Price controls: Too early for a victory lap

Narrative-driven triumphalism does not make for sound policy.

Here’s a story we all love: For many years, a theoretical consensus has held firm among the learned scholars of academia. Armed with this conventional wisdom, these scholars have gained prestige, fame, and money giving advice to the princes of the realm. Yet outside the cloistered ivory tower, one bold and brilliant iconoclastic researcher has discovered that the mainstream consensus is all wrong. Armed with an explosive new theory, the iconoclast travels to the halls of power to speak the truth. Initially scorned, the lone scholar eventually forces the world to recognize the superiority of their new paradigm with the power of incontrovertible empirical evidence…

…and so on. Nothing exactly like this ever happens, but it’s a powerful archetype — the scientific equivalent of Campbell’s “Hero’s Journey”. It’s not too hard to map the legends of our favorite scientific heroes — Galileo, Pasteur, Darwin, Einstein — onto this template. So if you want to get the public excited about the work of an iconoclastic scholar, you should probably try to tell their story as a version of this archetype. Let’s call it the Iconoclast’s Journey.

Zachary Carter masterfully harnesses the Iconoclast’s Journey in a recent New Yorker profile of economist Isabella Weber. Weber, a professor at UMass-Amherst, is a prominent proponent of the theory many call “greedflation” — the notion that inflation is caused by companies’ monopolistic behavior rather than by macroeconomic factors, and that the proper solution to this is price controls. Carter tells a story about how first the defenders of macroeconomic orthodoxy ignored Weber, then they laughed at her, then they fought her, and then she won:

[W]hile Weber was [skiing], a short article on inflation that she’d written for the Guardian inexplicably went viral. A business-school professor called it “the worst” take of the year. Random Bitcoin guys called her “stupid.” The Nobel laureate Paul Krugman called her “truly stupid.” Conservatives at Fox News, Commentary, and National Review piled on, declaring Weber’s idea “perverse,” “fundamentally unsound,” and “certainly wrong.”…

[Weber] had transformed from an obscure but respected academic…into the most hated woman in economics—simply for proposing a “serious conversation about strategic price controls.”…Weber was challenging an article of faith, one that had been emotionally charged during the waning years of the Cold War and rarely disputed in its aftermath. For decades, the notion of a government capping prices had evoked Nixonian cynicism or Communist incompetence…

Today, in a host of key sectors, [price controls are] more or less happening. The European Union is regulating the price of natural gas, the Biden Administration is regulating the price of oil, and the G-7 is enforcing a global cap on the price of petroleum products produced in Russia. Inflation appears to be cooling, and by nearly every measure we are living in the best labor market in a quarter century.

Weber, meanwhile, has recovered from her moment of notoriety. She’s now living something like the public-intellectual dream: shaping German energy policy one day, testifying before Congress the next. Her portrait is on the cover of a recent issue of the German-language magazine Institutional Money, the Financial Times writes about her academic work, the Washington Post wants her op-eds, and Bloomberg can’t stop hosting her on its flagship podcast. Analysts at the French investment bank Société Général and the European Central Bank now take much of Weber’s analysis for granted. In January, Krugman—who apologized to Weber as the fracas peaked—even argued that price controls might be a useful piece of inflation management after all.

Congratulations to Dr. Weber on her newfound prominence! But look carefully, and you’ll find that the story Carter is telling about economic policy over the last year doesn’t actually map that closely to what has actually happened — or what Weber suggests. A victory lap like this article is extremely premature.

Price controls, but only on oil and gas

Carter’s article, which focuses on Weber’s support for price controls, oversimplifies what is actually a nuanced policy recommendation on Weber’s part. In Weber’s 2023 paper “Sellers’ inflation, profits and conflict: why can large firms hike prices in an emergency?”, with Evan Wasner, she sums up her ideas for how to conduct anti-inflationary policy:

To be prepared for future emergencies, buffer stock systems are needed for a wider range of commodities. Limiting financial speculation on commodities is another useful tool to reduce the potential for impulses that can help trigger inflation. To prevent companies from exercising temporary monopoly power in response to a bottleneck, price gouging laws in many US states prohibit excessive pricing in emergencies. For the most part, these laws focus on consumer essentials. Similar national or even international regulations that limit the degree of legal price increases in times of emergencies for systemically significant upstream sectors could play an important role in preventing impulses that then propagate through the whole economy, creating inflation on the way. To be effective, price gouging laws need to be backed up with monitoring capacity. Windfall profit taxes can be a complementary tool that can make it less attractive for firms to hike prices in ways that increase profit margins and thus make initial price impulses and amplifications of price hikes less likely. Finally, if all these measures fail, strategic price controls for systemically significant sectors can be a means of last resort. Where prices are administered by a handful of firms, they are easier to implement than in competitive markets.

In fact, some of what we’ve done to reduce inflation so far does sound very much like a couple of the things Weber describes here! Specifically:

G-7 price caps on Russian oil purchases have helped to reduce the power of OPEC countries to keep oil prices high.

The EU has imposed dynamic price caps (i.e., price controls) on natural gas.

This sounds exactly like Weber’s suggestion of “national or even international regulations that limit the degree of legal price increases in times of emergencies for systemically significant upstream sectors”. It also sounds like “strategic price controls for systemically significant sectors”.

And as I argued in my last post, there’s good reason to believe that this strategy of price caps on oil and gas has been part of what has pushed inflation down from the 8-9% range to the 4-5% range. It was only one factor, of course. Russia’s need to glut the oil market to fund its war, rapid interest rate hikes by the Fed and other central banks that cooled off the housing market, and Biden’s use of the Strategic Petroleum Reserve were also probably important factors.

(Side note: When Carter says that “the Biden Administration is regulating the price of oil”, and presents this as a victory for price controls, he is wrong. Releasing extra supply is NOT a price control. But it is a buffer stock, which is another of Weber’s suggestions above.)

So anyway, we did do some of what Weber suggests, and it probably did help reduce inflation! But what we haven’t done is to implement anything resembling the more general regime of price controls that Weber suggested in her 2021 Guardian article, or which the U.S. implemented in World War 2 (Update: In a recent tweet, Weber has declared economy-wide, WW2-style price controls to be “mad”, and something to be reserved only for total war). In WW2, as Carter notes in his article, the Office of Price Administration regulated the prices of everything except agricultural commodities; no such comprehensive effort is underway today in either the U.S. or Europe. When Carter says Weber’s ideas are being implemented “in a host of key sectors”, he is simply wrong.

And this is true despite the fact that the current inflation is very broad-based. In his article, Carter incorrectly claims that most of the inflation we’ve experienced has been concentrated in energy prices:

If too much government spending were the problem, why weren’t all of the big spenders getting hit similarly hard? And if excessive household wealth were the key driver of inflation, you would expect the prices of consumer goods to rise more or less in tandem, as people bought more of everything. Instead, most inflationary pressure came from large spikes in the prices of specific products and commodities, such as natural gas. Were households devoting every cent of their stimulus checks to higher thermostat settings?

Even a cursory glance at the data would have shown that Carter is wrong about this. The median CPI measures broad-based inflation, because a median isn’t affected by a few outliers in the data. And median CPI inflation rose in late 2021 and is still fairly high today:

What’s more, inflation spread from goods to services in 2022:

What this means is that inflation isn’t just oil and gas, and it never was. Oil and gas are important, but they’re far from the whole story. (Economists argue vigorously about how much inflation is due to demand vs. supply shocks; Carter ignores this debate.)

Given how broad-based inflation is, someone who is in favor of price controls would naturally suggest a more broad-based price control regime than what has been implemented with regards to oil and gas. And indeed, Weber has been suggesting it. But we haven’t done it yet. There are serious dangers involved in a scheme like that. It went OK in World War 2, but there was a LOT of other stuff going on at that time — rationing, war production, and so on. And in some countries like Venezuela, schemes of comprehensive price controls have run totally off the rails.

So it’s very premature to say that Weber’s ideas have triumphed in the court of public policy. Her most sweeping, transformative ideas have not yet been implemented, and may never be, because of legitimate fears about the adverse effects.

This is also true in the case of Germany and its “price brake” on energy.

What happened in Germany

Isabella Weber is German, and in late 2022 she sat on a commission that Germany set up to deal with the high cost of energy following the cutoff of Russian gas. The commission’s recommendations were enacted into law at the end of 2022. Here is how Carter characterizes the result:

In mid-September, Weber received an urgent note from the German Ministry of Economic Affairs. Would she be interested in serving on an official government commission to contain gas and heating prices? She took the job, and, within a few weeks, the commission had settled on her price-control plan as the solution…The German “price brake” is currently scheduled to run through April, 2024.

The other people on the commission, however, tell a very different story. Veronika Grimm, who co-chaired the commission, was incensed at Carter’s description of the policy, calling it “bad journalism”:

I spoke directly with another member of the German commission, who provided some details as to the final policy differed from Weber’s suggestions. There were some differences that I consider fairly minor — whether the government supports were done at the building or household level, how much gas consumption the government would support for each building, etc. The biggest difference appears to be that Weber wanted government support for gas consumption by industry, not just by households. In any case, both Grimm and the commissioner I spoke to seem convinced that a significant portion of their effort during the deliberations was devoted to (successfully) resisting Weber’s proposals.

That might, of course, be a biased interpretation of what happened. But the broader point, I think, is that what Germany ultimately did was not actually a price control on natural gas.

A true price control is an unfunded mandate; the government says that if you raise prices past a certain amount, you will be punished, and that’s that. The German scheme implemented in 2022, in contrast, is a government subsidy. There is no law about how much utilities are allowed to charge; instead, the government writes people checks to buy gas. How much of a check the government writes you is dependent on A) how much utilities are charging for gas, and B) how much gas a particular building used in the past.

In other words, if utilities want to charge more for gas, they can. The consumers still decide how much to consume, and the government simply picks up more of the bill. If gas prices were previously high because of utilities opportunistically gouging German consumers, as the “greedflation” proponents believe, well, now those gas producers are able to opportunistically gouge the German government — and by extension, the German taxpayer — instead.

I do not see any accuracy in calling that sort of subsidy a “price control”. It is true that from the end user’s point of view, the cost is reduced. But the price paid to the producer is not.

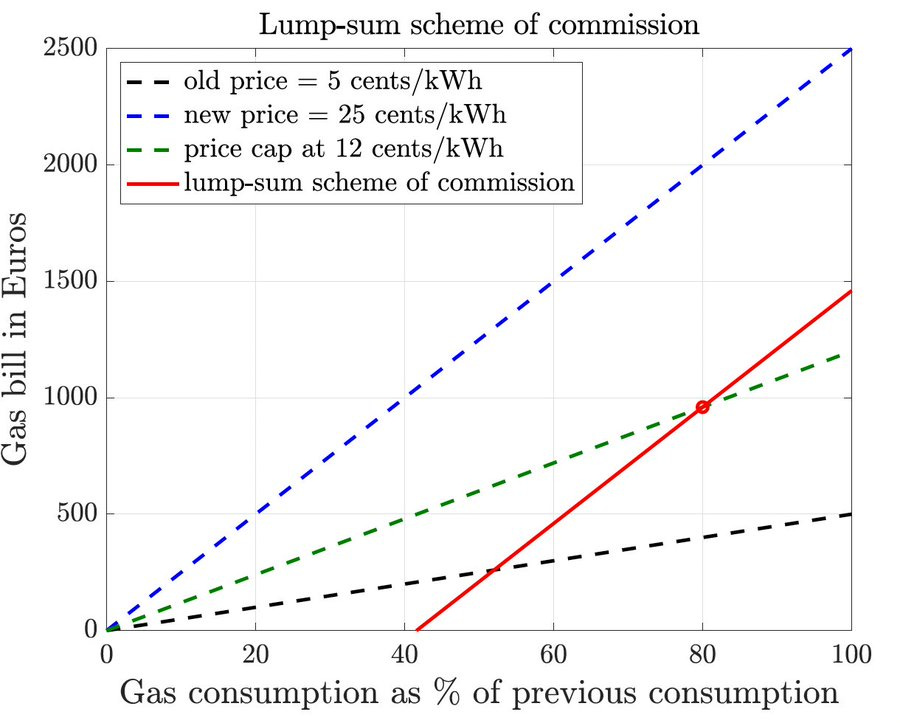

In fact, the German plan doesn’t even really cap the price that the user pays. The economist Ben Moll has a long thread explaining the difference. Basically, the German policy gives consumers a lump-sum subsidy to pay for a certain amount of gas (based on their historical gas consumption), and if they want to buy more, they pay full price to the utility. Here’s a diagram that Moll made to show the difference. The government writes a check to your utility to buy you a little over 40% of the gas that you bought last year, and after that you pay the utility full price:

Unlike a scheme that has the government subsidize gas consumption at any level, this scheme maintains the price incentive for households to conserve gas.

In other words, Carter has significantly mischaracterized the policy that Germany implemented. It is not a government limit on the price utilities are allowed to charge, and it doesn’t even cap the price that the user pays. Perhaps a true price control or a true user price cap would be better than what the German government did; I personally have my doubts. But it doesn’t look much like the ideas in Weber’s paper with Wasner, or the ideas that Carter presents in his article as having triumphed in the court of public policy.

Update: Weber herself characterizes the German scheme quite accurately, noting that the “price cap” is a subsidy that preserves “marginal prices”.

Again, a victory lap is not yet warranted. (Here is a post by Matt Bruenig making the same point, but more succinctly.)

“Greedflation”: still not a clear theory, still not vindicated by data

In addition to the policy ideas around price controls, Weber is a proponent of the idea of “greedflation”. Her paper with Wasner has a theory of what that means, and how it’s supposed to work. The theory is basically game-theoretic — it relies on ideas about strategic interactions between companies that end up causing inflation at the macro level. But because the game structure is not explicitly specified, it’s difficult to tell exactly how Weber thinks the strategic interaction is working. For example, on p. 189, Weber writes:

Firms do not lower prices, as doing so may spark a price war. Firms compete over market shares, but if they lower prices to gain territory from other firms, they must expect their competitors to respond by lowering their prices in turn. This can result in a race to the bottom which destroys profitability in the industry. Price wars are very risky for firms that are already in the market and are therefore typically launched by new entrants.

This leaves me with many questions. Do Weber and Wasner think incumbent firms never lower prices? (That’s obviously wrong.) Or do they just not lower prices in specific situations? What’s different about the situations where firms refuse to lower prices? What does it mean to “gain territory” from other firms, and how does that work? Where does the “race to the bottom” end? And so on. Mainstream economists specify the answers to these questions by writing out strategic interactions explicitly in the form of game theory; this approach certainly has its drawbacks, but at least it allows the reader to start to think about how to falsify or confirm the theory being presented.

And how is the above assertion supported? Weber and Wasner cite A) a number of economists from the early 20th century, whose observations of markets she claims to have distilled, and B) recent earnings calls by a few public corporations. I would not label this support “crap”, but neither do I believe that it’s sufficient to support the assertions about how strategic pricing interactions work. Sraffa, Kalecki, Galbraith, Robinson, etc. were all very smart people, and I am sure their close observations of firm behavior were useful and carefully made. But they were working decades ago, without the benefit of modern empirical data collection methods and analysis techniques; a lot of important work on strategic interaction between companies has been done since the 1950s, and I think Weber and Wasner should take it into account. The strategic landscape businesses face may have changed as well. As for corporate earnings calls…public-facing corporate statements can offer clues as to how companies behave and interact, but that’s more of a jumping-off point for the development of a theory rather than evidence confirming a theory.

The whole paper is like this, more or less. It feels like a proto-theory — a collection of ideas that might offer a good description of how pricing works in a modern economy, but one that needs to be made more concrete before we can properly evaluate how accurately it describes reality. And we should definitely test any theory as best we can, before using it to make policy.

But if the mechanism of “greedflation” (a term neither Weber or Carter uses, but which others use to describe the general) is unclear in Weber’s paper, it’s far less clear what Carter means when he talks about Weber’s theory. For example, Carter writes:

Analysts at the French investment bank Société Général and the European Central Bank now take much of Weber’s analysis for granted.

Do they? Both of the analyses Carter cites show only that profits have risen as prices have risen. For example, the ECB’s post shows a chart decomposing EU price hikes into profit increases, wage increases, and taxes, and productivity changes. In recent months, profits have accounted for about half of the change:

But this is merely an accounting exercise; it doesn’t tell us what caused what, or how. As so often in this debate, the “greedflation” proponents take correlation as proof of causation.

The ECB writes:

Inflation in the euro area has been high recently, mainly because of a surge in energy prices. Since the euro area imports more than half of the energy it uses and energy has become much more expensive, households and firms have lost real income. This has been made worse by supply chain problems which have also driven up import prices. In such a situation, firms have an incentive to try to minimise their share of the burden by raising their prices in order to protect their profit margins. Producers in some sectors might even try to increase their margins over and above what would be justified by higher input costs to also fully recoup previous real income losses from the various shocks of the past three years. Another motivation could be the attempt to build buffers in an environment of high uncertainty.

One of these potential explanations — protecting profit margins — is similar to what Weber and Wasner describe in their paper (I think). But the other two — recouping earlier losses or building buffers against uncertainty — are not. So Carter’s assertion that the ECB now takes “much of Weber’s analysis for granted” is unsupported. Instead, they list a variety of possible mechanisms.

Carter also writes:

Weber’s fundamental point that corporate profits are a key driver of today’s inflation is now openly embraced by the establishment on multiple continents. Researchers at the Kansas City Federal Reserve recently concluded that corporate price markups may have accounted for more than half of the inflation experienced by the U.S. in 2021.

But it does not appear that Carter has closely read the Kansas City Fed paper that he cites as support for Weber’s theories. Here are some excerpts from that paper:

[O]ne potential [inflation] explanation that has received significant public attention is “greedflation”—that is, the idea that firms are capitalizing on their market power by raising their prices higher and faster than the growth in their production costs…

We present evidence that the timing and cross-industry patterns of markup growth are more consistent with firms raising prices in anticipation of future cost increases, rather than an increase in monopoly power or higher demand…

Therefore, inflation cannot be explained by a persistent increase in market power after the pandemic. Second, if monopolists raising prices in the face of higher demand were driving markup growth, we would expect firms with larger increases in current demand to have accordingly larger markups. Instead, markup growth was similar across industries that experienced very different levels of demand (and inflation) in 2021.

Although markup growth was high in 2021, the evidence from the previous section casts doubt on the simple explanation of “greedflation,” understood as either an increase in monopoly power or firms using existing power to take advantage of high demand. Instead, this evidence may be consistent with an alternative explanation: that firms are raising markups in the present to smooth price increases they expect in the future. Indeed, both the hump shape of aggregate markup growth and similarity in markup growth across industries arise naturally in standard macroeconomic models[.] (emphasis mine)

In other words, the Kansas City Fed paper presents evidence against Weber’s claim that market power is responsible for increased inflation, and instead concludes that “standard macroeconomic models” account for what’s going on. This is exactly the opposite of what Carter claims in his New Yorker article!

I should note that many other economics writers have made the same mistake; only a few, such as Matt Bruenig, appear to have actually read the paper. If I were a researcher, it would be absolutely maddening to see the journalistic establishment use my research to claim exactly the opposite of what I wrote.

In any case, the lack of a clear theory of the how “greedflation” works, along with the general lack of evidence in favor of the idea, is yet another reason why Carter’s triumphalism is very premature.

Paradigm shifts are harder than this

Throughout this post, I may have sounded like a defender of the mainstream economic orthodoxy, but I’m really not. In fact, I think that the entire field of macroeconomics still knows relatively little about how things like inflation work! The big disagreements over the causes of the current inflation speak to the ignorance of the experts.

And on top of that, I do believe that there is a very important heterodox revolution brewing in the field of growth, development, and trade! The old consensus in favor of free trade and market liberalization is rapidly on the way out, and industrial policy looks set to replace it. When we tell the story of that shift, we will undoubtedly tell it in terms of the hallowed Iconoclast’s Journey, and the heroes of our story will be people like Ha-Joon Chang, Alice Amsden, Dani Rodrik, and Nathan Lane. We don’t yet know exactly what the new paradigm will look like, and it’s too early for a victory lap on industrial policy as well. But I think we’re starting to see that the economic establishment really did fall down on the job when it comes to growth and trade policy, and that heterodox thinkers from outside were able to find crucial insights that the mainstream had overlooked.

On price controls and the whole “greedflation” idea, I simply think we’re just nowhere near even that initial glimmer of paradigm shift yet. I think it’s important to formulate and test clear theories of how companies’ strategic behavior can exacerbate inflation. Price controls, meanwhile, are an interesting idea, and even though I think they’re probably a bad idea, they deserve more empirical investigation. But as thoughtful and smart as Isabella Weber and other proponents of the idea may be, we are very far from being able to justify the sort of triumphalist language that Zachary Carter employs in his New Yorker article. That article’s numerous mischaracterizations of inflation data, policy specifics, and research results show that it is driven more by narrative than by a hard reading of the facts.

A narrative is a powerful but dangerous thing when making economic policy. It’s hard or even impossible to avoid narrative construction entirely, but there’s always the danger that the field will go not to who has the most facts, but to who has the most appealing story. As someone who writes narratives every day, I’m all too aware of this problem, and of the inordinate power that I wield. That power should come with responsibility.

So what can econ writers do? Well, one thing is to talk to academics and listen to what they have to say. That doesn’t mean I’m in favor of academic gatekeeping; just because an idea isn’t published in the American Economic Review doesn’t mean it’s a bad one, and academic macroeconomists make big mistakes all the time. But if more journalists bothered to talk to professors in the field, they wouldn’t routinely mischaracterize the findings of papers like the one from the Kansas City Fed (or uncritically cite the people who make such mischaracterizations).

Someday it may be time to write about how a few pioneering heterodox scholars overturned mainstream thinking on inflation’s causes and cures. But that day is not today. Don’t jump the gun.

Remember how Stephanie Kelton and the MMT people have suddenly evaporated now that inflation has come roaring back?

Were Weber's ideas to be implemented, I would expect a similar evaporation as they imploded as well.

Jonah Salk cured polio and then spent 30 years trying to cure the common cold with vitamin C. Sometimes, the heterodox researchers aren't eccentric, countercultural geniuses; sometimes they're just wrong.

Great piece. I’m with you that the lack of an explicit model is frustrating. For example, she has said that in the face of a bottleneck, I know my competitor can’t increase Q so I raise P and that this is “no longer constrained by competition.” But that’s exactly what happens in competitive markets! See first half of this post https://www.economicforces.xyz/p/inflation-or-when-can-honda-raise