Cautious optimism about Ukraine's economy

Predictions of imminent collapse are overdone.

Most of the news you read about Ukraine is about the military situation. In recent weeks, the big story has been the Ukrainian offensive that pushed the Russians out of some of the territory they had occupied in the country’s northeast. But at the same time, Ukraine is waging another battle — the battle to keep its economy afloat in wartime.

Recently I’ve seen two articles arguing that Ukraine’s economy is nearing a state of collapse — the first by Adam Tooze at his blog, and the second by Niall Ferguson in Bloomberg. But although the challenges they describe are certainly real, their outlook strikes me as far too alarmist. In fact, there are plenty of signs that Ukraine will be able to weather the economic burden of the war, and emerge as a stronger nation, ready to rebuild.

Ukraine is suffering, but stabilizing

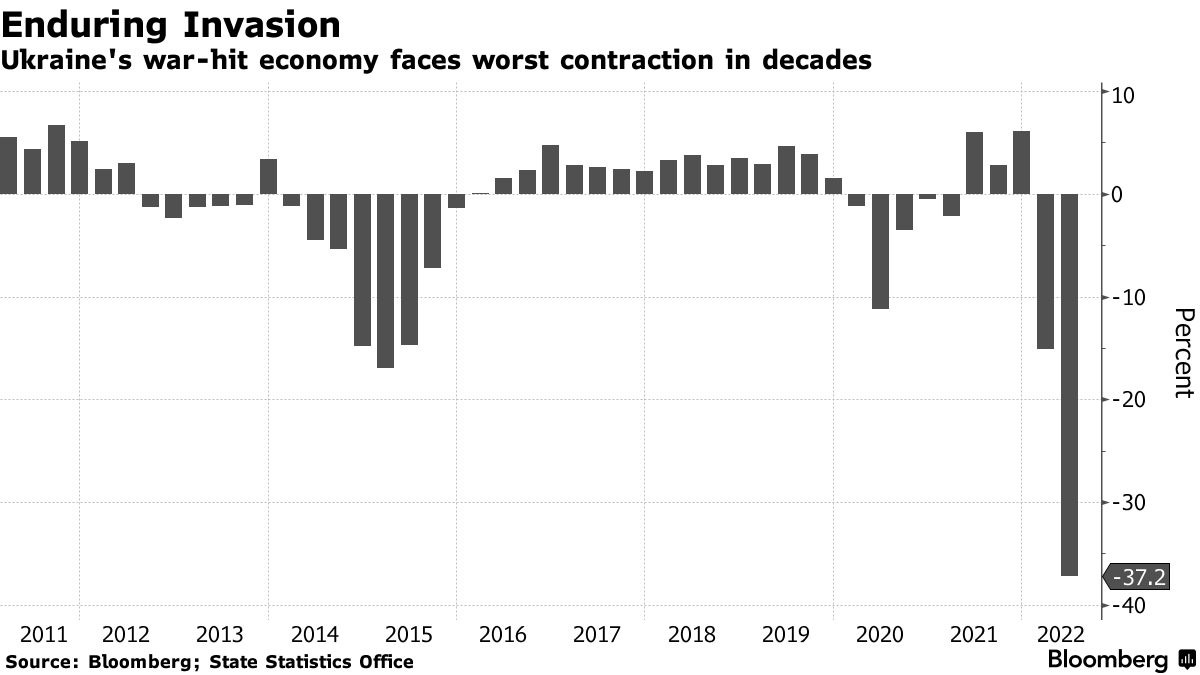

Both Tooze and Ferguson cite, first and foremost, the GDP numbers. Ukraine’s economic output was down 37% year-over-year in the second quarter:

And it’s forecast to be down 33% for the year as a whole. But remember the trickiness of year-over-year numbers — a 37% y/y decline in Q2 but only a 33% decline for all of 2022 is actually a forecast that the economy will experience a modest recovery by the end of the year. In other words, the initial economic shock of the invasion appears to be over.

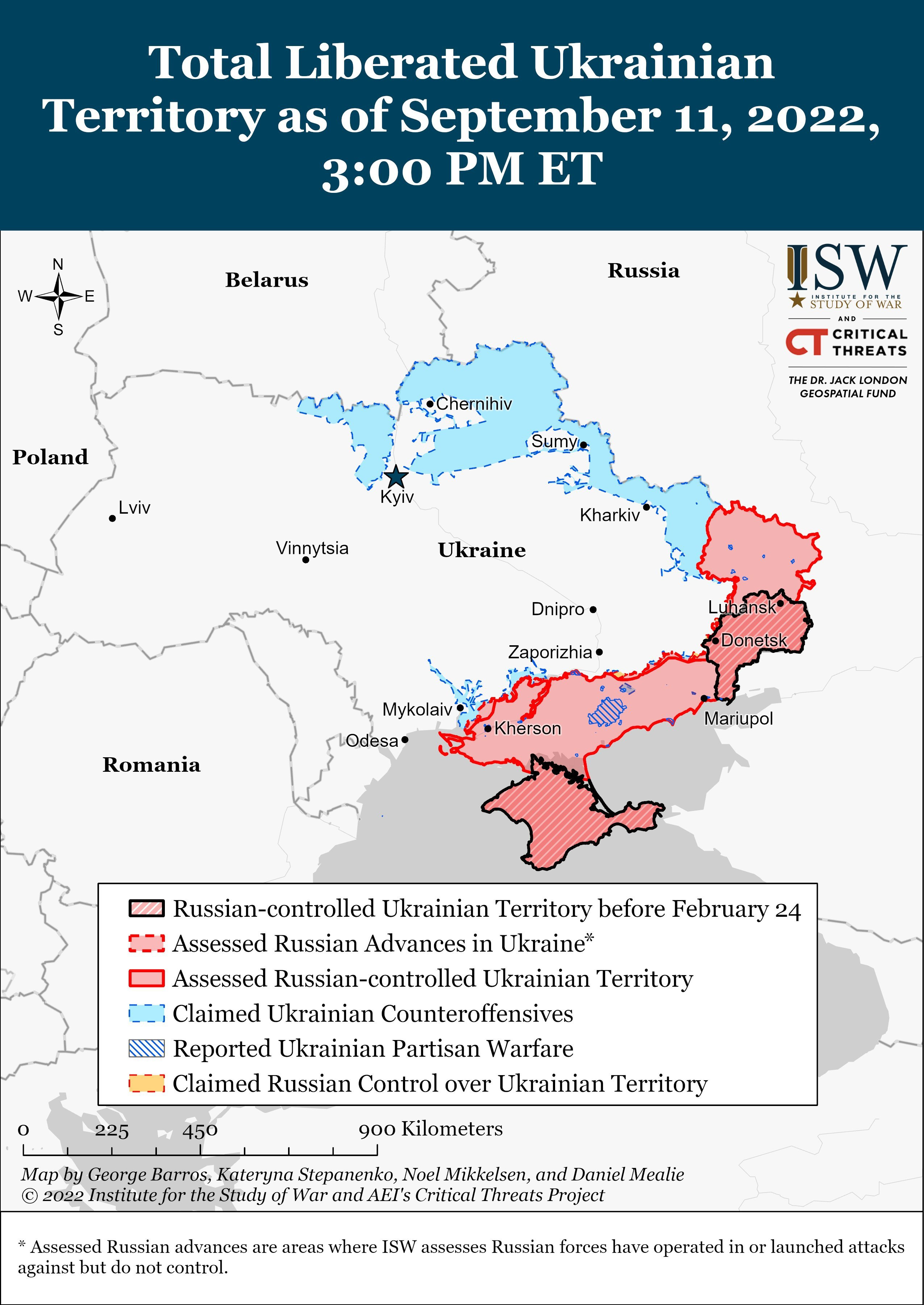

That makes sense, since Ukraine has managed to evict Russia from around half the territory they’ve conquered since February, especially the areas around the big cities of Kyiv and Kharkiv:

The Wall Street Journal has a story detailing what this stabilization looks like on the ground. Some excerpts:

Ukraine’s economy, while hurting, is stabilizing…“Things are bad but stable,” said Tymofiy Mylovanov, head of the Kyiv School of Economics. “It looks and feels like the economy is adapting.”…

Russian efforts against vital systems such as banks and the internet have been largely ineffective, and they have continued to function…Ukraine’s biggest employment website, reached more than 40,000 on a given day in August, compared with 6,000 in March. That compares with more than 100,000 vacancies in February, before the invasion…Exports of IT services were up 23% in the first half of 2022 compared with a year earlier.

If the Ukrainian economy stabilizes at two-thirds its prewar size, that’s bad, but not catastrophic. Ukraine was a lower middle income country before the war, with a per capita GDP of about $13000 — similar to Iran or Paraguay. If that drops to $8,600, Ukraine’s living standards would be more similar to those of Vietnam, El Salvador, or the Philippines. That’s a tragedy, to be sure, but those are not countries in a state of economic collapse. Countries deep in the throes of total war have endured far worse and kept on fighting.

Ukraine still faces some big immediate economic challenges. The first of these is paying for imports, especially fuel.

Ukraine will not starve or freeze

The main imports most countries have trouble paying for in economic crises are food and fuel, but Ukraine is actually good on food. Remember, this is the breadbasket of Europe, a country whose flag is literally a picture of a field of wheat under a blue sky. Ukraine’s harvest is expected to be much smaller than normal this year, but “much smaller” is relative — the grain harvest might fall from 85 million tons to 52 million, but that will still be enough to feed the whole country and export tens of millions of tons. Ukraine will not starve.

Fuel, though, is a bigger problem. Ukraine needs fuel to power its war effort, and also to heat homes during the upcoming winter. Ukraine has been able to secure sufficient fuel imports from Europe, but the question is how they will pay for this financially. Remember, in order to pay for imports, you need to get foreign currency, and there are three standard ways to do this: 1) export stuff, 2) swap your currency for foreign currencies, or 3) borrow foreign currencies.

Ukraine’s grain exports have recovered somewhat following a deal with Russia, the UN, and Turkey that allows the country to ship grain from Odesa through the Black Sea, but they’re still down by almost half from prewar levels. As the WSJ article notes, IT exports are ramping up, but the sector is still only 4% of Ukraine’s economy.

As for the second method — swapping Ukrainian hryvnia for foreign currency — this will become much harder if the exchange rate falls. Ukraine pegged the hryvnia to the dollar early on in the war, but that peg was unsustainable, because people kept moving money out of the country. The currency had to be devalued in July, and it’s now pegged again at a lower level:

This peg will also be broken if more people move their money out of Ukraine. The government is trying to prevent that in two ways — first, by imposing capital controls, and second, by raising interest rates to 25%. Raising interest rates gives investors a reason to invest in Ukrainian bonds. The recent military victories should also help restore confidence and curb further capital flight, reducing the chance of another painful currency devaluation.

The third method of paying for imports, of course, is to borrow. The country is attempting to borrow about $15-20 billion from the IMF and $5 billion from the EU this year, as well as various other loans.

Maybe I should put “loans” in quotes, though, because my bet is that most of these loans — like American “lend-lease” military aid — are going to be forgiven after the war. And that brings us to the fourth, highly nonstandard way to get foreign exchange to pay for imports — just have foreign countries give you the money. As Ferguson notes, Ukraine is currently getting quite a lot of financial support from both the U.S. and the EU — perhaps about $30 billion so far, plus substantial humanitarian and military aid:

Between massive aid, massive loans, measures to curb capital flight, recovering grain exports, and other exports such as IT, it seems likely that Ukraine will be able to keep the heaters on throughout the cold winter months, except in areas subject to massive Russian shelling.

Inflation and deficits can be curbed with wartime taxes

Other potential big problems for Ukraine include inflation and deficits. Inflation is currently running at 23% y/y. That’s not a catastrophic rate — some developing countries experience inflation at that level throughout their economic golden years. But the rate is accelerating each month, and Ukraine can’t afford to risk it spiraling out of control into a devastating hyperinflation.

The traditional way to control inflation is with high interest rates. Ukraine’s interest rates are already very high at 25%, but if inflation keeps creeping up, this might have to be raised even more. And very high interest rates come at a cost — two costs, in fact. First, by discouraging investment, high rates curb economic activity. Second, high interest rates make it even more difficult for the government to borrow money. So there’s a limit to how high rates can go before they start clobbering the economy and putting the government in danger of default.

The other way to control inflation is fiscal austerity. In fact, with interest rates very high, austerity is even more important. But spending cuts are unlikely to happen, because Ukraine’s government needs to borrow a ton of money to pay for the war. Also, as Tooze points out, Ukraine also hasn’t cut social spending much — the country traditionally has a robust welfare state, and it’s not about to slash that spending when babushkas throughout the country might freeze or starve.

The only realistic option for austerity is to raise taxes. A team of prestigious economists at the Center for Economic and Policy Research has released a report urging Ukraine to carry out a variety of tax hikes:

To support the war effort, Ukraine needs to radically improve its fiscal position…Raising tax revenues involves three basic elements. First, a stronger, larger economy provides more resources for taxation…

Second, the government can broaden the tax base…A large share of Ukraine’s workforce (approximately two million in 2021) is operating as private entrepreneurs, which allows workers to minimise their tax liability…The government can try to close this loophole, at least for some businesses for the duration of the war. More generally, the government should tax the shadow economy as households and businesses increasingly rely on cashless payments in light of elevated security risks associated with using cash. The government should also refrain from offering tax holidays, reductions, and other forms of ‘tax expenditures’…

Third, the government can raise tax rates, excises, duties, and fees. It should make taxes more progressive so that the burden of the war falls more on those who have more resources. This is desirable on both equity and social-solidarity grounds. For example, the Roosevelt administration set a 90% tax rate for the top income bracket during WWII. Ukraine has a flat personal income tax with a rate set at 18%…If the government cannot make these taxes progressive, it can introduce a progressive ‘war surcharge’ (for example, the surcharge would apply only to income or capital above a certain threshold) that may be easier to accept politically and could be rolled back after the war.

Countries’ ability to tax their economies effectively has traditionally been crucial to their ability to win wars. Ukraine is no exception. The war has generated a huge amount of national solidarity — now, that solidarity needs to be channeled into government revenue. If Ukraine raises taxes substantially, it will go a long way toward keeping inflation under control.

A bright future ahead

I therefore do not share the pessimism of Tooze and Ferguson regarding Ukraine’s immediate economic situation. Yes, it’s good to be properly alarmed in order to avert problems before they become insoluble. But at the same time, it doesn’t seem accurate to depict Ukraine’s economy as being on the brink of collapse. Economic activity is stabilizing, exports are rising again, foreign aid is pouring in, food isn’t a problem, fuel is being imported in sufficient quantities, inflation is high but still manageable, the hryvnia peg is holding for now, and the military situation appears to be improving. Ukraine needs to raise taxes, but if they make that one policy change, they should probably hold on OK.

And after the Russians are fully ejected from the country, Ukraine has a bright future ahead. Its grain exports will recover, its defense industry will be supercharged by the war and will transition to peacetime manufacturing, and it appears to be joining the greater East European information technology cluster. Foreign countries will likely forgive their wartime loans and provide reconstruction aid — already, countries are lining up to promise support. The EU will probably offer single market access for Ukraine, which helped supercharge the economies of Poland and Romania in earlier decades. And Ukraine’s oligarchs seem to be declining rapidly in power and wealth— a sign that the country won’t return to the corrupt, dysfunctional economy of the 1990s and 2000s.

In the long term, I am very bullish on Ukraine.

“And after the Russians are fully ejected from the country”

Herein lies the problem. If your argument is predicated on this assumption, well, it becomes a lot harder to imagine a prosperous Ukraine. Even the most optimistic forecasts rarely imagine a total Russian ejection from the country (and are we including Crimea here?).

Noah, are you really advocating for a tax increase in a country with a 37% GDP decline, 25% inflation, a war that has removed 9 million people from the country, and forced millions of others into internal refugees? As well as a 20% UAH devaluation?

You make statements like Ukraine "has a pretty robust welfare state" -- but compared to what? The UAH-denominated welfare payments are right now substantially all late. And with inflation and the UAH devaluation, there is not much left.

Moreover, you talk about "solidarity", but most entrepreneurs have (rightly) seen the government as being predatory in terms of taxation in the past, without offering any real social benefits or returns. There is a real reason that people prefer not to declare their true incomes: it's a sure route to expropriation by corrupt tax officials, corrupt fire officials, police, customs officials, rival oligarchs and pretty much everyone. Surely you are familiar with the problems of bribery in Ukraine.

Ukraine does have a lot of potential. But this is going to be a very rough winter for the average population still within its borders, as well as those outside.

There are very few scenarios where higher taxes are going to be achievable, even if laws are passed.

In contrast, the west should be doing a lot more with real support, paid out rapidly, not announced and then debated upon for months.