U.S. government debt is not a ticking time bomb

But a bit of austerity is probably inevitable.

\" by pingnews.com is marked with Public Domain Mark 1.0.")

Some folks asked me to write a post about whether the U.S. debt is a ticking time bomb. They were alarmed by this viral video of retired hedge fund manager Stanley Druckenmiller declaring that U.S. debt service costs are about to eat the rest of the budget:

Now, Druckenmiller is not a perennial prophet of doom and gloom, nor is he a perma-hawk who always warns that deficits and/or inflation are about to destroy the economy. He correctly warned of inflation as early as September 2020, but he does not appear to be one of the people who (wrongly) warned that quantitative easing would cause inflation back in the early 2010s. A lot of finance-industry macro guys will tell the crowd what they want to hear, but Druckenmiller seems like a straight shooter.

What’s more, some of his concerns are clearly appropriate. Higher interest rates will raise the amount of money that the U.S. government has to spend on debt service, and that will crowd out other types of government spending. And in the long run, we will probably have to either make cuts to entitlement benefits or find significant new sources of cost reduction, which can be a politically tricky thing to do.

Personally, though, I think things aren’t nearly as bad as Druckenmiller thinks. U.S. interest costs won’t rise catastrophically in the short term, and there’s not really a reason to expect interest rates to stay high for decades. Furthermore, inflation will itself erode some of the national debt, reducing long-term interest costs relative to GDP.

It does seem clear, though, that increased interest costs — and the Fed’s unwillingness to finance higher government borrowing — will force a bit of austerity in the years to come.

Interest costs are going up, but it’s not that bad yet

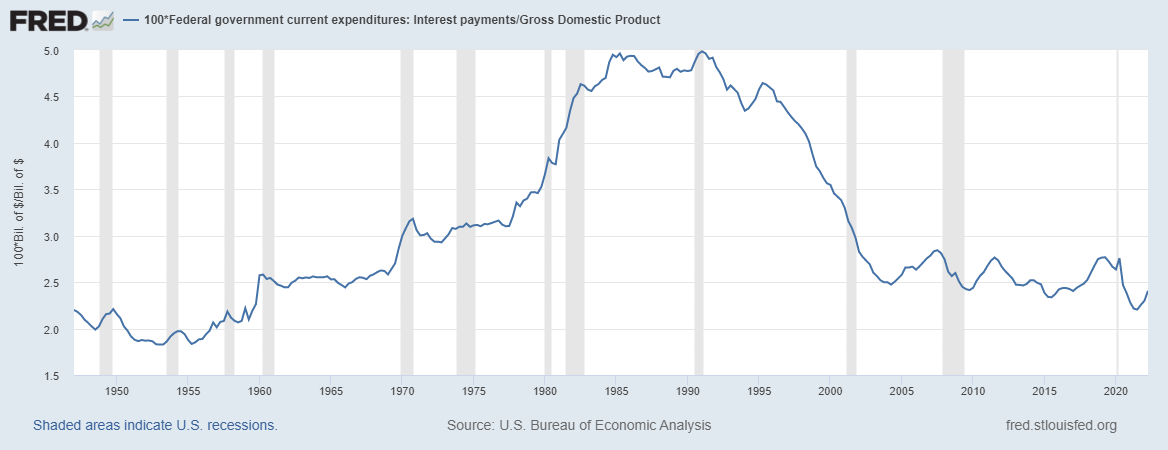

Here’s a long-term history of how much the federal government pays in interest payments, as a percent of GDP:

You can see that interest costs fell during and after the pandemic and have now started to rise again. But they’re a long way from being anywhere close to what they were in the 1980s, when they reached almost 5% of GDP.

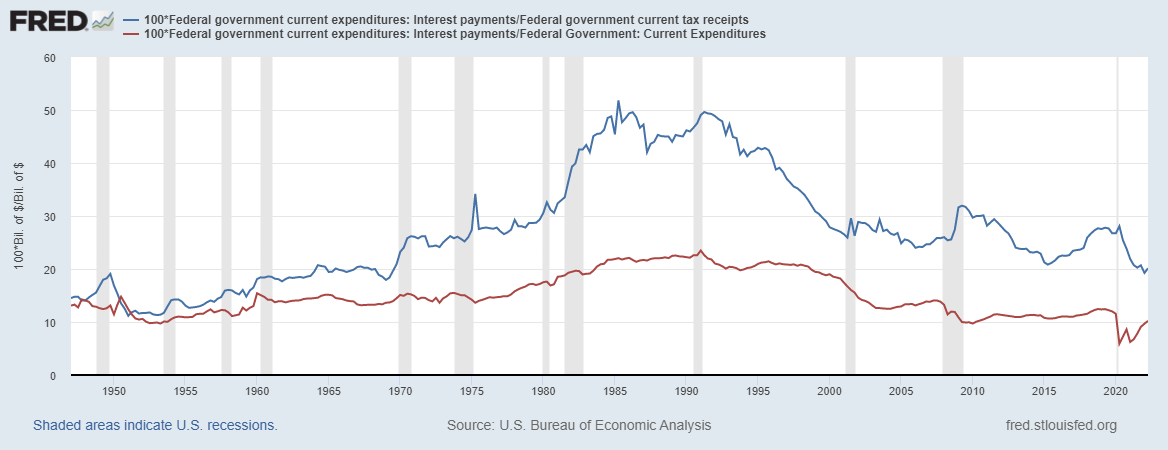

Now let’s look at interest payments as a percent of tax revenue and as a percent of government spending:

In the 80s, interest costs reached an astounding 50% of tax revenue! This is because we raised interest rates in the 80s while also cutting taxes. For better or for worse, Reagan was not a particularly fiscally responsible President.

Right now, interest payments haven’t even begun to rise as a percent of tax revenue, and one big reason is inflation. Interest rates are set in dollar amounts, and inflation increases the number of dollars in the economy, meaning that tax revenues increase in dollar terms as well. That makes it easier for the government to make its interest payments. Remember, inflation erodes debt of all kinds.

The problem: rolling over the debt

So right now, interest costs are fine. But if interest rates keep going up, then interest costs will rise. The reason is that the U.S. government has to roll over its debt as the bonds reach maturity. And as it rolls over debt, it will have to borrow at a higher interest rate.

Now, this doesn’t happen all in one fell swoop. Not all of our government debt has to be rolled over immediately. If the government issued a 20-year bond in 2020 at near 0% interest rates, interest costs on that debt won’t go up for 18 more years. Right now, we have a bunch of outstanding bonds that were all issued at different times, and at different maturities. Figuring out how fast our existing debt needs to be rolled over actually takes some serious work.

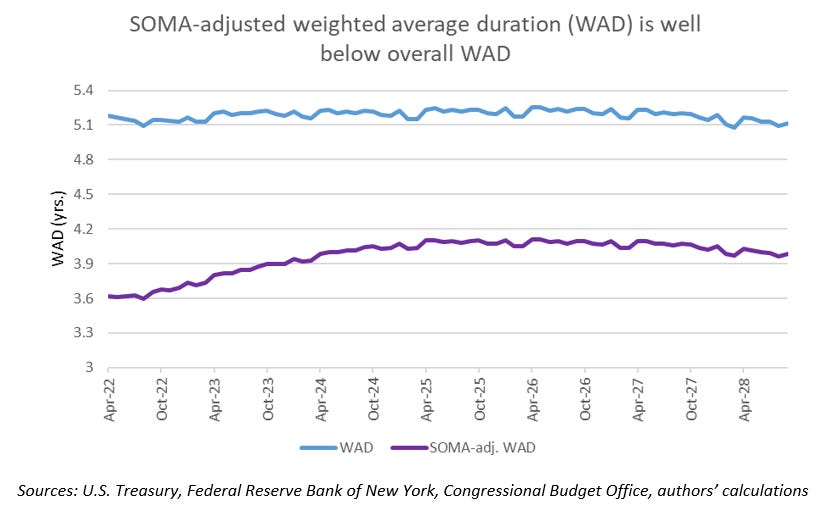

Fortunately, a team at Brookings has recently done this work. They found that the weighted average duration (WAD) of outstanding Treasury debt is a little over 5 years. And when you count “SOMA” debt that the Treasury owes to the Fed (which you probably should, since the Fed isn’t going to forgive that debt), the weighted average duration is only about 4 years.

It seems like a big mistake to me that we didn’t borrow at longer maturities to lock in low interest rates for a very long time. In fact, we kept making this mistake right into the spring of 2021, when inflation had already started to accelerate. Had we had the foresight to lock in low rates for decades, we would be facing much less of an interest cost problem in the 2020s. But anyway, here we are.

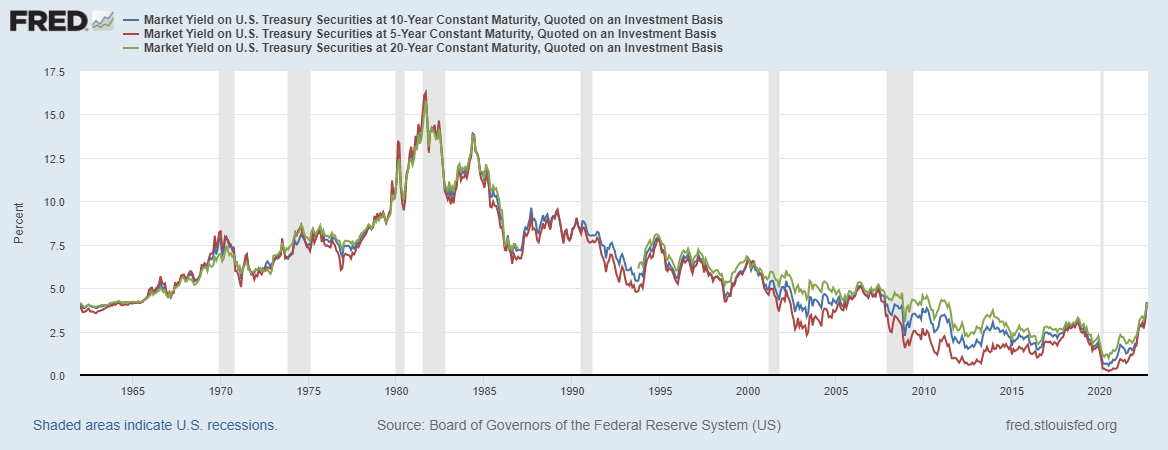

So we’ll have to roll over about half of our government debt over the next 4 years or so. And we’ll have to roll it over at higher interest rates. Here’s a historical chart of yields for 5-year, 10-year, and 20-year Treasury bonds, just to give you an idea of what we’re facing:

In historical terms, this really doesn’t look that bad. So far, yields are only back up to the levels of the mid-2000s, and not yet back to 90s levels. But there are two problems here:

Borrowing costs might go up more, as the Fed is forced to hike interest rates more and more in order to bring inflation down.

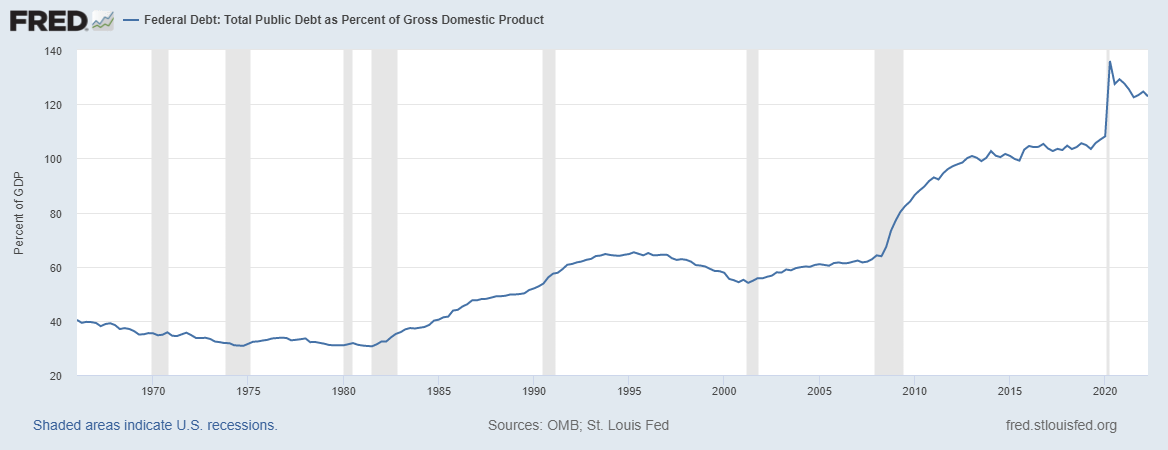

We have to pay interest on a much bigger pile of government debt than we did in the 90s and 2000s. Here’s government debt as a percent of GDP:

As a percentage of GDP, our debt is about twice what it was in the halcyon days of the 90s and early 00s. That means paying 5% interest on that debt would be as costly as paying 10% interest would have been back in 1995 or 2005. (The story is similar if you look at debt as a percent of tax revenues.)

So if something doesn’t change in the next 4 years or so, we could easily be paying 80s levels of interest costs on the federal debt. In this sense, Druckenmiller’s warning is right.

Two silver linings

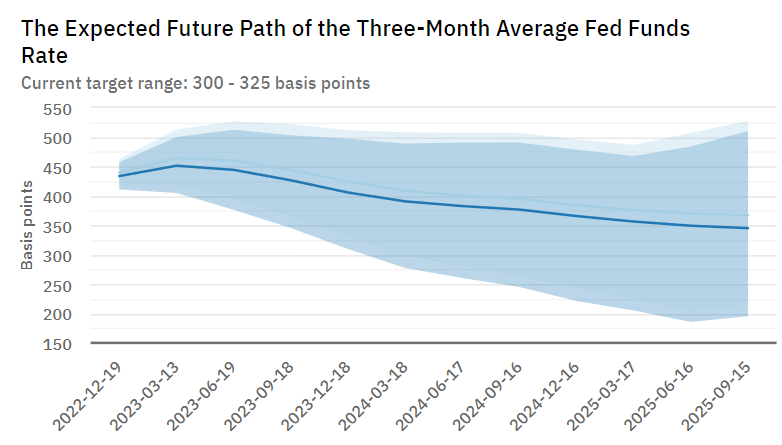

So why am I not alarmed? Well, two reasons. First, interest rates probably aren’t going to stay high for that long. The Fed currently predicts that it will start cutting rates in 2023. And markets expect this to happen too:

This will moderate the rise in interest costs a bit. Paying 3.5% interest on 120% of GDP will only be as painful as paying 7% interest would have been in the 90s. And in fact borrowing costs were about that high in the mid-90s. So this really isn’t too bad. And if inflation drops back to pre-pandemic levels, we can lower interest rates even more.

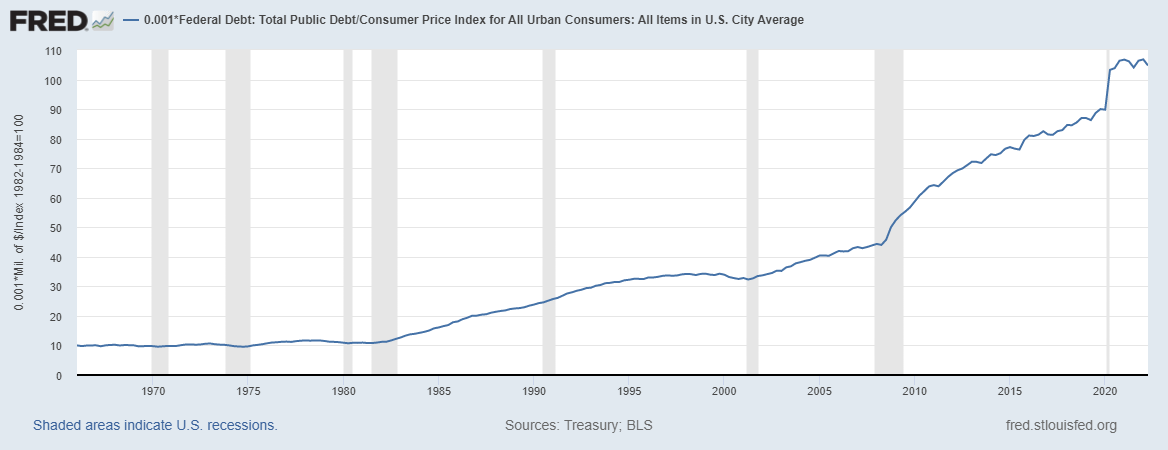

The second reason for calm is that inflation itself is eroding the debt. Notice how government debt as a percent of GDP has been going down for the last couple of years? Part of that is GDP growth, but part of that is just inflation. The government kept borrowing money, but the entire existing debt stock was shrinking in real terms. The result is that in inflation-adjusted terms, government debt didn’t even rise in 2021 or 2022:

In other words, we’re going to exit the current inflationary era with more expensive debt, but on a somewhat smaller amount of debt. And that debt erosion is permanent, even though higher interest rates will probably be temporary.

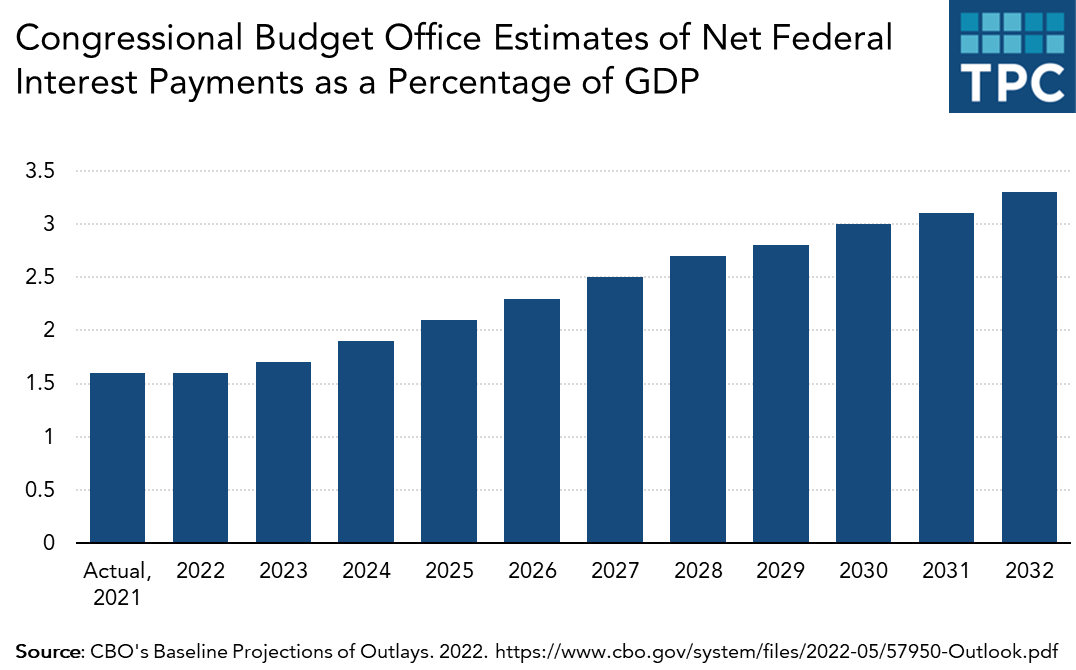

Therefore I do see increased interest costs in our future, but not as apocalyptic as Druckenmiller says. A return to the costs of the mid-90s seems reasonable. And in fact, this is exactly what the Congressional Budget Office projected, back in May:

That’s not exactly a ticking time bomb.

But although I don’t think we’re headed for a debt-service catastrophe, I do think it would be wise to engage in a little bit of fiscal austerity over the coming decade.

A little bit of austerity won’t hurt

Fiscal austerity will accomplish a couple of purposes. First, it’ll help hold down debt service costs, and second, it will help bring inflation down faster.

During the long slow recovery from the financial crisis and the Great Recession, “austerity” became a dirty word, and with good reason. With borrowing costs ultra-low and the economy far below its potential, there was every reason to borrow cheaply and spend on fiscal stimulus, and countries that chose to ignore this imperative tended to suffer as a result.

But now, a decade later, the situation has changed entirely — the economy is running hot, borrowing costs are higher and rising, and inflation is the big problem. Both basic Keynesian theory and financial reality say that in the current situation, the government should cut back. The UK is now finding out what can happen when a government pushes its fiscal luck too far. We’re in a stronger place than the UK, but that doesn’t mean we’re infinitely strong. Cutting back a bit is only prudent.

But what spending can we cut?

First, let’s talk about entitlements. Most of this is Social Security, Medicare, and Medicaid. When folks like Druckenmiller warn of the dangers of long-term debt, they often talk about how entitlements are projected to explode in cost. The CBO is sort of complicit in this, as it regularly releases deficit projections that show debt going up exponentially starting any day now.

But these projections always assume two things: First, that we won’t cut Social Security, and second, that health care costs will keep increasing at historic rates. Neither of these is likely to be true. They say Social Security is the third rail of politics, but when the system was about to become unsustainable in the past, we quietly raised the retirement age. It’s likely that we’ll do this again. As for health costs, these are a problem whether they’re paid by the private sector or the public sector. But as it happens, health costs as a percentage of GDP have leveled off recently. So it’s quite possible — even likely — that the age when health care costs went up and up has come to an end.

But if entitlements aren’t really going to eat the economy, they also probably won’t get cut by very much. Nor will other social spending, much of which is also health care. If we can bring down health care costs, that will be a big deal (and I’ll talk a lot about this in an upcoming post). But it’s unlikely that we’ll slash government health benefits outright.

And as much as we’d all like to live in an era of peace, defense spending will also have to go up, due to the return of great-power conflict. We need to not only replenish the munitions we’ve been sending to Ukraine, but also bolster our forces for the possibility of an imminent conflict over Taiwan, as well as raise spending on the military modernization efforts that we’re undertaking to match Chinese power in the 2030s.

So if social spending is going to hold steady and defense spending are going to increase, how do we get austerity? The answer is “taxes”. Since World War 2, federal tax revenue has fluctuated between about 15% and 20% of GDP. We’re now at the middle of that range. So we’re going to have to go to the top of that range for a little while.

Higher taxes are painful, and much of that pain will inevitably be borne by the middle class as well as the rich. But that’s the cost of maintaining a welfare state while also protecting the country against external threats. Having a nation is simply an expensive proposition. For a long time, rock-bottom interest rates let us get away with ignoring that cost. That era is now over.

I'm of mixed feelings but there's an important point you missed on the austerity point. While you hinted around it in inflation helping the real debt, inflation also makes cutting spending way easier as a political prospect by "increasing" funding less than inflation.

I've been banging this drum for over two years now but Treasury's debt management strategy is misaligned. They seem to be more concerned about issuing new debt in the manner that works best the primary dealers bidding at auction, rather than looking for the best way to manage debt for taxpayers.

It was easy to see that those extremely low rates were a rare opportunity that was going to go away. Treasury should have been extending maturities and willing to take the slight premium from buyers, knowing that the additional premium would be much smaller than the rate increase from any sort of return to more normal interest rates.