Your local price changes aren't inflation

Why do some people in the Bay Area think inflation is high when it's not?

There’s an old theory in macroeconomics called the Lucas Islands Model. In this model, each businessperson lives on their own little island, and the only thing each one knows is how much cash people are willing to pay for their goods. When people suddenly start shelling out more cash for their goods, the businesspeople assume that some of this is due to an increase in how much consumers want the stuff they sell, so they increase production and hire more workers. But if instead it’s due to an increase in the money supply — basically, the central bank just handing out dollars, so everyone has more dollars to spend — then the businesspeople get tricked into producing more, even though people don’t actually value their stuff any more than yesterday. Thus, the Lucas Islands Model is a theory of how monetary policy can boost the real economy.

The Lucas Islands Model isn’t a very good model of the economy. Theoretically, it’s more than a little bit suspect — why wouldn’t businesspeople just look at the inflation rate instead of letting themselves be tricked into thinking their products are suddenly more popular? Even before the internet, it was easy to know what the inflation rate was — just read the Wall Street Journal or watch the news. Empirically, the model also didn’t do too well — it led to the conclusion that GDP would swing around pretty wildly from quarter to quarter, which in reality it doesn’t. Good try, Lucas, but not quite.

But I keep thinking of the Lucas Islands Model every time I see my friends in the tech world wonder if inflation is actually a lot higher than the government statistics indicate. Tech folks are generally not hard-money/austerity types, so it’s unlikely that they just want to believe in made-up inflation measures like the Chapwood Index (if you want to know why that’s made up, I wrote a Bloomberg post about it). So why do so many tech people seem to suspect that inflation is more of a problem than the government numbers make it out to be?

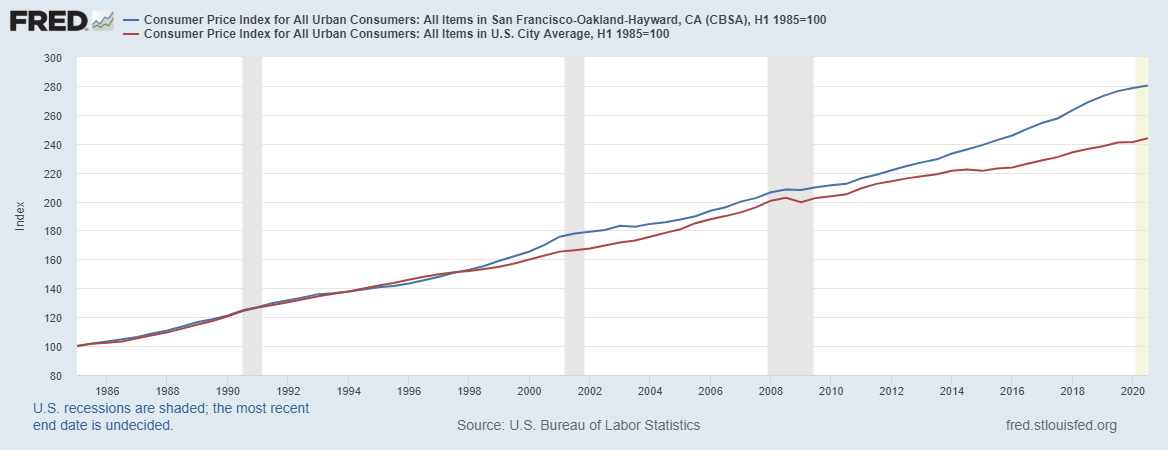

My theory: They’re living on a Lucas Island! Basically, a bunch of high-earning people moved to the Bay Area and pushed up the price of land and other things. And that makes it look like the cost of living is rising fast. But in fact, this is pretty unique to the Bay. Consumer prices in the San Francisco metropolitan area, for example, have outpaced the nation as a whole, especially since around 2014:

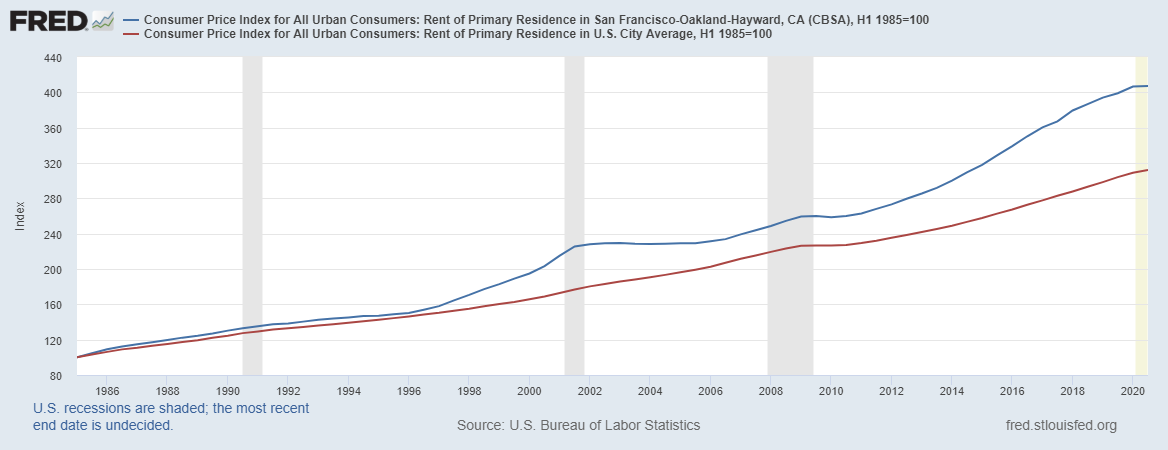

And rents even more so:

This divergence has happened because of an increase in people’s desire to live in the Bay Area. That means people living in the Bay Area tend to see prices rising faster than people see in other areas. And subconsciously, that probably makes them wonder if the government inflation statistics are wrong — just like someone on one of the islands in the Lucas Islands Model!

(Actually, my friend Adam Nash also suggested another reason: When stock prices go up, tech employee compensation goes up too. So people may also be mistaking rises in asset prices for wage inflation — another Lucas Islands effect! A third possibility is that tech folks are simply being optimistic about the future of their Bitcoin portfolios, since they view Bitcoin as an inflation hedge.)

Anyway, you might say that local price changes matter, and asset price changes matter, so doesn’t that mean there’s actually hidden inflation? Well, no. It’s not that local price changes don’t matter — they absolutely do. And it’s not that asset price changes don’t matter — they absolutely do. It’s just that those concepts aren’t what economists are trying to get at when they measure inflation.

So let’s talk about why economists define inflation the way they do.

Inflation explainer

Economists think about “prices” in several different ways. Suppose you’re buying a TV. First, there’s the number of dollars (or Bitcoins, or yen, or whatever) that you use to buy the TV. That’s called the “nominal” price. Then there’s the amount of some other useful thing — food, or shelter, or your own leisure time — that you give up in order to obtain the TV. That’s called a “relative” price. Economists tend to think that only relative prices are “real” — dollars are just little green pieces of paper (or metaphorical little green pieces of paper, at this point), while actually giving up other stuff to get a TV is a real cost.

So imagine the nominal price of everything in the economy doubled, including wages. TVs that cost $500 now cost $1000, people who earned $50,000 now earn $100,000, etc. The relative prices would all be the same; you’d still have to forgo the same number of pizzas, or work the same number of hours, in order to get a TV. Economists typically think that this kind of change isn’t really important in economic terms; our material standard of living is exactly the same, we just assigned different numbers to things.

This kind of change is what the concept of “inflation” tries to get at. We tend to colloquially think of “inflation” as meaning “an increase in the real cost of living”, but to economists it really means something more like “fiddling with the unit of account”. The economists who created the term were probably thinking about intentionally inflationary monetary policy, where the government basically spams money into the economy in an attempt to make currency less valuable, often as a way of reducing the real burden of debts.

In the idealized, econ-textbook concept of inflation, it doesn’t reduce standards of living, because wages rise in tandem with everything else. In reality, it doesn’t always work out that way. In the late 1960s, compensation kept up with the reasonably high (4-5%) inflation at the time, but in the 1970s it failed to do so.

So even though economists intended for inflation to mean “the numbers change but nothing else changes”, in reality a burst of unexpected inflation probably can increase the real cost of living, possibly because workers aren’t able to bargain effectively for raises to keep up with inflation when inflation levels are high and erratic.

(Side note: This raises the interesting question of whether wages should be included in official measures of inflation. The typical and official answer is “no”, because labor is an intermediate good — including its price in inflation would be like including the price of the glass used to make the TV screen, which has already been rolled into the price of the TV itself, so that would be double-counting. But there’s an argument that leisure is a consumption good that isn’t counted in the “market basket”, and that wages are the price of leisure. Anyway, let’s skip this question for now.)

Official inflation numbers don’t do a perfect job of measuring what economists want them to measure, but you can pretty easily see why local prices aren’t included in the measure. If people decide they don’t want to live in Detroit and would rather live in San Francisco, then yeah, prices in San Francisco are gonna go up. That doesn’t mean the U.S. dollar is worth any less than it used to be. Which means if you think the Fed is spamming dollars into the U.S. economy and driving down the value of the dollar, you probably shouldn’t just look at prices in the Bay Area. You should look at prices everywhere that things are priced in U.S. dollars.

(Side note: Because of the way monetary policy works, the Fed spamming dollars into the economy doesn’t always devalue the dollar. One reason is that banks also have some control over the money supply; they can destroy dollars as fast as the Fed creates them. Another reason is that people can spend their dollars more slowly. This is basically similar to the principle that creating more of something doesn’t decrease its value if people just hoard it more.)

Now we get to the common question of whether asset prices — stocks, houses, etc. — should be included in inflation numbers. The answer is “no”. For stocks, the reason is double-counting — when the price of TVs goes up, the earnings of the companies that sell the good also go up, which makes stock prices go up. So to count both the stock price and the price of the TV in inflation would be double-counting.

More fundamentally, stocks don’t actually represent a valuable good in and of themselves; remember that economists’ main reason for measuring inflation is to separate the value of the dollar from the value of valuable goods. Stocks have no inherent value, so including them in inflation wouldn’t help separate the value of stuff from the value of money.

But how about houses? Houses are real valuable stuff, they aren’t just a financial accounting tool like stocks. In fact, economists do try to include the price of the real value of owner-occupied housing in measures of inflation. They do this by calculating “owners’ equivalent rent”. Basically they look at your house, they try to estimate how much you’d have to pay to rent that house on the market, and they count that amount in the inflation numbers. In other words, they pretend that owner-occupiers are renting their houses from themselves.

So that means that when house prices go up, it usually does feed into inflation, since rents go up as well. But in situations where house prices go up a lot more than rents — as in the housing bubble — then only the rents get counted in inflation. Because the “extra” house price increase is more of a financial asset price than the price of a real good; when people pay more for a house because they’re speculating it’ll go up in price even more in the future, it doesn’t increase the real value of living in that house. As we discovered to our woe in 2007-2008.

So anyway, that’s how inflation works. It’s not a perfect measure of the difference between dollar prices and the real value of goods, but that’s what economists are trying to use it to measure. There are lots of (very wonky) arguments about how it could be better. But local prices shouldn’t be included, nor should asset prices. Those are important things, but for other reasons.

(Update: Some people have also asked me about whether monetary policy changes relative prices — for example, if the Fed’s actions are making the Bay Area cheaper and Detroit cheaper, or raising the salaries of software engineers at the expense of the teacher salaries, etc. That’s a very interesting question, and I’ll cover it in another post! Stay tuned!)

The thing that people don't seem to understand when they talk about inflation is that price increases in

- homes

- healthcare

- education

- child care

are definitely real, they're just not due to *monetary* policy. They are due to other policies like not building any houses or reduced education subsidies/student loans. These are *relative* cost shifts in the economy over time, not general rises in the price level, but they have their own causes and must be addressed specifically. I think Noah has written about this

"A third possibility is that tech folks are simply being optimistic about the future of their Bitcoin portfolios, since they view Bitcoin as an inflation hedge."

Chapwood invocations are increasingly common among hard money people; I wouldn't discount the connection between crypto enthusiasm and an inclination to seek out any purported evidence of actual or impending inflation. There's a powerful temptation to want to be in on things, especially dark, secret, even (gasp!) _conspiratorial_, money things. A lot of present and past inflation prognosticating is just that: gnostic.