Insurance companies aren't the main villain of the U.S. health system

It's mostly the providers overcharging you, not the middlemen.

“I’d rather die than owe the hospital til I get old” — Courtney Barnett

When UnitedHealthcare CEO Brian Thompson was gunned down in the street in cold blood the other day, a bunch of people on the internet gloated and cheered:

The jokes came streaming in on every social-media platform, in the comments underneath every news article. “I’m sorry, prior authorization is required for thoughts and prayers,” someone commented on TikTok, a response that got more than fifteen thousand likes. “Does he have a history of shootings? Denied coverage,” another person wrote, under an Instagram post from CNN. On X, someone posted, with the caption “My official response to the UHC CEO’s murder,” an infographic comparing wealth distribution in late eighteenth-century France to wealth distribution in present-day America…On LinkedIn, where users post with their real names and employment histories, UnitedHealth Group had to turn off comments on its post about Thompson’s death—thousands of people were liking and hearting it, with a few even giving it the “clapping” reaction. The company also turned off comments on Facebook, where, as of midday Thursday, a post about Thompson had received more than thirty-six thousand “laugh” reactions.

In general, I think it’s a very bad look to endorse murder. And I think this kind of thing is a sign of how stressed-out and mentally unbalanced our country is after an era of unrest. (The chief suspect, who was just apprehended, looks like a random crazy guy rather than a leftist ideologue.)

But more fundamentally, I think the outpouring of schadenfreude1 at Thompson’s killing reflects some deep-seated popular misconceptions about the U.S. health care industry. A whole lot of people — maybe even most people — seem to regard health insurance companies as the main villains in the system, when in fact they’re only a very minor source of the problems.

All my life, Americans have been raging at health insurers. Who could forget this clip from the 1997 movie As Good as It Gets?

It’s not hard to understand why people hate health insurers. When you interact with the U.S. health care system, the providers — the hospital staff, the doctor, the nurses, the technicians — all just take care of you. The only time they ask you for money during your doctor visit is when you pay your copay at the front desk, and that’s usually not that big — if the bill is big, they’ll send it to you later. So for the most part, your interaction with the providers is just you walking up and asking to be taken care of, and them taking care of you.

Your interaction with the health insurer, on the other hand, feels like a struggle against an enemy who wants to destroy you. If you get a big hospital bill days after your visit, it’s because the insurer wouldn’t cover the whole cost. If the bill is a surprise because the provider didn’t tell you they were out of network, that also feels like the insurance company’s fault — why wasn’t that provider in their network?

Even more terrifying is when insurers deny coverage completely, which happens to about 10-20% of claims. It feels like you’ve been robbed. You paid this company a hefty premium every month, and in exchange you expected them to pay for your health care if you needed it. And now you needed it, and they won’t even uphold their end of the bargain? Why were you even paying them the premium in the first place?

Everyone knows that denying claims is in the insurance company’s financial interest. The more they can get away with taking your monthly premium and then weaseling out of their end of the bargain, the more their shareholders and executives can walk away with giant bags of money. They’re the ones buying huge houses and yachts and whatever on the money they made from finding some technical reason to send you and thousands upon thousands of people like you into medical bankruptcy after your chemotherapy. Who wouldn’t be mad?

And yet when we take a hard look at the question of why Americans pay so much more for their health care than people elsewhere in the developed world, insurance companies and their profits just aren’t that big of a piece of the story.

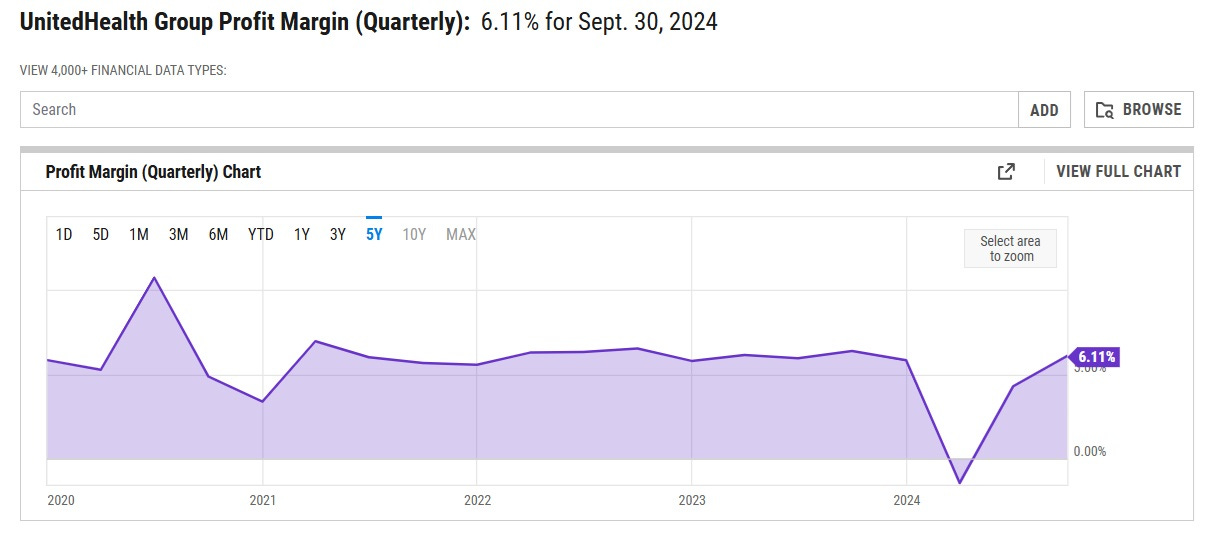

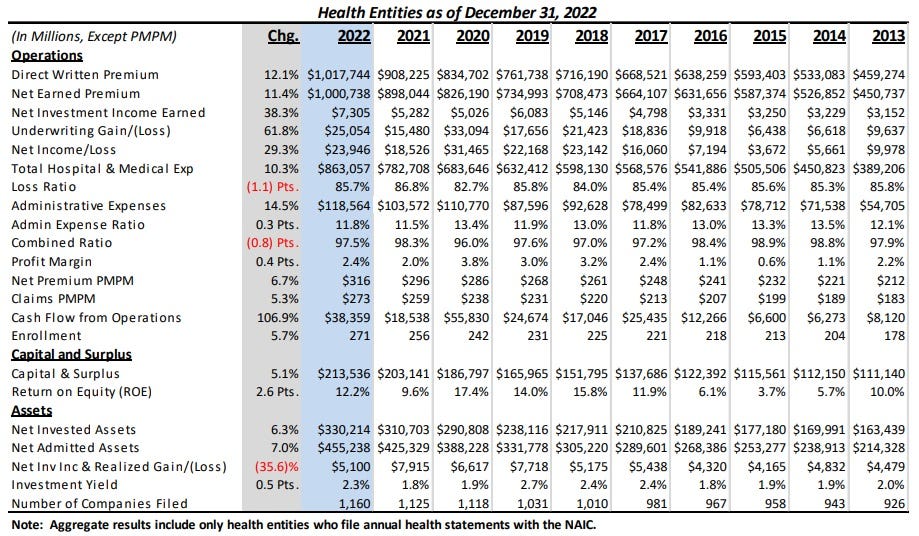

First of all, insurance companies just don’t make that much profit. UnitedHealth Group, the company of which Brian Thompson’s UnitedHealthcare is a subsidiary, is the most valuable private health insurer in the country in terms of market capitalization, and the one with the largest market share. Its net profit margin is just 6.11%:

That’s only about half of the average profit margin of companies in the S&P 500. And other big insurers are even less profitable. Elevance Health, the second-biggest, has a margin of between 2% and 4%. Centene’s margin is usually around 1% to 2%. Cigna Group’s margin is usually around 2% to 3%. And so on. These companies are just making very little profit at all.

Here’s another way of visualizing that:

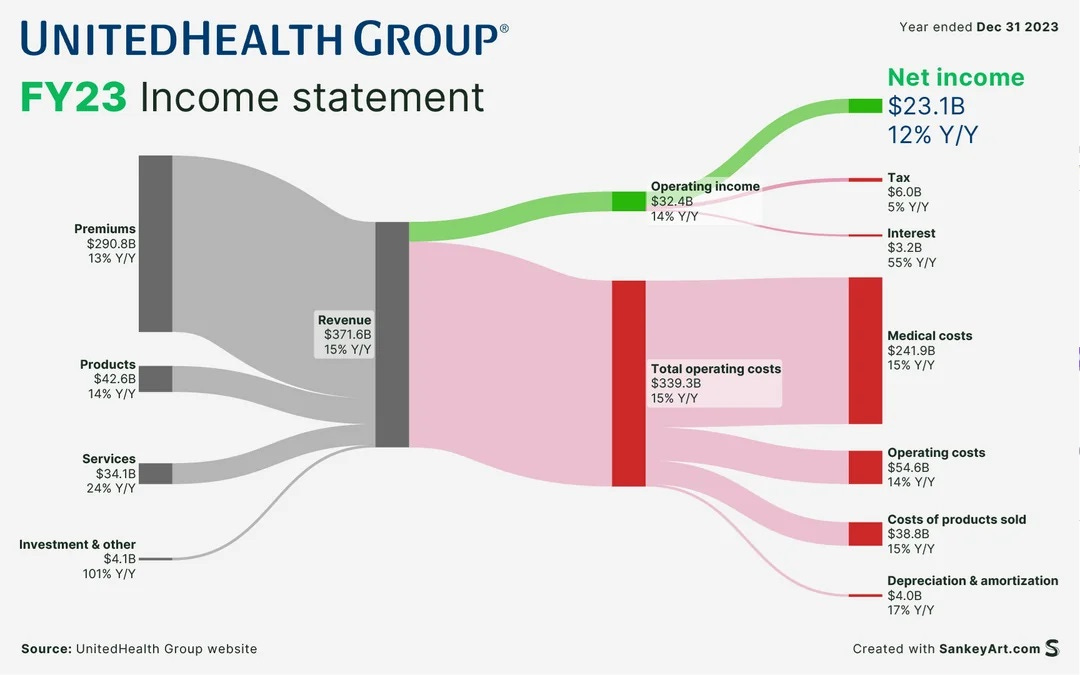

You can see that the company’s net income — i.e., its total profit — was $23.1 billion in 2023. That’s a lot of money, but it pales in comparison to the $241.9 billion that the company spent on medical costs.2 Even the company’s $54.6 billion in operating costs — of which Brian Thompson’s own $10 million salary represented 0.018% — are dwarfed by actual medical costs.

What does this mean? It means that if UnitedHealth Group decided to donate every single dollar of its profit to buying Americans more health care, it would only be able to pay for about 9.3% more health care than it’s already paying for. If it donated all of its executives’ salaries to the effort, it would not be much more than that.

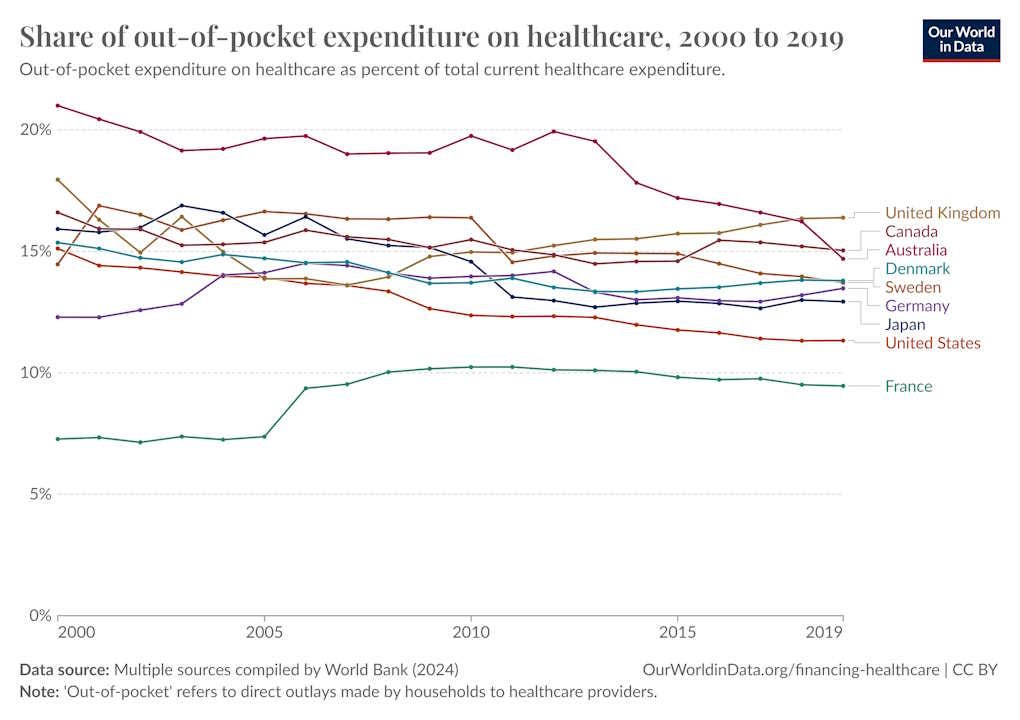

What about those denials of coverage, copays, deductibles, and so on? In fact, Americans are paying a smaller percentage of their health costs out of pocket than people in most other rich countries!

Note that the song lyric at the top of this post, about a woman in anaphylactic shock worrying that she won’t be able to afford her hospital bills, is from a band in Australia, not the U.S. This isn’t a coincidence — although Australian medical costs are fairly low, the proportion they pay out of pocket is unusually high.

In other words, Americans’ much-hated private health insurers are paying a higher percent of the cost of Americans’ health care than the government insurance systems of Sweden and Denmark and the UK are paying. The only reason Americans’ bills are higher is that U.S. health care provision costs so much more in the first place.

On top of all that, health insurance companies don’t actually look very inefficient, in terms of their administrative costs. Yes, we all know that the fragmented U.S. health system is a paperwork nightmare, with different providers and insurers drowning each other in forms and approvals. And Elizabeth Warren has claimed that switching to national health insurance would save huge amounts of money by reducing administrative costs. But when we look at United Health Group’s operating costs in the diagram above, they’re only 22.6% of the actual cost of medical care.

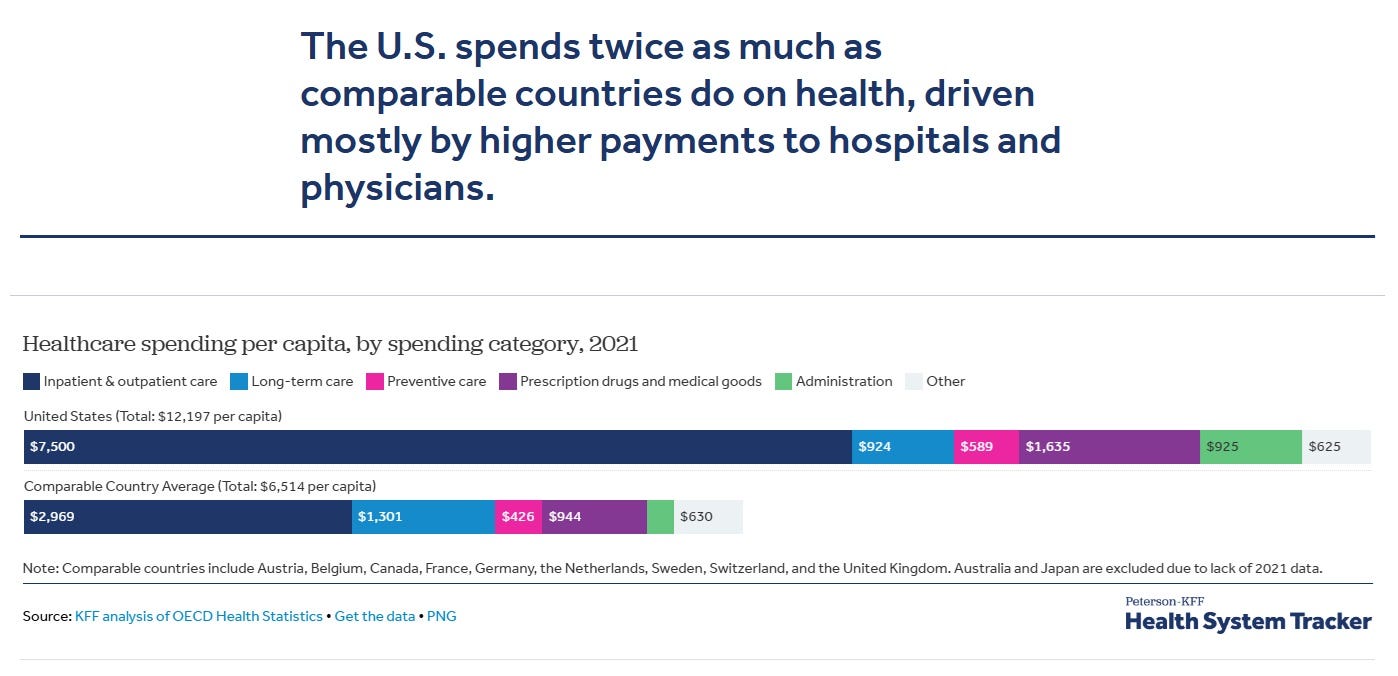

In fact, the Kaiser Family Foundation does detailed comparisons between U.S. health care spending and spending in other developed countries. And it has concluded that most of this excess spending comes from providers — from hospitals, pharma companies, doctors, nurses, tech suppliers, and so on:

This means that eliminating all administrative waste and inefficiency in the entire U.S. health care system — not just at insurance companies, but administration of government insurance programs — could save Americans at most about $680 per person every year, and probably not anywhere close to that amount.3 A few hundred bucks a year is not nothing, but it’s only a small fraction of the $5683 more that we pay relative to other countries.

So the fundamental reason your health care costs so much is not that the health insurance companies are lining their pockets. And it’s not that insurers are an inefficient mess. It’s that the actual provision of America’s health care itself just costs way too much in the first place.

The actual people charging you an arm and a leg for your care, and putting you at risk of medical bankruptcy, are the providers themselves. The smiling doctor who writes you prescriptions and sends you to the MRI and refers you to a specialist without ever asking you for money knows full well that you’re going to end up having to wrangle with the insurance company for the cost of all those services. The gentle nurse who sets up your IV doesn’t tell you whether each dose of drugs through the IV could set you back hundreds of dollars, but they know. When the polite administrative assistants at the front desk send you back to treatment without telling you that their services are out of your network, it’s because they didn’t bother to check. The executives making millions at “nonprofit” hospitals, and the shareholders making billions on the profits of companies that supply and contract with those hospitals, are people you never see and probably don’t even think about.

Excessive prices charged by health care providers are overwhelmingly the reason why Americans’ health care costs so cripplingly much. But they’ve outsourced the actual collection of those fees to insurance companies, so that your experience in the medical system feels smooth and friendly and comfortable. The insurance companies are simply hired to play the bad guy — and they’re paid a relatively modest fee for that service. So you get to hate UnitedHealthcare and Cigna, while the real people taking away your life’s savings and putting you at risk of bankruptcy get to play Mother Theresa.

So the way to make our health care system affordable is not to browbeat insurers, in the hope that they will be able to reduce their profits and pay for us to have cheap health care. Insurance companies simply do not have the power to do that, even if you threaten to shoot them. What we need is to reduce costs within the actual medical system itself. One idea is to have the government insurance system play hardball with providers, negotiating lower prices. is what the Biden administration had Medicare do with some drug companies. There are some risks to this approach — if it’s executed clumsily it can suppress innovation — but it’s basically what every other rich country does, so the track record is decent. There are probably other ways to foster competition and increase efficiency in the medical care system.

But focusing all our anger on the middlemen of the U.S.’ bloated health care system is just a way of shooting the messenger.

Update: Matt Bruenig argues that insurers really are to blame. He claims that inefficiency in the system is a bigger driver of costs than I realize, because providers have to spend money dealing with insurers — something the KFF numbers don’t include. He also alleges that some of this “inefficiency” is actually intentional on the part of the insurers — a disguised way to pay themselves out.

But I don’t think this passes the smell test. If insurers were so good at extracting money from the system, why are they so unprofitable? The average company in the S&P 500 has a profit margin of 12%, but these insurers have margins of 1% to 3%. If they’re so good at extracting money from providers, why are shareholders — and executives who own stock — not getting a piece of that money? It doesn’t make sense.

Also, provider-side administrative costs don’t just include the money providers spend wrangling with insurers — it includes the money they spend on the executives, managers, and billing departments who figure out how to charge patients $700 for every injection of IV drugs, or hundreds of dollars for a hospital pillow, or $10,000 for an MRI.

So no, I don’t buy Bruenig’s argument here. Though I still do agree with him that national health insurance would be a good idea — mostly for the negotiating power, not for the administrative cost savings.

Update 2: Over at Tyler Cowen’s blog, a commenter argues that profit margins are not a good guide to the financial success of a business, and that instead one should look at return on equity (ROE). That’s fine, I wasn’t talking about the financial success of health insurance companies; I was simply showing that they don’t have the ability to pay for much more health care than they’re currently paying for. But for what it’s worth, the ROE of health insurers is pretty low. The S&P 500’s weighted average ROE is usually around 15%, and has been a bit higher lately. Here’s what health insurers were earning:

They had a couple of good years in there, but in general it’s underwhelming. UnitedHealth Group, which does include businesses other than the low-margin health insurance business (e.g. providing health care and pharmaceuticals), is doing pretty well with 26%.

But if you look at the list of companies with the highest ROE, you see health care providers or suppliers like HCA Healthcare (272%), Cencora (234%), Abbvie (84%), Mckesson (84%), Novo Nordisk (72%), Eli Lilly (59%), Amgen (56%), IDEXX Laboratories (53%), Zoetis (46%), Novartis (44%), Edwards Lifesciences (43%), and so on. If you want to know which shareholders are making the real money in the health care industry…well, it’s the shareholders of those providers and suppliers.

Update: Here’s a good Bloomberg story on predatory pricing by hospitals. Hopsitals bilk insurers, who are forced to pass on the higher costs to patients, who then blame the insurers instead of the hospitals.

Corrections: A previous version of this post said that Courtney Barnett is British. She is Australian (but is an excellent artist regardless of location). Also, a previous version mistakenly claimed that providers’ billing administration is included in the KFF’s estimate of administrative costs; it is not included.

I got the spelling right on the first try. Please clap.

In fact, the actual health insurance business — taking premiums and paying out claims — is even less profitable than these numbers might suggest. As Axios recently reported, insurers’ profits are increasingly coming from other lines of business.

One reason it couldn’t save nearly that much is that Americans’ salaries are much higher than those in the average country.

I agree that health insurers are not the main culprit of the high cost of healthcare in the US. However, your arguments that’s it’s the “providers” knowingly charging the patient which leads to the high cost is in my opinion part right/part wrong and extremely oversimplistic.

I am an infectious diseases physician to get my bias out there first. In my view the reasons costs of high are many fold but some of the highlights

1: The way care is compensated. The AMA created a compendium of codes (CPT) and assigned value to each (RVU). Medicare then decides how much to pay for each RVU. This is used as a surrogate of productivity and the way physicians are both judged and paid. Procedures have long been given more “value” so physicians who practice procedures are paid more (surgeons, cardiologists, dermatologists). This incentivizes providers to do “things” to generate RVU and does not incentivize prevention of disease. For example: I am in the lowest paid field of medicine because I have perform zero procedures and much of my job is stopping antibiotics or switching them to cheaper ones. This leads to much more expensive treatment as opposed to prevention.

2. The system is fragmented and Byzantine. Most physicians have no idea how much each test costs or what will lead to the lowest cost for the patient. Your example - MRI - this cost wildly varies and is based purely on the cost insurance has negotiated with various operators of MRI. If I could give patients a flyer the cost of an MRI by location and point them to the cheapest I would! But I have no freaking clue. I think the fragmentation also leads to many other inefficiencies that raise the cost of care.

3. Litigation. The US is extremely litigious and the fear of a lawsuit leads to physicians to practice defensive medicine in ambiguous situations (which in medicine is common). Some physicians pay > 100K for insurance even those who have never been used.

These are just the three I could write down on my train ride home. The whole system is not great and was made by accident in the 1940s-1960s. Providers are part of the problem but I just don’t think we are the only problem and a solution needs to tackle it all not just blaming doctors and nurses for pulling a fast one on patients.

“it’s mostly the providers overcharging you” - i think i know what you’re trying to say (that healthcare is expensive in usa), but this isn’t up to the doctors or nurses you mention (and we don’t secretly know costs as you say, this is negotiated btwn insurance plans and hospitals) and little of it is going to the physician and nurse as your statement seems to imply. physician services are something like 15% of healthcare expenditures in usa.