Turning the page on the Second Tech Boom

One chapter ends, another begins.

Around the time the above picture was taken, I took a trip to San Francisco. A friend of mine had just left academia to take a job as an engineer at Google — a decision more and more people I knew seemed to be making — and I went to housesit and take care of his cats over winter break. He lived close to Dolores Park, and every day I’d wander through, watching the young tech workers and hippies of San Francisco fly drones, practice acrobatics, and smoke weed. I felt that inescapable tug that I had felt visiting Japan in college; I had discovered the Place To Be.

Back in 2012, the Second Tech Boom was just coming into full swing. The IT industry had taken a decade to fully bounce back from the dotcom crash, but Facebook’s titanic IPO in May of that year showed that it had was back, and stronger than ever before. With the development of mobile computing and social networks, the internet had finally come into its own as the center of human life, and worries that advertising was insufficient to sustain massive business revenues were proving unfounded. Meanwhile, behind the scenes, cloud computing was transforming the way every company did business, enabling a new explosion of productivity tools and making it far easier to start a high-growth startup on a shoestring budget. The venture capital industry took advantage of the boom, with big new players like YCombinator and Andreessen Horowitz creating both new business models and a new startup culture.

That boom transformed the economic opportunities for the highly educated members of my generation. $100,000 a year for a job teaching in some little college town out in Indiana or Oregon is a career the vast majority of Americans would envy. But it looks like a bum deal compared to making $500,000 working in a shiny new tech office in San Francisco. If you were a recent college graduate, the choice was even easier. In 2005 investment bankers in NYC were the “masters of the universe”; ten years later, it was the hoodie-and-laptop set.

But this post isn’t a reminiscence about what life and business were like during the Second Tech Boom — it’s a retrospective. Over the past year, tech stocks have crashed, some big companies have stumbled badly, and a wave of layoffs has begun. The sudden evaporation of the crypto exchange FTX in a highly ridiculous burst of financial fraud will probably put a final fork in the era that began in 2012. But that’s merely a spectacular coda; the end of the boom has been driven by much deeper and more systemic factors that built up over a long period of time.

How do we know the Second Tech Boom is really over? Why did it end? And what does that mean for the future of the tech industry as we know it? I have some very definite thoughts on the first question, and some more speculative thoughts on the second and third. I think we’re at an important turning point, but that the tech industry will bounce back in a new form after a few years.

No “bubble” this time, but a slow deflation

No sooner had the Second Tech Boom began than people started calling it a bubble — and being wrong.

The mistaken bubble calls started appearing around 2011. In that year The Economist declared that “Irrational exuberance has returned to the internet world. Investors should beware”. The next year, an op-ed in Forbes declared “With Facebook Earnings, The Second Internet Bubble Is Over”. In 2013, Business Insider claimed to have “evidence that the tech sector is in a massive bubble”. And so on. To be fair, many others in the media disagreed, but concern over a repeat of the 2000 crash was present from the very beginning.

If you repeat a negative prediction about stocks for long enough, though, eventually you’re bound to be right. And even excluding the vaporization of much of crypto, tech stocks have surely received a mighty drubbing over the past year. Titans like Amazon and Google have taken big hits, but “medium-big” companies like Shopify, Twilio, Square, and Spotify have fared even worse:

Obasanjo makes a good point, which is that these stock collapses are happening the midst of a booming economy, with incredibly low unemployment and strong consumption growth. The S&P 500 is down from its peak a year ago, but only by about 16%. This bust is very tech-specific.

It’s important to remember that a stock crash, even in a single sector, doesn’t imply a bubble — at least, not in the sense of irrationality or “greater fool” speculation. Basic finance theory tells us that stocks with greater aggregate risk — that is, more exposure to broad movements in the economy — do better in good times and worse in bad times. Tech, in some generalized sense, is probably just high beta. Interest rates are going up and capital is getting more scare, and it’s not surprising that higher-growth sectors would suffer more than others.

And there are huge differences between this crash and what happened in the late 90s. As Andreessen Horowitz correctly pointed out in a 2015 presentation, the tech companies getting flooded with investor dollars in the 2010s pretty much all had revenue, and many had substantial earnings. Those revenues and earnings are why despite the stock declines, no one really expects a ton of well-funded companies to go out of business this time around, except in the fraud-ridden crypto sector. It’s also worth noting that the tech stock decline this time has been more muted than the crash of 2000 — that time, the Nasdaq Composite declined by around 70%, while over this past year it has fallen only around 30%.

That said, I do suspect that there was some amount of either over-optimism or speculation in the tech investment world of 2021. The darlings of the Second Tech Boom made a lot more revenue than their dotcom predecessors, but revenue doesn’t equal profits, and relatively mature companies like Uber were given enormous valuations without ever making their way to profitability. And of course there’s the entire crypto sector. So maybe there wasn’t a bubble, but there was some froth. Which means there’s reason to doubt that tech will quickly bounce back all the way to its 2021 highs after interest rates go back down.

Meanwhile, even a more modest crash is going to impact a lot of people, given how much bigger the tech sector is than in 2000. A lot of people are getting laid off.

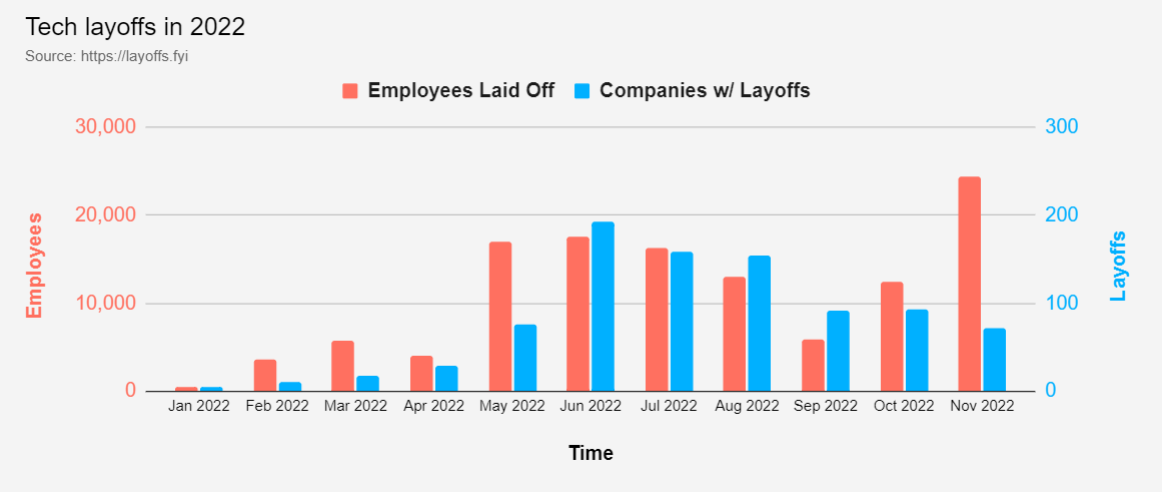

San Francisco, the place where I once felt such energy at the start of the boom, is getting hit hard:

And there’s no little sign the layoffs are over. Amazon just laid off 10,000 workers, and last week Meta announced 11,000. Meanwhile, numbers from the website Layoffs.fyi suggest that the cuts are now coming from fewer companies but are larger in size:

A combination of stock price declines and layoffs will likely lead to lower compensation throughout the tech industry. Layoffs and hiring freezes reduce labor demand — more unemployed or underemployed tech workers clamoring for a shrinking pool of jobs allows employers to at least restrain compensation growth over time.

In many cases, compensation will be actually fall by a lot. In most industries, it’s hard to actually cut workers’ wages, but in tech a lot of the compensation is in the form of stock, especially at the upper levels. Here, via the website Levels.fyi, is a picture of the salary of an “L7” at Google — a fairly high-level engineer.

The predominance of equity in these numbers means that when there’s a crash, all an employer has to do in order to slash comp is to fail to “refresh” the value of a worker’s stock grants to its pre-crash level. And a lower stock price will make employers especially reluctant to fully refresh equity compensation, since this will mean more dilution for the shareholders. So expect to see the big number above — which is about 19 times the U.S. median personal income — come down somewhat. (Update: In the comments, Nicholas Weininger, a former L7 at Google, has a much more detailed explanation of how this compensation works.)

So even if it wasn’t a true bubble, and most tech companies survive, and it’s not as bad as 2000, it looks like the tech sector is in for a period of sluggish performance and lowered expectations. That’s as good a place as any to put a bookend on the Second Tech Boom.

Why did the boom end?

The next question is why this long boom ended when it did. The proximate causes are easy enough to see — the pandemic ended, clobbering the business models of companies like Zoom and Peloton, then inflation rose and interest rates went up, making capital more expensive, and finally crypto blew up when it turned out (unsurprisingly) to be full of frauds. But I see some longer-term factors at work as well.

One is that network effects turned out not to be as common or as powerful as many had hoped. If an industry has network effects, it means that rich companies get richer — it makes more sense to get on the social network where everyone else already is, or develop apps for the app store that the most people use. This creates a natural “moat” that protects profits from competitors — and thus leads to the creation of incredibly valuable mega-companies. When I first started visiting Silicon Valley and meeting VCs in the early 2010s, they all talked excitedly about how more and more markets were becoming “winner-take-all”.

But this enthusiasm may have been overdone. A lot of markets that looked winner-take-all may have been a lot more contestable than people believed. A good example is Netflix, which twice soared above a price-to-earnings ratio of 400 (compare to ~25 for the Nasdaq) based on expectations that it would dominate streaming entertainment. But then the production studios and other competitors just set up their own streaming services instead, and Netflix started losing subscribers. That brought Netflix’s stock crashing down to a more reasonable P/E of 26; once heralded in the mid-2010s as one of the big “FAANG” companies, it’s now worth about the same as Comcast or CVS. Competition often finds a way.

As for big dominant “platform” companies, they may turn out to be fewer in number than people think. Facebook (now Meta) was the poster child for the Second Tech Boom — a company with an unassailable network effect that connected billions of users. If you were an advertiser, you had to advertise on Facebook (and instagram), and the platform would keep a substantial piece of that ad revenue. But recently, Meta ran afoul of an even bigger platform: Apple. Earlier this year, Meta’s stock price took a hit when Apple made privacy rule changes to its App Store. That was a strong hint that the App Store had platform dominance over Meta. Then in October, this was confirmed when Apple required App Store users to give it a cut of ad revenue. Overall, Meta’s stock is down by about 70% from peak, much worse than most big tech companies.

And then antitrust has to figure into this as well. Lina Khan’s FTC hasn’t really taken strong action against Big Tech yet, but it has made a lot of noise about doing so. That can definitely exert a chilling effect (though Apple’s recent moves suggest that the FTC should probably have focused on Apple rather than Meta.)

So those factors probably meant that optimism over tech companies’ earnings potential reached excessive levels. But I suspect there are also technological factors as well.

For a long time, the growth of IT was sustained by Moore’s Law. But the number of transistors on a chip, as well as the speed of the fastest supercomputers and the cost of memory, have all slowed down a bit since 2012. And the cost of continued improvements along these traditional axes has soared, such that the frontier is being driven forward by fewer and fewer player. This means progress in computing is being forced to search for new ways to improve — purpose-built chips like GPUs, parallel computing, new chip materials, low-power computing, and so on. But this means that improvements in the fundamental drivers of IT now have to come in areas where the growth curves are far less established and reliable than Moore’s Law itself. Which suggests that progress will require more ingenuity going forward, and ingenuity is always in short supply.

On the opposite end of the production chain, meanwhile, is the fact that the consumer internet itself seems largely built out at this point. Internet, social media, and smartphone usage are pretty saturated, especially in rich countries. And the internet has absorbed so much of our daily attention that there’s just little more to give — people already play video games in meetings and tweet at work. There will surely be more competition for eyeballs, as some platforms die and others take their place, but this fight will be ever more zero-sum. This is even true if Meta or someone else successfully inaugurates virtual reality as the next way of accessing the internet; VR is cool, but it cannot increase the number of minutes in a day.

Finally, the Second Tech Boom was driven in part by the financial side. Big players like Softbank’s Vision Fund and Tiger Global charged into the market, throwing huge piles of money at anyone who would take it, and forcing traditional VCs to raise and deploy larger sums just to stay in the game. The boom in crypto, despite all the obvious frauds and Ponzis, was a clear symptom of too much money sloshing around in the system — the financialization that typically comes at the end of any boom. But the big aggressive players are getting burned very badly now, and their pullback is probably exacerbating the bust in private tech markets. I wouldn’t be surprised if other investors are wary about imitating their strategies, at least for a decade or so. That will mean less money for startups for a while.

Another tech boom waits to be born

There will be a tendency among some people — especially the more tech-skeptical members of the commentariat — to view the end of the Second Tech Boom as some kind of failure on the tech industry’s part. It is no such thing. Yes, some of the crypto frauds are getting their (well-deserved) comeuppance now, but most of what the industry built since 2012 was good and valuable stuff. I’m quite glad we have a consumer internet, a smartphone industry, and a ton of SaaS tools. And the cloud computing infrastructure that got built to serve all those applications will end up being even more valuable in the future, just like the internet cables laid during the dotcom boom.

Progress proceeds in punctuated equilibrium.

Nor do I think the end of the Second Tech Boom means the end of growth for the tech industry, any more than the dotcom crash did. Remember that in the early and mid 2000s, even as the masses had taught themselves to scoff at internet companies because of Pets.com, Facebook was being created, the building blocks of the smartphone were being invented, cloud computing was finding its footing, and Google was coming into its own. If the next decade is marked by a receding tide of easy money, that will just mean greater opportunities for talented investors who can find good startups desperate for cash. It’s nice not to have to compete with Tiger Global.

It does seem, however, that the tech industry will shift direction in some ways. The transition from the dotcom era to the smartphone-and-social-network era was in some ways only a slight direction change in terms of the actual technologies involved — tech companies in the 2010s were still selling people computers, computer programs, and websites. Business models based on AI will probably be quite different; AI is a kind of information technology, but it’s not about networking people together.

A shift back toward physical (“atoms”) technologies is also probably in the offing, after decades spent largely neglecting these. I personally believe that batteries will be a game-changing technology, allowing extremely compact portability of energy for things like robots, appliances, drones, and transportation. There’s also the explosion in biotech, the sudden affordability of space launch, and the promise of cheap solar electricity. All of these will involve very different models than the social networks, SaaS, and smartphone apps that became standard in the last boom.

There will also probably be important technologies that I haven’t even given much thought yet. How many people in 2002 would have predicted the socially transformative impact of digital cameras?

Human ingenuity has not flagged, or even slowed down, nor has the perennial human desire to make money off of new technologies. The early winners of the Third Tech Boom, whether it comes in 2027 or 2037, will be the people who see the possibilities of the new technologies early on, and are mentally unconstrained by the impulse to pattern-match on what was successful in the last boom.

That’s why I think it’s useful to bookmark the end of the previous era in innovation. The less we linger over the past, the quicker we can hop on to the next thing.

I used to be an L7 at Google, and a manager who set comp for my reports. I think that your sentence:

"The predominance of equity in these numbers means that when there’s a crash, all an employer has to do in order to slash comp is to fail to “refresh” the value of a worker’s stock grants to its pre-crash level." gives an incomplete picture of how bad the morale effect will likely be, and I need to get into the compensation mechanics weeds a bit to explain why.

For those unfamiliar with big tech company comp practices: typically you, an employee, get a comp letter each year after annual performance review, around about early December. The letter has three components. The first is your salary for the coming year, which typically applies a percentage raise to your salary for the current year, where the magnitude of that percentage is performance-based. The second is your bonus for the current year, which will be paid out the following January as a lump sum; the lump sum amount is based on your level and performance. And the third is an equity "refresh grant" amount, which is an annual new grant of restricted stock shares (they used to grant options but haven't for more than a decade now) that vests on a schedule. The vesting schedule is typically four years long, sometimes starting immediately with 1/48 of your grant vesting each month, sometimes starting with 1/4 of it vesting a year after the grant date and then 1/48 each subsequent month. The grants overlap and the overlapping vesting schedules serve as "golden handcuffs," in the sense that at any given point if you leave the company you are leaving on the table a bunch of shares that are granted but not vested. So the size of the grants are set based on expected future performance potential, i.e. how much the company cares about keeping you around for the next four years. If you really wanted a low performer to get the message that they were on the way out, you'd give them zero equity grant in their comp package.

Now, if the equity grant levels were set and reported to employees in terms of numbers of shares of stock per grant, and if the overlapping vesting schedule didn't make the cash flow trajectory so much more complicated, what you said would be completely correct. If your performance is flat, your new grant this year would be the same number of shares as last year, only those shares would now be worth much less than they were in your last grant, so the dollar value of your comp would go down without actually cutting any of the nominal parameters in your comp package. People would still notice, but it'd be much less obvious and obnoxious than a nominal salary cut.

And they did actually used to denominate equity grants in numbers of shares-- until the mid-2010s when the stocks started taking off at unpredictable but high rates of increase. Then the comp policies changed so that the equity grants were reported to employees *as a dollar value*, and the number of shares in the grant was chosen to be that much money worth of shares at some index date, say January 1 of the upcoming year. So as I remember and understand it, if your equity refresh grant value for a year was $250K, and GOOG happened to be worth $100 a share on January 1, you'd get 2500 shares in your grant.

This had two advantages in the mid-to-late 2010s. First, it gave employees a better sense of the expected present value of their total new compensation grant. Second, as long as the stock kept going up and up, the company could achieve the same nominal comp grant value with fewer and fewer shares.

But when the stock crashes, two things happen. First, the company has to *increase* the number of shares in comp grants or else cut their nominal value in a way that is obvious, easily measurable, and immediately morale-chilling to employees. Second, the value of previously granted shares that are now vesting goes down to less than the nominal value they were reported to have at grant time, so actual cash flow comp goes down *even if* forward-looking grant amounts are increased proportional to the stock price decline, and people who have been reckless enough to e.g. take out mortgages that are only payable if their total cash flow doesn't go down are in a bind. When we managers were planning comp we would get enough info about the values of people's prior grants to know if this was happening to them, because we knew it created a severe retention risk if you let someone's cash flow go down.

Now it's certainly possible that they won't even try to make employees whole for any of this. They could just say: look, we're in a recession, you can't go out and get a competitive offer from another company anytime you want the way you used to, therefore we don't have to avoid de facto comp cuts to keep you around, please understand how tough it is out there and be reasonable. That is definitely not what happened in 2008-09, the last time tech stocks went down a lot: back then they made us whole and then some. But revenue growth rates are not what they were in 2008-09 and the payroll is probably more bloated now than it was then too.

But one way or another, the choice is going to be between a large and very directly perceived comp cut and a major, major increase in shares per grant and thus in dilution rate. Caveat: the above description is several years old now; they may have changed some of the mechanics of this since I left, or I may be misremembering some detail about how the index pricing worked.

When the dot.com boom went bust, a lot of tech info headed to the hinterlands, small towns, rural areas, secondary cities and suburbs. This helped spread out a lot of talent, that filled in a lot areas for the economy, all over the U.S. People came in and set about fixing up payments and taxes with programs run on computers, not adding machines. It made American business overall more productive, which was seen in the boom that followed the bust.

It is my expectation, that all of these recently let go or fired employees, will find new jobs, with different companies, doing different things, but that once again spread the knowledge and ability of what tech can do. Lower costs, and see that businesses become more profitable and exposed to new ideas, as least where they are concerned.

The future, despite this kerfuffle is still bright, put on some shades.