Yes, your house is wealth

In order to fix our dysfunctional housing politics, we must confront this economic fact.

Every so often I encounter the argument that owner-occupied housing isn’t a form of wealth. This would come as news to economists like Emmanuel Saez and Gabriel Zucman, who study wealth inequality for a living, and who definitely count owner-occupied home equity in their wealth numbers. It would also come as news to the U.S. Census Bureau, who finds that equity in owner-occupied housing represented the largest share of the wealth of households outside the top 1% as recently as 2015:

The definition of wealth here is just assets minus liabilities. An asset is anything you can sell for money. You can sell your house for money. Hence it is an asset. In fact, historically, it’s one of the assets with the best returns.

But I don’t want to make an argument from authority here. There are very good reasons we count owner-occupied housing as wealth, and they’re not too hard to understand.

To see why, first let’s make an analogy: a magic cupboard that gives you food.

The magic cupboard analogy

Suppose you had a magic cupboard that gave you three meals a day, free of charge. Furthermore, suppose there was a market for magic cupboards, and that you could sell your own for $1 million if you wanted to.

This magic cupboard represents a form of wealth. If you think it’s not, consider whether you would be poorer if your magic cupboard burned down or got stolen or stopped working. Yes, you would be poorer.

Some people might argue: “But you need food every day. If you sold your magic cupboard, you’d just have to use the money to buy food.” And indeed you would. You would have to go to the grocery store or go to restaurants, because you wouldn’t have a magic cupboard. You could use the cash from the sale of your magic cupboard to buy food at the store or at restaurants.

But now consider someone who doesn’t own a magic cupboard. They also have to eat every day. They have to go to the grocery store or go to restaurants. But unlike you if you sold your magic cupboard for cash, the person who didn’t start out with a magic cupboard has to work for the cash they need to buy food every day. Because they have to work for what you could just buy off of an asset sale, they’re poorer than you.

Thus, the magic cupboard is wealth.

The magic cupboard is pretty much a perfect analogy for an owner-occupied house. We are all born with a need for shelter every day, just as we are all born with a need for food every day. A house is just a magic cupboard that gives us free shelter every day.

Consider two people — Tom, who owns a house (and has no mortgage debt), and Jerry, who does not. Tom gets free shelter every day, while Jerry has to work to pay rent. (And assume they have no other assets or liabilities.) If Tom chooses, he can sell his house and get a bunch of cash, and use that cash to pay rent from then on, without having to work for his rent money. Jerry, on the other hand, has to work to get shelter every day.

Tom is definitely richer than Jerry in this example. His owner-occupied house makes him richer. Thus, it is a form of wealth.

“But you always need a place to live”

The people who push back on the idea that owner-occupied housing is wealth often argue that because you need somewhere to live, selling your house would just require you to buy a different house:

But this is wrong. You don’t have to own a house. 35% of American households pay rent!

When I suggest renting as an alternative to homeownership, people sometimes bristle. And I guess this makes sense because after all, homeownership is part of the American Dream — part of the basic package that’s supposed to be the birthright of the great American middle class. But the fact is, plenty of Americans don’t actually have that privilege — they don’t have the money to buy a house, so instead they have to work to pay rent. Whereas the homeowner, as I pointed out in the previous section, could just sell their house and use the proceeds to pay rent instead of having to work.

Just because you feel that your class and station should afford you a certain amount of wealth does not mean that it isn’t actually wealth.

Does owning a house make you long housing?

A similar but more subtle argument is that homeownership doesn’t give you a net long position in the housing market. MIT’s Erik Brynjolfsson makes this argument:

The idea here is that your natural need for shelter — your own frail mortality — is a form of housing liability that you’re born with. So if you’re a homeowner, you have zero net housing wealth, because your asset only cancels out your natural liability.

In fact, it is perfectly possible to think of your need for housing — and your need for food, etc. — as a liability that you’re born with. In fact, there are a lot of things we could count in wealth numbers that we typically don’t. For example, we could count human capital — the skills and knowledge that will allow you to earn more money in the future — as a form of wealth. We could count future government benefits as a form of wealth. We could count a genetic tendency toward heart disease as a liability. We could count your need for companionship, your need for respect, or your need for self-fulfillment as a liability. Etc. etc. We don’t count any of these things in our official wealth numbers, but we could if we wanted to.

But even if we did count your need for shelter as a liability, Erik’s argument isn’t quite right, for two reasons.

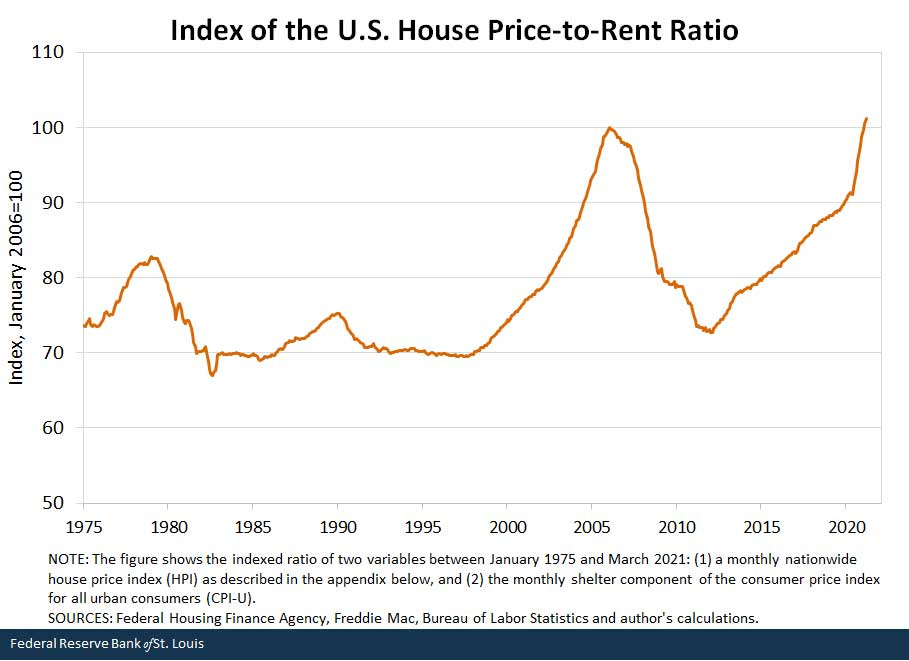

First of all, the housing market is not the same as the rental market. In fact, these can diverge pretty strongly. Here’s a graph of price-to-rent ratios in the U.S. as a whole:

As you can see, sometimes house prices really outpace rent a lot!

Your need for shelter does not require you to own a home. You can get shelter by renting. So if home prices go up and rents don’t go up — as they did in the bubble of the 2000s and have done again recently — homeowners gain. Thus, they are long the housing market.

The second reason Erik isn’t quite right is that people’s inherent biological need for shelter is pretty meager. Some people live in bunk beds in dorms. In Japan, some people live in one-room apartments with only 50 square feet (4.6 square meters) of floor space. Pretty much American homeowner owns massively more house than that — the median floor space per person is 700 square feet, and the median size of a newly constructed home is 2,386 square feet.

Thus, even if we did decide to start counting people’s biological need for shelter as a liability, it would be much smaller than the amount of housing assets that American homeowners own. And thus, they would still be long housing.

Wealth vs. liquidity

Another reason people think housing isn’t wealth is that it isn’t very liquid. Liquidity means how easy it is to sell something for cash. You can sell your house and go rent if you like, or downsize to a smaller place to get some cash, but it’ll cost you some time and quite a bit of money to do so. In the U.S., real estate transactions have traditionally been 5-6% of the purchase price, and there are various closing costs as well.

These fees are absurd — U.S. real estate commissions have come down somewhat, but they’re still much higher than in most other countries. In fact, they’re just another of those things that Americans pay too much for, like health care, infrastructure, and housing itself. But they represent a real reason why housing wealth is less liquid than, say, stocks or bonds.

Another reason housing wealth is illiquid is that you can’t sell just a bit of it — you either have to sell the whole house or none of it. This is different than stocks or bonds, where you can sell just a little if you just need a little cash. This makes housing wealth less useful than stocks and bonds — trading it for cash is an all-or-nothing proposition. When people say “house rich, cash poor”, this is what they’re referring to.

Now, I should mention that this is starting to change. New businesses are finding ways to let people sell a piece of the equity in their home. Essentially, they get a bit of cash, and an investor gets to own a share in the equity of their house — much like a share of stock. When this becomes widespread, owner-occupied homes will become a much more liquid asset. This will probably push home prices up, because liquidity is valuable.

In any case, the point of this section is that liquidity and wealth are two different things. Not all dollars of wealth are equally useful. But even illiquid wealth is still wealth.

Basing our wealth on housing is dysfunctional

Hopefully this ends the debate about whether owner-occupied housing is a form of wealth. Having said that, however, I think it’s worth saying that basing the wealth of our middle class on owner-occupied housing is a system with a huge number of drawbacks.

In the U.S., rich people have most of their wealth in stocks and bonds, while the middle class has most of its wealth in (mostly owner-occupied) housing:

What this means is that in order to increase their own wealth, the vast majority of Americans have to make sure their home values go up and up and up. This applies to young Americans who stand to inherit their parents’ homes, as well.

The easiest way to pump up your house’s price is by using control of local politics to keep poor people out of the neighborhood and to artificially limit housing supply. Local NIMBYism has basically become America’s national pastime, and it has resulted in a housing shortage in many of the most desirable locations. And so we have Milpitas School District in California begging local residents to rent out their spare rooms to teachers.

In order to fix this problem, we’re going to have to recognize that housing is a real form of wealth, and the inequality of home equity ownership is a real form of wealth inequality. It’s understandable that middle-class Americans might want to deny that their houses are a form of wealth — it’s always nicer to think that your assets are simply your basic due, rather than a form of privilege that many people don’t enjoy. But in order to fix our country’s dysfunctional housing politics, we have to confront the fact that owner-occupied housing is a form of wealth.

This gets weirder in the context of regions with rapid cost increases. Are you five times wealthier than a decade ago, when nothing about your material lifestyle or ability to consume has actually changed? Is renting actually an option when rents are spiraling towards infinity and your wages are not? Is the occupant of a high-rise 2BR on Chicago's Gold Coast really such a pauper relative to the occupant of a studio in San Francisco's Mid-Market?

I think we'd have to say that "choosing not to move away" is a luxury that becomes increasingly lavish each year. You have to admit that is pretty unlike what a normal person is thinking about when they think about being wealthy. Perhaps it is the popular conception of wealth that's wrong, though.

This is a good article, but it's missing a second part of "What do we do about this to ensure that housing becomes (somewhat) more affordable". Anyone who's bought a house should know that it's 100% an asset (a form of wealth). My question is: how can we build more housing without having people believe that their biggest asset is going to crash in value? Because ultimately YIMBYism will have to win in the political arena and that means winning arguments.