I’m going to be writing more about inflation, monetary policy, etc. in the coming days. But I thought that today I’d repost something I wrote for my old blog back in 2016, about the macroeconomic theories of Milton Friedman.

The 1970s were an era of great macroeconomic turmoil — persistent inflation, recessions, and falling wages. Out of that chaos came a great intellectual ferment in the economics profession. The greatest macroeconomic thinkers of the age struggled to figure out why inflation had gone up, why it wasn’t going down, how high unemployment could coexist with high inflation, and how the government might correct the situation. Out of that explosion of ideas, for better or for worse, came pretty much all of modern macroeconomics.

Milton Friedman was right at the heart of that intellectual ferment. His ideas didn’t stay constant over time (as you’ll see in the post below), but he was always injecting something interesting into the mix. Fed Chair Paul Volcker’s eventual conquest of inflation — at the cost of a deep recession — owed much to Friedman’s ideas.

But macroeconomics is an incredibly hard thing to get right. It’s very hard to empirically test any of the theories — at best you can make policy, and wait for history to happen, and then observe whether you kinda-sorta got it right. So how are Milton Friedman’s macroeconomic ideas holding up now? The post below explores this question.

I recently wrote a Bloomberg View post about consumption Euler equations, and how these are increasingly being targeted as a broken piece of macroeconomics. I traced the idea back to Milton Friedman and the Permanent Income Hypothesis, and Bloomberg decided (wisely) to go with Friedman for the headline. "Economists Give Up on Milton Friedman's Biggest Idea" is probably going to get orders of magnitude more clicks than "Economists Search for Replacement for Infinitely Lived Perfectly Far-Sighted Model of Consumption Smoothing".

BUT, anyway, Emily Skarbek decided that Uncle Miltie needed some defending, and wrote a blog post praising his legacy. Most of the post discusses stuff that I didn't touch on in my Bloomberg post, since I was only talking about the PIH. So I decided to do a post about Milton Friedman's overall legacy - actually, much too big a topic to do justice to in one post, but hey, that never stopped anyone before, so what the heck! I pitched it to Bloomberg, and they said "But didn't you just do a Milton Friedman post??", so on the blog it goes.

For some reason, Friedman is treated a bit like a secular saint in policy discussions. If you criticize "Idea X", fine. We can have an argument. But if you criticize "Milton Friedman's Idea X", then WHO ARE YOU, LOWLY WORM, to criticize the great FRIEDMAN?? If you say government is a lot more useful and important than Reagan and Thatcher and Art Laffer and Friedrich Hayek and Ed Prescott and Greg Mankiw think, well, fine, that's your opinion. But if you say government is a lot more useful and important than Milton Friedman thought, then you're wrong wrong wrong and don't you know that Friedman proved government was bad in the 70s?? Etc.

OK, I might be exaggerating as an excuse to use lots of capital letters and italics, but Friedman is such a towering intellectual that criticizing him does feel a bit like tipping a sacred cow. Fortunately I'm from Texas, where cow-tipping is a way of life.

So I, a nobody, shall proceed to grade the multifarious ideas of the great Friedman. As of 2016, how is each of Friedman's ideas holding up?

As I wrote for the Bloomberg post, economists figured out by the 90s that the PIH doesn't look strictly true - there are lots of hand-to-mouth consumers out there. And natural experiments tend to find that people consume windfalls to a fair degree. What we don't know is why some consumers smooth and some consume hand-to-mouth, or whether and how it's state-contingent. Yes, the idea of a mechanical hand-to-mouth consumption function is dead - many people obviously are forward-looking to some degree under many conditions. But the strong form of the PIH - perfectly forward-looking consumption smoothing - doesn't look like a good approximation to reality.

Oh, and here's Skarbek's defense of the concept:

It seems to me that the PIH is a useful way to understand personal investments decisions over one's lifetime. For example, why young people who expect (even if inaccurately in many cases) to have high earnings after college incur student loans instead of directly entering the workforce. Or why people take out 30 year mortgages to buy homes.

Sorry, but "I have seen instances of people borrowing large amounts of money" doesn't tell us much about consumption smoothing. But even if it did, these are not good examples. A mortgage doesn't entail taking on net debt, since the value of the loan is the same as the value of the asset you acquire. And education is generally regarded as investment, not consumption (though some might argue). So, no.

A more sophisticated defense of the PIH is that we can always find some utility function that makes it look like people are smoothing consumption. But this defense is also bad, because A) it makes the PIH totally vacuous, and B) utility-function-mining is just going to get you something that fails out of sample, and you'll have to go mine for a different function, etc.

But the most common defense is: "But the PIH doesn't say all consumers are perfect smoothers, only that people do some amount of consumption smoothing." Fair enough; β>0 is technically a hypothesis, right? But if your hypothesis is only about a sign and not a magnitude, it generally isn't that useful.

This idea was adopted in the U.S. between 1979 and 1982. But as Bennett McCallum has documented, the Fed failed to hit its targets:

[T]he Fed did not succeed in improving its record of money stock control. Instead, the realized growth rates for the years ending in the fourth quarter of 1980, 1981, and 1982 were again outside the specified target range, as indicated in Table 1-3. And monthly values of the growth rate were highly variable, as can readily be seen from Figure 1-1. This is especially striking, of course, because the special operating procedures of 1979-1982 were designed precisely for the purpose of improving money stock control so as better to achieve the monetary growth targets!

As it turns out, central banks just aren't very good at controlling the money supply. McCallum also speculates on what effects the failed attempt to target money growth rates might have had:

What, then, were the results of this experiment? In one respect the Fed's attempts were successful: by September 1982 the U.S. inflation rate had been reduced from around 11 or 12 percent (per year) to a magnitude in the vicinity of 4 or 5 percent. Other aspects of the outcome were not as planned, however, and were highly unpopular with the public and with most commentators. Of these undesirable side effects, four will be mentioned. First, short-term interest rates rose to levels unprecedented in U.S. history. Over the month of May 1981, for example, the 90-day Treasury bill rate averaged 16.3 percent. Second, the extent of month-to-month variability of interest rates was greater than ever before. Third, in 1981 a recession began that was the most severe since the Great Depression of the 1930s; the nation's overall unemployment rate climbed over 10 percent in the second half of 1982. So while the economy was relieved -- at least temporarily -- of the inflationary pressures that it had been experiencing for about a decade, this relief was apparently obtained at the cost of an unwelcome recession and the associated loss in output.

In any case, the failure of money supply targeting caused central banks to switch to a mix of interest-rate targeting and inflation targeting.

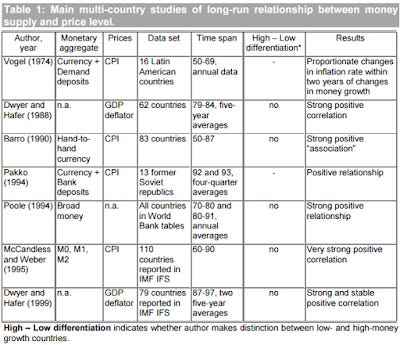

This is probably Friedman's most famous idea - the notion that "inflation is always and everywhere a monetary phenomenon." Unfortunately, it's hard to tell if it's right, because it's a vague idea. First, you have to define the money supply (Are bonds money? Etc.). Next, you have to specify the lag of the effect - if money has a long and variable lag on inflation, as Friedman thought, it'll be hard to pin it down empirically. But anyway, tests appear to be generally in favor of the hypothesis. Here's an abstract from a 2001 discussion paper by Paul DeGrauwe and Magdalena Polan:

Using a sample of about 160 countries over the last thirty years we test for the quantity theory relationship between money and inflation. When analysing the full sample of countries we find a strong positive relation between the long-run inflation and money growth rate. The relation is not, however, proportional. The strong link between inflation and money growth is almost wholly due to the presence of high (or hyper-) inflation countries in the sample. The relationship between inflation and money growth for low inflation countries (on average less than 10% per annum over the last 30 years) is weak. We find that the long-run average inflation and country-specific factors have a significant influence on the strength of the relationship. We also confirm that money growth and output growth are orthogonal in the long-run; i.e. higher growth rates of money do not lead to higher growth rates of output.

And here is a table from their literature review:

So, generally pretty good support for Friedman's idea in high inflation countries (which are probably the main cases Friedman and everyone else cared about), though not so much when inflation itself is low. In particular, at the Zero Lower Bound (or maybe just more generally in a long disinflationary stagnation after a financial crisis), velocity seems to fall off substantially:

So although high inflation appears to coincide with high money supply growth, the correlation does seem to break down for economies like ours and Japan's.

Also, studies like these can't isolate causality, so there's always the possibility that high inflation itself boosts the money supply, by increasing bank lending and/or politically forcing the central bank to print more money. To my knowledge, this is not well-known.

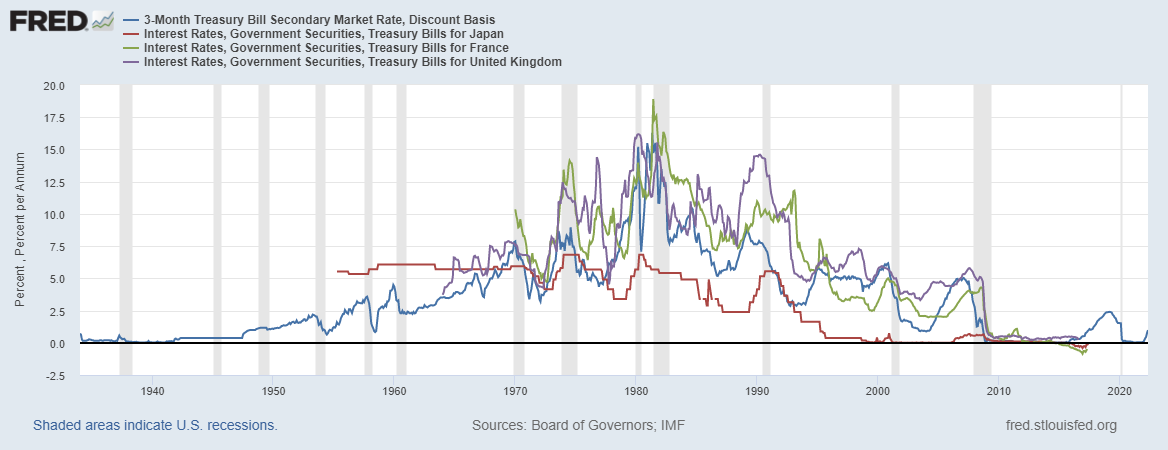

This is the idea that nominal interest rates should be set at zero. It generally contradicts the k-percent money growth rule, unless setting rates at zero just happens to make the money supply grow at a constant rate (how much of a PR badass are you if you can get your name on two mutually contradictory rules?). Interestingly, the Friedman Rule is based on Neo-Fisherism - it says that rates should be at zero because in the long run, low interest rates are deflationary and mild deflation is what we want.

The idea that deflation is good has probably not stood the test of time, as most people agree that it has been damaging to Japan's economy. People have generally agreed on inflation targets of 2 percent, rather than negative inflation targets. But interestingly, zero or near-zero nominal interest rates have now become the global norm, at least in the developed world:

So it seems to me that no one really knows what to make of the Friedman Rule. Everyone is doing it, but for essentially the opposite of the reason than Friedman envisioned. It's a weird world out there, folks.

This appears to have been a big bust. Whatever monetary policy has or hasn't done, it has proven incapable, by itself, of pulling economies out of long slumps. Meanwhile, most of the evidence we have - which is weak evidence, because it's macro, but nevertheless is all we have - seems to indicate that fiscal policy works, even if we don't understand exactly why it works (see here, here, and here for example). Moreover, there is a growing recognition that what often matters is the combination of fiscal and monetary policy, and that fiscal policy can cancel out the effects of monetary policy. This may be why governments around the world still engage in fiscal stimulus when times get rough.

The poor quality of macro data saves Friedman from getting an F on this one.

Lots of countries have certainly gotten into trouble trying to peg their exchange rate too high - this generally leads to a devaluation, capital flight, and a "sudden stop." But some countries (China) seem to have gotten some good results by pegging their exchange rates low during their catch-up growth phase, while using capital controls to prevent inflation. Also, a lot of countries have "managed floats", where they pretend to float their currencies but don't really do it. Anyway, to my knowledge, the data is just too poor and sketchy here to know which kind of exchange rate regime is really optimal, or whether this depends on the situation. Basically, I think we don't know much more about this now than we did in Friedman's day. Though I could be wrong.

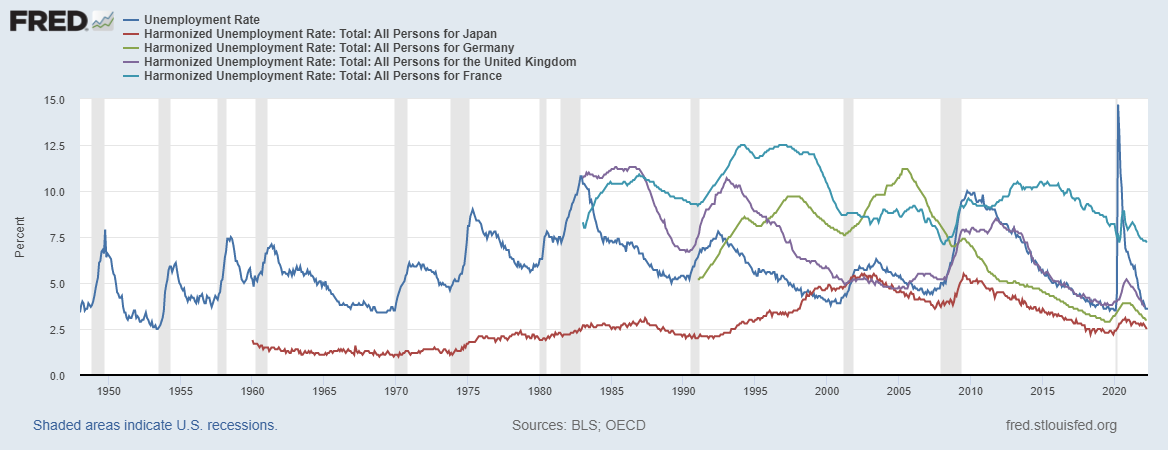

Basically, this is just the idea that unemployment is mean-reverting to some slow-moving number. Looks pretty true for the U.S., less so for other developed countries:

Of course, you can claim that in the other developed countries, big structural shifts happened that changed the natural rate. Unfortunately, that's just a fudge factor, and attempts to explain these changes with easily observable structural changes (e.g. taxes) haven't gone so well.

One one level, it's pretty obvious that there's some floor to unemployment - there will always be people between jobs, and people who don't want to work but who claim they do. The presence of a natural floor means that if a country keeps trying to put everyone to work, but keeps suffering negative shocks, unemployment will appear to oscillate. You can then draw an average line through that bouncy time series and call it the "natural rate". But in this case, the real things would be the unemployment rate floor and the average size of recessions - not the "natural rate".

So it's just not clear how useful this concept is, without some way to anticipate what the "natural rate" should be.

This is the idea that people's expectations of future inflation (or other economic variables) is basically just some moving average of recent past inflation.

In fact, we do see that people's past inflation experiences tend to influence their expectations, but at a very very long time lag - basically, people's entire life. And it might be a lifetime average rather than a moving average.

Anyway, it seems to me that if you write down models with a simple, precisely specified model for adaptive expectations, with fixed lags etc. etc., it won't fit the data very well. But things like Bayesian priors and inattention will create learning effects that make expectations look like they have an adaptive component. People don't use Friedman-style adaptive expectations in models anymore, but A) it's unclear whether what they do use works well, and B) more sophisticated learning-based models seem to be popular. So this seems like a case where a simple Friedman idea contains an important principle that shouldn't be taken too far, and inspired a line of work that is interesting and still in progress.

Most decision theory researchers now realize that risk aversion can be positive or negative depending on the size of the gamble. Friedman's specific form for the utility of consumption is probably not that useful, but the basic idea - which has persisted into theories like prospect theory, salience theory, and others - is sound. People definitely do seem to buy both life insurance and lottery tickets.

Friedman's macro ideas were enormously influential, and probably made very crucial points at the time they were introduced. However, they suffer from one fatal flaw: They are macro ideas. Macreconomics does not easily yield its truths to the probing mind, given uninformative data and the complexity of the thing. Plus, it's likely that big structural changes make it such that the discipline has few eternal verities - what describes the economy well in 1976 might have little to do with the events of 2016. So while "C+" looks like a harsh grade, I'm not sure what other macroeconomic thinker has done better. My favorite macroeconomists, like Bob Hall or Chris Sims, tend to be much more cautious and circumspect than Friedman - the smartest researchers seem to have realized that big, Friedman-style ideas will almost always fail to a substantial degree.

The main thing people know about Friedman is "inflation is always and everywhere a monetary phenomenon". You justly called it his most famous idea.

I pretty much think it's wrong.

Sure - print tons of money, don't increase supply of goods/services and you're bound to get some inflation at some point (though, the collapse in the velocity of money will work very hard against you ; so printing isn't everything - as we saw with QE. Giving money to bankers doesn't do jack shit to standard everyday prices. Asset prices otoh...)

So already we got qualifiers.

And that's before we get into things like supply shocks that can generate inflation, whatever the money supply or money printing powers do.

Also note the difference (for inflation) between the QE stuff by the Central Banks and the fiscal spending/COVID relief done by the governments. One generated at most "asset inflation", invisible by and large to the CPI or PCE while the other has gotten us an honest to God inflation crisis.

Now, you can say that the fiscal powers can only send money to people because the CB enables it by printing money but this is getting stupid/tautological. Inflation is not always and everywhere a monetary phenomenon. Indeed, it seems to be the exception rather than the norm, at least for the last 40-50 years in developed countries.

I'm skeptical of economics as a discrete branch of human thought, yet nonetheless have spent decades reading through the greats (as a lay person), from Hayek and Friedman, Adam Smith and Ricardo, Keynes and Galbraith, to Marx and neo Marxists, Lenin and Mao and MMTers.

I come to the Tolstoyian resignation that it's all so complicated, we're better off calling it God's Will, making our propitiations, keeping our heads down, and plodding on.

So I figure I should comment when I like one of your articles and say so. This analysis is more than silly spreadsheetery and humble enough to be harmless. I think grading Uncle Miltie as C-level work is fair and instructive.

{kind=link}

The main thing people know about Friedman is "inflation is always and everywhere a monetary phenomenon". You justly called it his most famous idea.

I pretty much think it's wrong.

Sure - print tons of money, don't increase supply of goods/services and you're bound to get some inflation at some point (though, the collapse in the velocity of money will work very hard against you ; so printing isn't everything - as we saw with QE. Giving money to bankers doesn't do jack shit to standard everyday prices. Asset prices otoh...)

So already we got qualifiers.

And that's before we get into things like supply shocks that can generate inflation, whatever the money supply or money printing powers do.

Also note the difference (for inflation) between the QE stuff by the Central Banks and the fiscal spending/COVID relief done by the governments. One generated at most "asset inflation", invisible by and large to the CPI or PCE while the other has gotten us an honest to God inflation crisis.

Now, you can say that the fiscal powers can only send money to people because the CB enables it by printing money but this is getting stupid/tautological. Inflation is not always and everywhere a monetary phenomenon. Indeed, it seems to be the exception rather than the norm, at least for the last 40-50 years in developed countries.

I'm skeptical of economics as a discrete branch of human thought, yet nonetheless have spent decades reading through the greats (as a lay person), from Hayek and Friedman, Adam Smith and Ricardo, Keynes and Galbraith, to Marx and neo Marxists, Lenin and Mao and MMTers.

I come to the Tolstoyian resignation that it's all so complicated, we're better off calling it God's Will, making our propitiations, keeping our heads down, and plodding on.

So I figure I should comment when I like one of your articles and say so. This analysis is more than silly spreadsheetery and humble enough to be harmless. I think grading Uncle Miltie as C-level work is fair and instructive.