks from ever having to acknowledge their losses:

Peek and Rosengren (2005) document this empirically as well.

Evergreening kept a bunch of companies afloat — like Daiei — that had utterly broken business models. Theoretically, the companies could have eventually pivoted their business models and recovered, or Japan’s economy could have started booming again, etc. In practice, this never happened.

Caballero, Hoshi, and Kashyap argue that evergreening was very bad for the Japanese economy, because it hoovered up scarce resources that better companies could have used to grow. With all of those crappy loans clogging up their books, Japanese banks couldn’t lend to healthier companies. With big zombies like Daiei still able to employ large amounts of Japan’s best managers, young scrappy upstarts were deprived of talent. The authors argue that keeping all of this labor and capital locked up inside doomed companies contributed significantly to Japan’s long productivity stagnation.

Why did the Japanese government allow this to happen? Preserving employment at the zombie companies was probably a big part of it. Japan had a strong tradition of job security at that point in time, and to throw so many people out of work — even if they could have gotten new jobs eventually — would have been seen as cruel and unfair. Social unrest was a possibility. Bank bailouts may also have been deeply politically unpopular. In any case, whatever the reason, throughout the 1990s the government supported banks with various capital injections and regulatory forbearance, without forcing banks to cut off the zombies.

Anyway, that’s Japan. The question is whether something like this will happen in China.

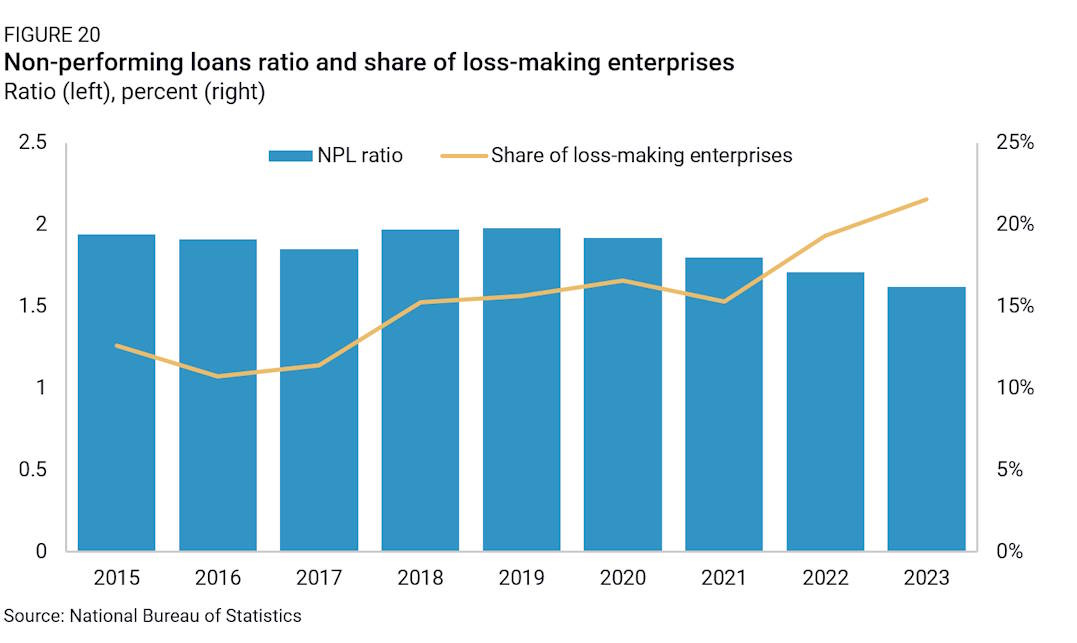

China’s experience with its real estate bubble and bust doesn’t exactly parallel Japan’s, but there are some broad similarities. Since 2021, there has been a broad economic slowdown (probably more severe than the official numbers suggest), and a long-lasting chill in real-estate-related industries. This has predictably led to a rise in the number of loss-making companies:

You’ll notice on this chart that the share of non-performing loans has actually gone down since 2021, even as fewer companies are turning a profit. That suggests that lots of Chinese companies are being kept on life support by cheap bank loans. Here’s the Rhodium Group:

Some concrete data points suggest that China’s evergreening of debt is more widespread than is commonly the case in most market economies. The ratio of banks’ reported non-performing loans has decreased over the past years, while the share of loss-making enterprises increased…This would indicate Chinese banks have been sitting on large volumes of NPLs that have not yet been fully recognized. This is an open secret: The National Audit Office recently claimed in an annual audit report to the NPC that 16 of 43 audited banks last year had NPL levels that were double the officially reported figure…

Loan rollovers are a pervasive phenomenon in China…[T]he financial system…served as a shock absorber, channeling resources to enterprises facing losses to maintain output and prevent the defaults and bankruptcies that occurred in market economies.

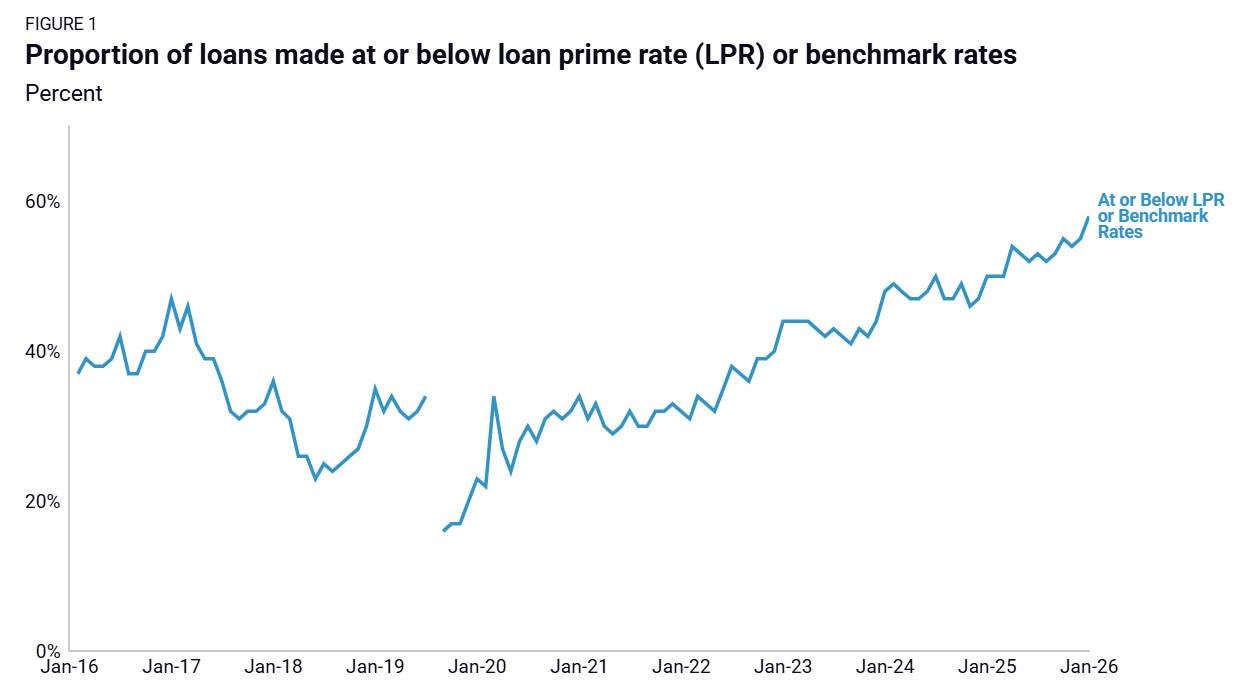

Another Rhodium report finds that the proportion of loans made below benchmark rates has risen significantly since 2021, even though benchmark rates are lower than they were back then:

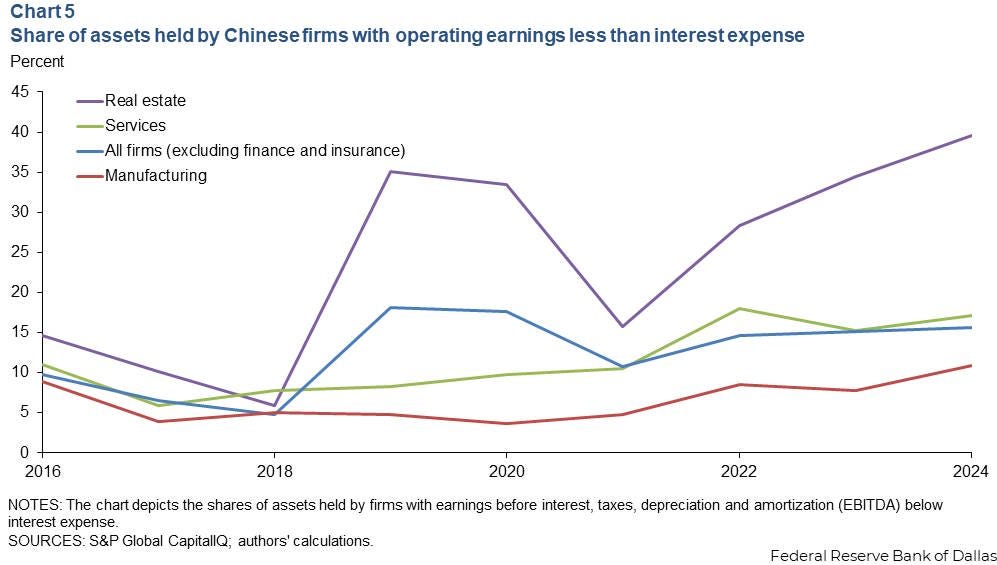

And the Dallas Fed has documented how more and more Chinese companies, especially in the real estate sector, aren’t making enough money to pay the interest on their loans:

All this — falling official NPLs, much more below-market lending, companies unable to pay their interest expenses, widespread suspicion that many of the companies whose loans are “performing” will never be able to repay those loans — matches the general pattern that Hoshi and Kashyap (2000) documented in post-bubble Japan. Banks have taken a bunch of losses, but have refused to recognize those losses, using a flood of cheap debt to keep their borrowers afloat.

A bunch of people have warned about this. Here’s Rhodium:

Because of the political incentives shaping China’s financial system, banks in China tend to extend or roll over debt to poorly performing or loss-making companies. This can have some of the same effects as a subsidy, by removing incentives for companies to stay profitable and isolating them from market forces that would otherwise lead to their restructuring or bankruptcy….Evergreening of credit, therefore, allows firms to…[reduce] domestic and global prices to unprofitable levels[.]

And here’s the Dallas Fed:

There is mounting evidence of “zombie lending” in China, banks rolling over bad loans to unprofitable firms and allowing the status quo to continue rather than recognize losses.

And here’s a Business Times story about how China’s government has allowed and even encouraged zombification, much as Japan did in the 1990s:

It’s impossible to quantify the true extent of the [bad debt] problem, though most economists say the ratio of bad loans is significantly higher than the 1.5 per cent official rate…One analyst at Absolute Strategy Research in London pegs it at about 10 per cent…Others say it could be double that amount…

While the [banks’] leniency [toward borrowers], largely condoned by regulators in Beijing, has helped maintain financial stability over the past few years, it also means the banking system is recycling capital into unproductive companies rather than spurring real growth in healthy firms…

[Government] officials have moved to bolster the nation’s six biggest banks with more than US$100 billion in fresh capital…[R]ather than cracking down on deadbeat borrowers, China’s banks are encouraged to cut them some slack. Regulators have for years urged the big banks to keep their reported bad loan ratio under 2 per cent, according to sources familiar with the guidance…As a result, banks routinely roll over maturing loans, extend repayment periods, or allow interest to be capitalised to avoid triggering NPL recognition.

Now you might be tempted to think — and I’ve seen a few people argue — that this only matters in a market economy. In a market economy, undercapitalized banks matter because banks have to succeed or fail on their own. In a state-directed economy like China’s, the theory goes, debt on the banks’ books might as well be on the government’s books.1 Banks can keep lending no matter how much bad debt they have, because the only entity that could punish them — the Chinese government — wants them to do so.

But while government control might avert a financial crisis, it doesn’t automatically solve the zombie problem, or make the comparison with Japan inappropriate.

First of all, it would be a mistake to see Japan’s government in the 1990s as operating at arm’s length from Japanese banks. It most certainly did not; in fact, it acted to support the banks that were supporting the zombies. The government bailed out the banks, deliberately turned a blind eye to the zombie problem, and encouraged banks to keep on lending to healthier companies despite the unrecognized bad loans on their books. That’s not too different from what China’s government seems to have done in response to the real estate bust, at least initially.

But simply having the government urge (or order) banks to keep lending didn’t solve the zombie problem in Japan, and it won’t solve it in China either. Even if the zombie companies don’t end up competing with healthier companies for capital, they compete with them for other resources. They compete for labor — workers who could be working at young, growing, healthy companies are instead being paid to continue to work for unproductive companies that are just spinning their wheels. They also compete for raw materials, for land, for energy, and so on.

These resources are not in infinite supply, even in China. As long as unproductive zombie companies are hiring workers, hoovering up metals and chemicals and watts of electricity, and taking up prime real estate, they’re holding back the rest of the economy. This doesn’t just manifest as higher costs for healthy companies — it also shows up as increased competition. In 1990s Japan, if a new retailer wanted to enter the scene, it had to compete with Daiei, the unproductive behemoth that was essentially being paid by banks to produce below cost. The same will be true in China.

In fact, this may be a reason for the “involution” that Chinese companies are experiencing. In the wake of the real estate bust, China’s government directed banks to lend to manufacturing companies instead of to real estate-related companies. They did this (though some of the loans ended up sneaking back into the real estate sector). In fact, a large percent of the “subsidies” that China dishes out to its manufacturing companies is through below-market-rate loans.

Some of these manufacturing companies will be successful and efficient — indeed, many already have been. But others are unproductive and inefficient. Instead of letting these die, China’s banks may keep them on as zombies as well, paying them to compete with China’s healthier companies. Here’s Alicia Garcia-Herrero from back in March:

In many sectors, including…electric vehicles, solar panels, batteries, and other green technologies…Chinese firms…keep selling at rock-bottom levels, sometimes below what it costs to produce, just to hold onto market share. A growing number of these companies cannot earn enough revenue to even service their debt…These “zombie” companies survive only because banks roll over loans and local governments provide subsidies to avoid job losses and keep tax revenues flowing…In newer, high-priority sectors like green tech, the share of zombie companies has hit 30 percent of total listed companies…

Without real productivity advances, [zombies] still join the price-slashing frenzy to stay in the game thanks to external support from banks or local governments. They cut prices aggressively…The outcome is predictable: collapsing profit margins across the board, even for the better companies, whose productivity is increasing.

When we Westerners think about the effect of Chinese zombification, we often think about the flood of cheap exports threatening to deindustrialize Europe and other regions. But while that export dominance might seem like a victory to China’s mercantilist leaders, it’s a double-edged sword, because zombification reduces productivity at home. In the long run, lower productivity hurts growth, despite the temporary bump from exports.

In other words, China’s fusion between the financial system and the state may have made zombification worse, not better. The Chinese state is not a ruthlessly efficient allocator of capital; it has sociopolitical goals just like any other state, and it fears the unrest that could result from widespread corporate failure and unemployment. Yes, it can tell banks to lend to manufacturers instead of property developers, but that just ends up adding more zombies to the horde.

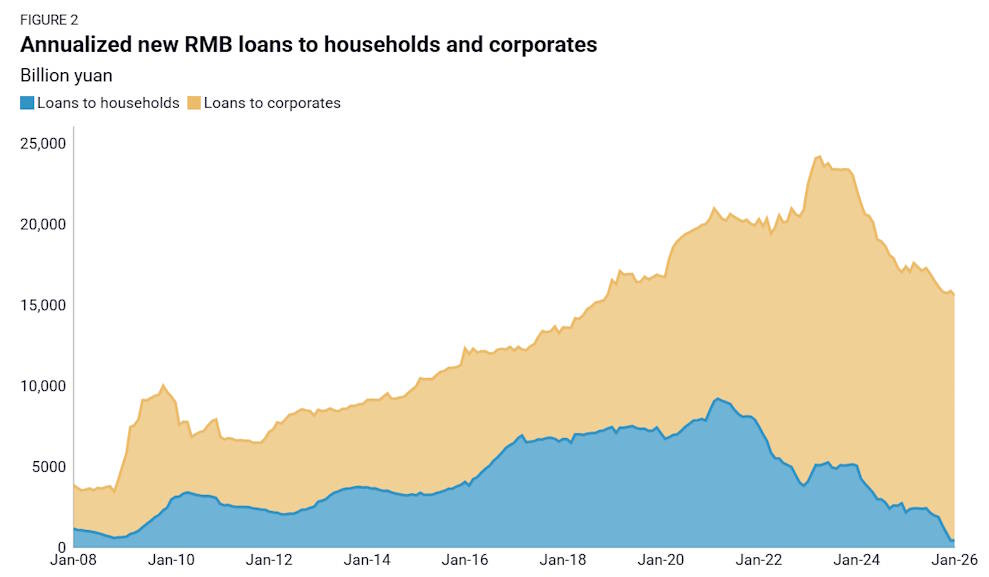

And at some point, even state-owned and state-directed banks probably do care about profitability. Yes, the government can bail out any bank at will, but if you’re the bank executive or manager who dished out the bad loans and made a bailout necessary, your career might be over. This might be why corporate loans have started to fall slightly from the torrid pace of 2023-24:

Ultimately, when people write the story of China’s economy in the 2020s, zombification could end up being more fundamental to that story than exports. The parallels with Japan are not always real, but they’re real in this case — and so far, China’s government seems to be walking into a similar trap.

Update: In the comments, Jack Lowenstein asks a very important question: So what? Even if zombification proceeds in China, what are the downsides from the point of the Chinese government? He writes:

I think the critical difference between Japan’s “extend and pretend” policies and China’s is the geopolitical element.

Japan feared domestic social and political disruption - and was heavily influenced by “free market” vested interests. There was also a degree of denial by MOF and METI that the gogo years of the post war period up to the mid 1980s were really over.

The CCP and the PRC however are driven by the deliberate aim of de industrialization of critical parts of the OECD supply chain. Loans and other support to the companies that will deliver this outcome are not going to stop for economic reasons.

Sadly policy makers in most of the countries suffering these effects are ideologically unwilling to enact anti-dumping and other defenses to respond. So zombification will not stop in China. Yes the population of the PRC will pay a price. But since when did the CCP care about that?

This is a very important question, and I should have probably gone into that more in the post. Here was my response to Jack in the comments:

I think some of these are real differences, but perhaps not all of them.

“Japan feared domestic social and political disruption” <-- I actually don’t think this is a big difference. China is worried about social and political disruption as well -- just look at how fast Xi ended Zero Covid after some small scattered protests. The old social compact in China was “growth in exchange for political quiescence”. But with rapid growth now over, that social compact is gone, so the possibility for unrest is definitely there.

“There was also a degree of denial by MOF and METI that the gogo years of the post war period up to the mid 1980s were really over.” <-- I’m not sure this is different either. China has been overstating its growth since the bubble burst in 2021 (https://rhg.com/research/chinas-economy-rightsizing-2025-looking-ahead-to-2026/). This is often a tool the government uses to “smooth” growth between good and bad years (https://www.aeaweb.org/articles?id=10.1257/mac.20150074), suggesting that they think fast growth might come back.

“The CCP and the PRC however are driven by the deliberate aim of de industrialization of critical parts of the OECD supply chain. Loans and other support to the companies that will deliver this outcome are not going to stop for economic reasons.” <-- This is true, and I think this is an argument FOR zombification. Unproductive, unprofitable companies that fill supply chain gaps will continue to be supported with evergreened loans.

So the question becomes: What are the downsides of zombification from the regime’s perspective? That’s a topic I should have considered more. One answer is “social unrest” -- if slow growth makes the repressiveness of China’s regime less tolerable, then we could see popular anger at the industrial-policy regime. Remember that Japan was a very free society, where people could pivot from the pursuit of money to the pursuit of lifestyle and art and leisure. That’s not necessarily true in China.

Another possibility is that eventually China becomes more like the USSR. The USSR was famously unproductive, because it insisted on onshoring its entire supply chain. Right now, China looks hyper-competitive in a bunch of high-tech industries, but if zombies suck up more and more labor and other resources (including compute), that competitiveness could narrow over time.

Finally, there are fiscal dangers (https://rhg.com/research/chinas-financial-and-fiscal-decay/). When Europeans buy cheap Chinese EVs, part of the consumer surplus they receive comes out of the pockets of Chinese taxpayers and bondholders. Japan’s zombification caused it to run up an enormous amount of debt, which it was able to carry safely only thanks to A) persistently low demand and low natural interest rates, and B) the government’s ability to buy overseas assets that performed extremely well (https://www.ft.com/content/f7d3f20c-b303-4f6c-b4a0-8ee8906ae155). Now that the first of those has gone away, Japan’s government debt IS becoming a problem, with a plunging exchange rate and creeping inflation.

So while China’s government can get away with “damn the economics, full speed ahead” for a while, eventually I think something breaks...

And since that debt is owed almost entirely domestically, the theory says that the debt doesn’t really matter in a macroeconomic sense; it’s just some Chinese people owing money to other Chinese people.

I think the critical difference between Japan’s “extend and pretend” policies and China’s is the geopolitical element.

Japan feared domestic social and political disruption - and was heavily influenced by “free market” vested interests. There was also a degree of denial by MOF and METI that the gogo years of the post war period up to the mid 1980s were really over.

The CCP and the PRC however are driven by the deliberate aim of de industrialization of critical parts of the OECD supply chain. Loans and other support to the companies that will deliver this outcome are not going to stop for economic reasons.

Sadly policy makers in most of the countries suffering these effects are ideologically unwilling to enact anti-dumping and other defenses to respond. So zombification will not stop in China. Yes the population of the PRC will pay a price. But since when did the CCP care about that?

This article is very clear - and damning. One point should become more clear: China is also competing against every other country. By undercutting those counties, China is evicerating their future. By undercutting, say, the EU, it is going to put the EU out of business, depleting a generation of productive youth that won't have jobs. As Dionne Warwick sang, "And all the stars that never were are parking cars and pumping gas". I would think that tarrifs by the EU against China in this case would be a good idea, simply to protect their own capabilities. We all learned long ago that cheap ain't always good.

This point also raised a possibility for another useful article - or there may already be one: How big does a "country" have to be to be wealthy? And who gets to say that? Can the EU sell only within itself and be as rich as it is now? Can the US? What are the trade-offs if they aim to do so? I know those are black-and-white questions and that shades of grey are more the truth of the matter.

Thank you, Dr. Smith, for making the science of economics nowhere near dismal. More like "