Yes, we're probably in a recession, and that's fine

Economic fluctuations aren't always catastrophic

The Bureau of Economic Analysis has released its advanced estimates for growth in the second quarter of 2022, and the numbers show that the U.S. economy shrank for the second quarter in a row. In

Here, via Furman, is a picture that I think tells the story quite well:

GDP bounced back very strongly from the pandemic, and had just about reached the upward trend it was on before Covid struck. Now, in 2022, it’s weakening again by a small amount.

All these numbers are just advance estimates, of course, and revisions are often substantial. Some people suspect that we’ll eventually find that GDP didn’t even fall in the first quarter at all! But it seems clear that economic activity is slowing a bit in recent months. That’s all we really know so far.

Of course the big debate in the media will be over whether we’re now in a recession. The reason people argue over this isn’t really economics; it’s politics. “Recession” is a scary word, especially for those who remember 2008-12 — It conjures up images of unemployment insurance lines and dejected hopeless workers sitting around at home reading the classified ads. Because recessions are thought to equal political death for the governing party, supporters of that party tend not to want to admit that we’re currently in one, while opponents of that party tend to yell that we are in one. In this case, that means Biden supporters will mostly be trying to avoid the use of the r-word, while Republicans will be using it a lot.

But in my opinion this debate is a bit unnecessary. “Recession” wasn’t always a dirty word, and recessions aren’t always such bad things. Let me see if I can help demystify the idea a bit.

Three definitions of “recession”

There are basically three notions of “recession” — I call them the official definition, the folk definition, and the academic definition.

1. The official definition

The official definition of a recession is not based on hard-and-fast rules. Recessions are determined not by the U.S. government, but by The National Bureau of Economic Research, a nonprofit made up of (mostly academic) economists. The NBER has a group of macroeconomists called the Business Cycle Dating Committee, who decide when we’re in a recession. So the official definition is just “whenever these folks decide”.

So how do they decide? A recession, the NBER folks say, is “the period between a peak of economic activity and its subsequent trough, or lowest point.” But this isn’t a precise mathematical definition, for two reasons.

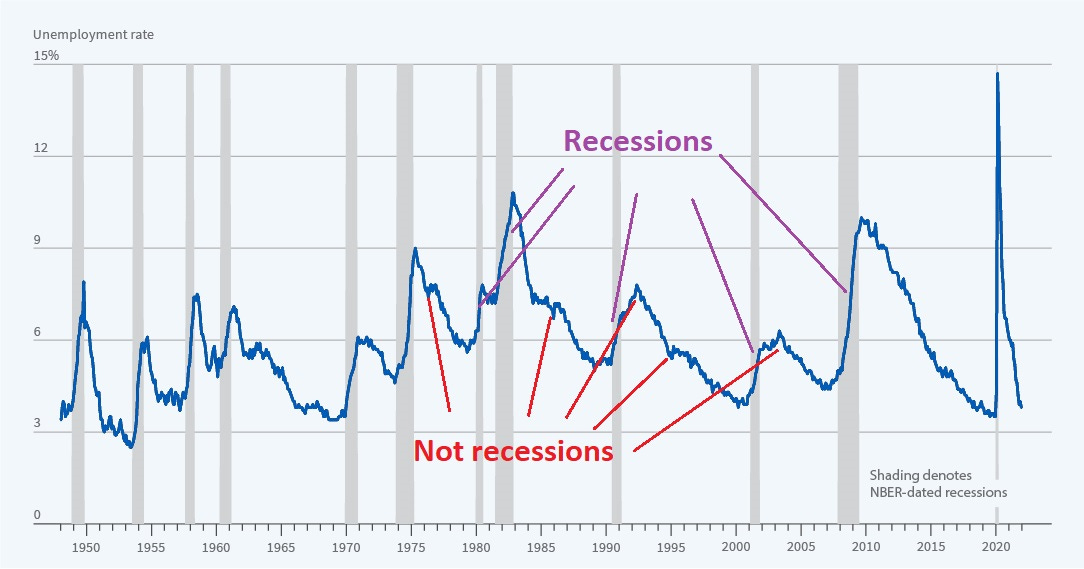

First of all, how big of a peak and trough are we talking about? Economic numbers bounce up and down constantly. Is each little monthly down-tick followed by a monthly up-tick a “recession”? No. The economists only care about big peaks and troughs. But how big is big? They just kind of eyeball it and decide. For example, here’s unemployment (note that a peak of unemployment is actually a “trough” of economic activity, since unemployment is bad):

As you can see, small increases in unemployment don’t get called recessions; big increases do. Just how big is up to the NBER people’s discretion.

The second thing that’s up to the NBER people’s discretion is which kind of economic activity to look at. On their FAQ page they state:

The NBER's traditional definition of a recession is that it is a significant decline in economic activity that is spread across the economy and that lasts more than a few months.

Basically the committee looks at a number of indicators — GDP, unemployment, and so on — and look at a bunch of different areas of the country, and decide if economic activity is going down.

That’s really all a recession technically is. It’s just a few economists sitting around and looking at data and saying well, we think the economy is sort of going down right now. And by this official definition, we won’t even know for a while whether we were in a recession in July 2022.

2. The folk definition

The folk definition of a recession, which is the one you hear the most often, is “two consecutive quarters of negative real GDP growth”. This idea originally came from an economist named Julius Shiskind in 1974. Shiskind, who was the head of the Bureau of Labor Statistics at the time, was trying to give the public a rule of thumb to tell whether we’re in a recession or not.

That rule of thumb gets cited a lot in the media, but also by various government and intergovernmental organizations — the IMF, Eurostat, the UK treasury, the Bank of India, and so on. So it’s a popular rule of thumb. But it doesn’t always match up with the official definition. In 1947, the economy contracted for two quarters and it wasn’t counted as a recession:

This is a weird case where the official definition of something is fuzzier and more judgment-based than the folk definition!

By the folk definition, we’re probably in a recession right now, subject to data revisions.

3. The academic definition

There’s one more notion of a recession, which is the one that academic macroeconomists think about. This is the one I like the best, but it’s also the hardest to understand.

Macroeconomists generally think about the economy as having a slow-moving “growth trend” and short-term, fast-moving “fluctuations” around that trend. The trend is supposed to represent deep fundamental forces like changes in technology and trade and regulation and population growth, while the fluctuations are supposed to represent transitory “shocks” like financial panics, oil price shocks, or waves of general optimism and pessimism.

That makes sense, but in practice it’s hard to separate the trend from the fluctuations. Economists argue about this a lot, and there are various mathematical notions of how to measure the trend. Here’s a picture of one of those methods, called a Hodrick-Prescott Filter:

(Note: This method isn’t considered a very good one, but it’s very well-known, so I’m just using it for illustration purposes.)

You can think of “recessions” as the parts where the blue line — the actual economy — is below the green trend, and “booms” as the parts where the blue line is above trend. In fact, this is how macroeconomists generally colloquially speak. They think of a slow economy not as one that’s decreasing in size, but one that’s below trend.

(Note: I’m playing a bit fast and loose with terminology here. Academics colloquially tend to use the word “recession” to refer to when the line is below trend, but this is not an official definition of any kind. Many macroeconomists make fun of the NBER’s recession-dating procedures.)

By this measure, recessions last a lot longer than by either the official definition or the folk definition. The official and folk definitions say that the Great Recession ended in 2009, but it took until the mid-2010s for unemployment to come back down to pre-recession levels. Most people probably didn’t think the economy was in such great shape in 2010, even though officially we were in “recovery”. That’s why I prefer the academic notion of a recession to the official and folk ones.

By this academic definition, we’re almost certainly in a recession now, since growth has probably dipped a little bit below the trend.

Recessions aren’t always so bad

But no matter which definition of recession you use, recessions don’t have to be a catastrophic thing for the welfare of the nation. In fact, they don’t always have to lead to political losses for the party in power.

First of all, size matters a lot. Big downturns like the Great Recession that began in 2008 are obviously economic catastrophes. Medium-sized ones, like the early 90s downturn or the Volcker Recessions of the early 80s, are also quite painful. But there are also plenty of recessions that the nation shrugged off. For example, in the twelve years from 1949 through 1961, we had no fewer than four recessions:

As you can see, real GDP did indeed shrink in each of these episodes. And unemployment did rise in each case, usually by about three percentage points

But the 1950s are remembered as a golden time for the U.S. economy. Unemployment bounced around, but it was generally low, and the spikes lasted only about two years each — laid-off workers knew that they would soon find work again. And though growth fluctuated, income growth overall was robust:

Dwight D. Eisenhower won reelection handily in 1956 despite a recession in his first term.

Nor are relatively harmless recessions purely a thing of the past. In 2001 we had a recession that raised unemployment by less than 2 percentage points:

Unlike the recessions of the 50s, this bump in unemployment took several years to return to some approximation of pre-recession levels (9/11 might have played a role there). But because the recession had been so mild in the first place, there were not many people whose lives were seriously impacted by the downturn of the early 2000s. You just don’t hear people talk about that time as a tough time in America. And like Eisenhower in 1956, George W. Bush won reelection in 2004 despite a recession in his first term.

The fact is, macroeconomies are volatile things. We can’t expect them to stick exactly to a smooth upward trend forever. Sometimes they’ll take a dip. The job of policymakers is to make sure those inevitable dips are as small and short-lived as possible.

And the American people seem to understand this — they’re pretty forgiving of small dips in economic activity, and only really get up in arms when things get severe.

The big danger is still inflation

It’s understandable that Biden defenders are trying to tamp down talk of “recession”. But as I see it, they should be much more worried about ongoing inflation.

The quarterly GDP numbers include both nominal GDP (the total number of dollars of economic activity) and real GDP (which is adjusted for changes in prices). By looking at the difference between these, you can see that inflation is still going strong:

These aren’t the official consumer price inflation numbers, but they suggest that the problem is persistent.

Ongoing high inflation represents a greater danger than a mild recession, both in terms of general economic welfare and in terms of political danger to the Biden administration. People tend to forgive mild recessions, but they get really, really up in arms about high inflation. And they are up in arms about inflation right now.

The mild recession that we are probably in right now is being caused by the Federal Reserve’s attempts to tame high inflation. The Fed has hiked interest rates from near 0 to 2.5% and has made it clear that more big hikes will follow if inflation doesn’t fall. This and other Fed actions have curbed aggregate demand, by discouraging investment. That’s why housing investment has cratered, and why business investment is inching down. And the reduction in investment is why we’re in recession.

Now, consumption is still rising slowly. And there’s no sign of a rise in unemployment at all yet. And with disinflationary pressures mounting from the supply side, there’s a decent chance that the Fed will only end up having to induce a mild recession in order to tame inflation.

So Biden supporters shouldn’t be terrified of the r-word. If general knowledge of a “recession” helps stop businesses from continuing to raise their prices, that will be a healthy thing — both for the economy and for Democrats’ chances of keeping Donald Trump from returning to office in two and a half years.

Seems like a lot of people on Twitter think this is some sort of critical decision. I don't see how the NBER's classification should make any difference to 99% of people.

Would all the people bending over backwards and trying to avoid using the term "recession" for the last two negative quarters of GDP growth be doing this if Trump was still president?

No, definately not. This is exactly what is wrong with Journalists, academics and economists. Their political bias pollutes their opinions and articles depending who is in charge.