Against "polycrisis"

We have lots of problems, but they're not mutually self-reinforcing

“Hypodermics on the shore/ China’s under martial law/ Rock & roller cola wars/ I can’t take it anymore” — Billy Joel

One term I see used increasingly often in the econ opinion-sphere is “polycrisis”. This term was invented by some French folks in decades past, but it has recently been popularized by Adam Tooze. Tooze, a historian at Columbia and a popular blogger, is also the author of some of my favorite history books, including The Deluge (about WW1), Wages of Destruction (about WW2), and Crashed. The latter is the best history of the early 2010s Euro crisis that I’ve ever read (or am ever likely to read), and it does a great job of explaining how problems in various different countries exacerbated each other.

So perhaps it’s not surprising that Tooze sees the world of the 2020s as a system of even larger interrelated crises. In a recent blog post, he pulls a definition of “polycrisis” from a report by the Cascade Institute:

We define a global polycrisis as any combination of three or more interacting systemic risks with the potential to cause a cascading, runaway failure of Earth’s natural and social systems that irreversibly and catastrophically degrades humanity’s prospects…A global polycrisis, should it occur, will inherit the four core properties of systemic risks—extreme complexity, high nonlinearity, transboundary causality, and deep uncertainty—while also exhibiting causal synchronization among risks.

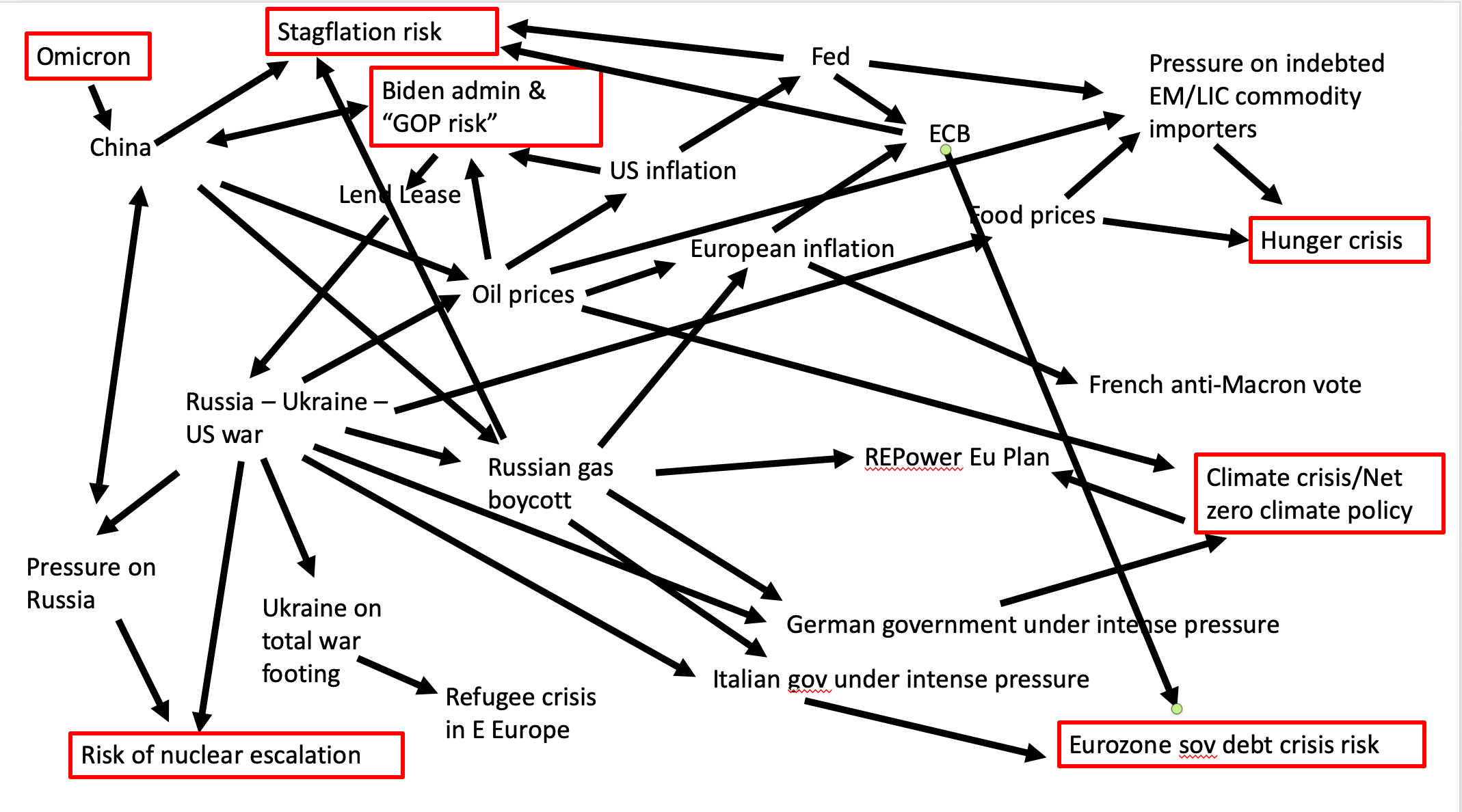

This basically seems like a way of saying that all the bad things you read about in the news — inflation, climate change, war, political turmoil in the U.S., economic turmoil in China — are all of a piece, with the individual crises reverberating back and forth and causing a general system failure. In an earlier post, Tooze attempted to draw a picture of this system of interrelated crises and risks:

I generally enjoy big-think like this. (If I didn’t, I would be somewhat of a hypocrite, given that my recent post about decoupling was entitled “The end of the system of the world”!) But I’m just not sure if the challenges and risks the world faces today are as mutually reinforcing as Tooze and the other “polycrisis” enthusiasts believe.

The polycrisis illusion

For one thing, it’s always very easy to think that we live in an era uniquely chock-full of risks, disasters, and problems. This is because of something called the availability heuristic — we tend to think the things we read about are typical of the world at large. And both the news media and the social media shouters who crave our eyeballs have long ago realized that “no news is good news” — i.e., negative news is uniquely good at grabbing our attention. So the more we’re engaged with current events, the more we’re likely to see the world as defined by things that alarm us — this is the subject of the song “We Didn’t Start the Fire”, quoted at the top of this post.

This is not to say the world is free of crises and risks; there are plenty out there. Nor is it to say that our current era has less than others; this is very hard to judge. But the idea that these crises are all related may be a case of apophenia — our natural human tendency to perceive connections that don’t actually exist, or are far weaker than we think.

Just because we can draw arrows between news items does not mean that the items are strongly coupled. For example, Tooze’s diagram draws an arrow from China to the Russian gas boycott, but China didn’t join the boycott. He draws an arrow between “Biden administration & GOP risk” and the Lend-Lease bill, but there’s no reason to think Lend-Lease was motivated by U.S. domestic politics, and the support for Ukraine has so far remained bipartisan. He draws an arrow from oil prices to the climate crisis, but — as I’ll talk about in a bit — the former actually helps address the latter.

When crises aren’t really strongly coupled, they can act as low-correlation assets in a diversified financial portfolio — when one problem is getting worse, another problem somewhere else is likely to be getting better.

In fact, though, I think there’s an even more important reason to be skeptical of “polycrisis”: buffer mechanisms. The global economy and political system are full of mechanisms that push back against shocks. Supply-and-demand is a great example — when supply falls, elastic demand cushions the short-term impact on prices (this is a little like Lenz’s Law in physics). Political backlashes are another mechanism — people don’t like it when you try to deny elections or invade your neighbors, and they get mad and push back. Policy responses are a third buffer — when central banks see inflation, they restrain it with higher interest rates. And so on.

The reason this makes a polycrisis less likely is that the buffer mechanisms often push back against problems in addition to the ones they were designed to push back against. There are plenty of historical examples of this. The New Deal didn’t just fight the Depression; it finally implemented a long-needed social insurance system that has served us well to this day. The victory over the Axis in WW2 also prompted decolonization and the creation of a global economic system that has allowed most of the world to flourish in the century since. More recently, the 2008 financial crisis led to needed infrastructure spending, Obamacare, and the intellectual revival of industrial policy.

In other words, sometimes instead of a polycrisis we get a polysolution.

Today, I can see a number of examples where the various crises that newsreaders worry about are leading to responses that will help address the others.

Buffer mechanisms in the global political economy of the 2020s

As I mentioned before, one very simple example of a buffer mechanism is supply and demand. In the past year, China’s economy has slowed dramatically due to a combination of a real estate bust, the Zero Covid policy, and various regulatory crackdowns. Normally, a recession in the world’s biggest trading nation would be a cause for global alarm, but in this one it’s more likely a source of relief. A collapse in Chinese demand is helping to restrain oil prices, keeping them at around the same level as the early 2010s:

That in turn is blunting the impact of the Ukraine war and Russia sanctions on Europe’s economy (and America’s, and Japan’s, etc.).

A combination of China’s economic slowdown and Russia’s military fiasco in Ukraine also seem to have reduced the chance of U.S.-China conflict, at least in the short term. Seeing Russia fail to conquer a smaller country must have given even Xi Jinping pause about launching a similar military adventure to conquer Taiwan, while economic struggles distract policymakers’ attention.

Though it’s too early to tell, the results of last week’s midterm elections in the U.S. — which were a victory for stability and bipartisanship and a loss for election-denialists — might also have been prompted in some minor way by the Ukraine war and the threat of geopolitical competition with China, which should remind Americans that there are enemies in the world more dangerous than other Americans.

Meanwhile, the war in Ukraine will spur the fight against climate change. Disruptions to Russian energy supplies, especially in Europe, create incentives for the rapid deployment of renewable energy. This is from May:

The Commission proposed that 45% of the EU’s energy mix should come from renewables by 2030, an advance on the current 40% target suggested less than a year ago. Officials also want to cut energy consumption by 13% by 2030…

“It is clear we need to put an end to this dependence and a lot faster before we had foreseen before this war,” said Frans Timmermans, the EU official in charge of the green deal.

Just a few days ago, the European Commission followed through with a temporary emergency regulation to speed the adoption of renewables. (The war is leading to minor outbreak of sanity on energy in general; Germany is keeping its nuclear plants open, at least for a while.)

The rapid adoption of renewables will, in turn, drive down their price, through a mechanism known as learning curves — the more you build, the more cost goes down, creating an incentive to build even more. So the increased adoption of renewables in Europe and other Russia-sanctioning countries in response to the Ukraine war will also make renewables more attractive in China, India, and other countries that aren’t joining in the sanctions.

All this will help the fight against climate change. But it will also help address another longstanding economic problem in the rich world: slow growth. Due to massive continuing cost drops, renewable energy increasingly isn’t just green energy — it’s cheap energy. The forecasters who study learning curves believe that technologies like solar, batteries, and hydrogen are much more susceptible to learning effects than fossil fuel technologies or even nuclear. That means that renewables are going to give us cheaper energy than we’ve ever had in our history as a species. And that in turn will help the developed world shake off the creeping stagnation in productivity and wages that it has endured for most of the time since the oil shocks of the 70s. Cheap energy is highly complementary to human labor — armed with cheap energy, we can rebuild much of our world.

This is not to say that there are no cases in the world where one problem is exacerbating another. Higher interest rates, for example, are sure to cause capital flight and currency depreciation in some developing countries, making it harder for them to buy food and energy. But the global free-market system built in the last three decades is looking more resilient than many expected; most developing countries are doing OK.

Dark Brandon vs. polycrisis

In other words, I look out in the world and I don’t see a polycrisis; I see an emerging polysolution. The looming threats of climate change and authoritarian revanchism, combined with the shocks of Covid and inflation, have stirred both policymakers and businesses to action. And many of those actions will end up addressing multiple crises rather than just one. Nor am I alone in my feeling that the narrative of the world suddenly seems to be improving:

I want to venture out on a limb here and say that this is not a coincidence. A lot of the buffer mechanisms I described above are political in nature, and they share the basic description of “human beings coming together in a crisis to address their collective problems”. During good times, human beings tend to seem irresolute and divided as pursue our individual goals and fight over the pie. External shocks can bring the entire system crashing down, but they can also spur humans to get serious and start working together.

This is not to say that “hard times make strong men”, as the popular meme goes. It’s that we were “strong men” (and women, and nonbinary persons, etc.) all along, and we just didn’t have a reason to buckle down and get serious about solving society’s problems. You know how in the fantasy stories, the Hero of Legend always mysteriously appears just in time to fight the Great Evil? It’s not luck, it’s selection bias. If the Hero of Legend appeared in normal times and there was no Great Evil around, they would just end up playing in a grunge band or coding a mobile app.

On Twitter, we jokingly refer to humanity’s attempts to fight back against our collective problems as “Dark Brandon”. But we don’t really think that our aged President is manipulating the world behind the scenes to fight climate change, authoritarianism, etc. It’s a metaphor for the polysolution — for the aggregate efforts of our collective efforts to fight back. The world is not a fragile over-engineered machine just waiting for a shock to tip it into collapse. It’s something we are constantly working to rebuild. Sometimes we have to work harder than other times.

I've never had an opportunity to comment on an optimistic blog post before.

. . . .

I don't know how to do it.

“You know how in the fantasy stories, the Hero of Legend always mysteriously appears just in time to fight the Great Evil? It’s not luck, it’s selection bias. If the Hero of Legend appeared in normal times and there was no Great Evil around, they would just end up playing in a grunge band or coding a mobile app.“

This is a wonderfully silly analogy.