The wreck of Bidenomics

Fortunately, we have a good idea of where to go from here.

It really pains me to have to write this post.

I had high hopes for Bidenomics. The combination of the Covid emergency, Chinese competition, and general American anger at long years of stagnation and inequality felt like they might motivate this country to get up off its butt and do something to improve the situation. And it felt like Biden’s people had a good, cohesive program for improving the situation, which I thought would be fairly effective. I wrote:

The tenor, pace, and scope of Biden’s economic programs proposals, and the muted nature of the ideological opposition, suggest that we’ve entered a new policy paradigm — much as when FDR took office in 1933 or Ronald Reagan in 1981…

The Biden program is multifaceted — it includes things like support for unions, environmental protection, student debt cancellation, immigration, and a bunch of other stuff. But it would be wrong to characterize his program as merely a grab bag of long-time Democratic policy priorities. Three approaches stand out above the maelstrom:

Cash benefits

Care jobs

Investment…

Cash benefits were at the center of the COVID relief bill that already passed…A child allowance [is] basically a pilot universal basic income program for families…

The new “infrastructure” bill includes tens of billions of dollars a year for long-term in-home care for disabled and elderly people…

The third pillar of Bidenomics is investment — government investment, and measures to encourage private investment. The former includes tens of billions a year in new research spending, massive construction of new green energy infrastructure like electrical grids and charging stations, retrofits of existing infrastructure (e.g. lead removal from pipes), and repair of existing infrastructure like roads and bridges.

15 months later, it’s looking like my optimism was unwarranted. Yes, FDR and Reagan both accomplished much less than they wanted (their policy revolutions were completed by their successors). But they accomplished something, at least — FDR the New Deal, and Reagan a giant tax cut and anti-union policies. In comparison, Biden’s two legislative achievements have been:

1) A Covid relief bill that was marginally smaller than Trump’s, and

2) An infrastructure bill that was good and necessary but really just plugged a hole from the previous decade of disinvestment.

Now Joe Manchin has announced that he will let essentially nothing more of substance pass the Senate. And with Republicans likely to take back at least one house of Congress in this year’s midterm elections, it looks likely that this will be the final word on Bidenomics. That doesn’t mean Biden’s presidency will be a failure — there’s still the Ukraine war, executive-branch regulation, and so on. But economically, this is a legacy that would be mediocre even in normal times. It’s definitely a lot less than Obama managed. And it’s far short of what the initial rush of successes seemed to foretell.

Why I’m now pessimistic about Bidenomics

Legislative frustration by itself doesn’t spell final doom for Bidenomics as an idea. FDR and Reagan’s agendas were both carried to fruition by successors — and by leaders from the opposition party who felt the need to triangulate. Eisenhower and Nixon made large and substantive contributions to the New Deal package of policies, while Jimmy Carter and Bill Clinton arguably carried out more of the Reagan Revolution than Reagan himself. But I’m not as optimistic that this will happen with Bidenomics, for one simple reason: Popularity.

Here’s the 1932 election map:

FDR pulled off four thumping victories in a row, and in the process swept his party to large Congressional majorities:

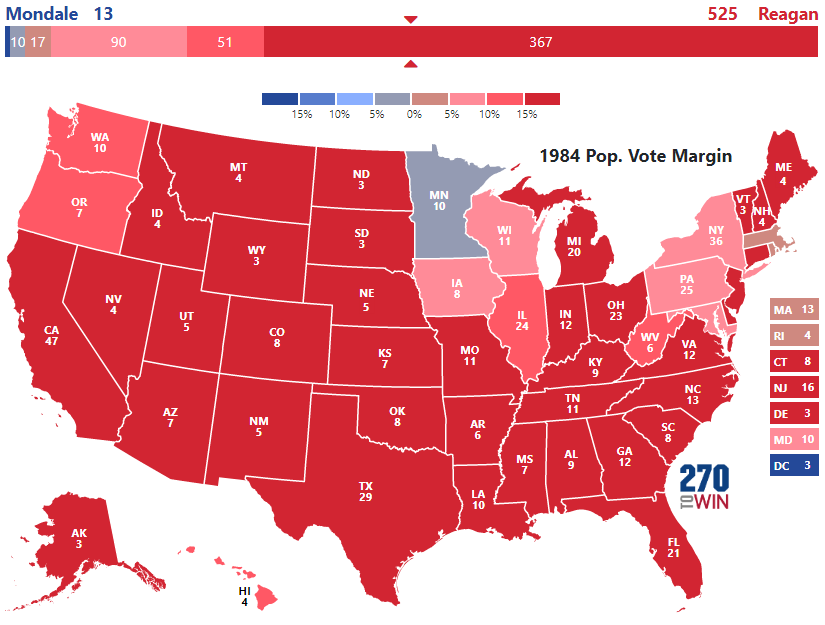

In other words, Eisenhower and Nixon got with FDR’s program in part because it seemed like it had been validated by economic and military success, but also partly because they felt they had to in order to win elections. The same was true with Reaganomics. Here’s a map of Reagan’s reelection in 1984, in which the Democratic candidate won only a single state:

This was why Bill Clinton (and to a large extent, Barack Obama) felt the need to triangulate.

Joe Biden’s victory, however, was by a slim margin:

A bit of the narrowness is due to the Electoral College and the differing geographical distribution of partisan votes across eras. But the popular vote was also much closer in 2020 than in the FDR and Reagan elections. And Biden didn’t score anywhere near the sort of dominant Congressional majority that FDR scored (but which Reagan, notably, failed to garner).

Moreover, it doesn’t look as if what Biden has done will be a big enough success that future Presidents from either party feel a need to follow in his footsteps. Employment is very high in America, but inflation is rampant and real wages are falling — as a result, consumer sentiment is about as low as it was during the Great Recession.

And this has, predictably, led to Biden’s approval rating trending relentlessly downward, until by now it’s even lower than Donald Trump’s was at a similar point:

This isn’t a legacy future leaders from either party are going to seek to emulate; it’s a legacy that they’ll try to run away from. Biden looks a lot more likely to be the “next Carter” than the “new FDR” or the “Reagan of the left”.

Manchin is bad, but Bidenomics just didn’t catch fire

The easiest explanation for the failure of Bidenomics is simply that there was one recalcitrant Senator, Joe Manchin, who personally refused to allow it to succeed. And in some narrow sense, it’s true. With a 50-50 partisan split in the Senate, and Republicans unwilling to break ranks to support Biden’s Build Back Better bill, Manchin could essentially dictate economic policy. Many pundits and legislators believed they could craft some compromise that would meet Manchin’s demands, but it is now pretty clear that no such compromise was ever really on the table.

But the failure actually goes a lot deeper than Manchin. One reason is that what I thought of as the first pillar of Bidenomics — cash benefits — turned out not to be as popular as many had hoped. The idea was that because the expanded child allowance was quasi-universal, it would garner broad support like Social Security did. Initial broad support for the policy seemed to validate that hope. But then, surprisingly, most Americans didn’t want to make the child benefit permanent. Whether that’s because Americans are in a stingy mood, or because they believe that government benefits should come with work requirements, or because they’re worried about the inflationary effects of cash benefits is not yet clear. But what is clear is that cash benefits failed to get the broad popular buy-in that FDR’s social insurance or Reagan’s tax cuts secured.

Climate investment ran into a similar problem. Despite accelerating heat waves, wildfires, and floods, Americans place a pretty low priority on climate action:

If people just don’t want what you’re selling, it won’t happen, even if it’s a good idea.

Is Bidenomics fit for purpose?

But there’s a third big reason Bidenomics failed, and it’s that substantial parts of the program didn’t actually address the needs of the nation as much as I thought they would. As the British say, key elements of Bidenomics turned out not to be “fit for purpose”.

First, care jobs. A big pillar of Biden’s agenda was the “care economy” — the idea that as manufacturing jobs get automated away, people will move en masse into health care, eldercare, education and child care. In fact, this has already been the trend for many decades now. So Biden wanted to speed the transition along, to ensure mass employment with good wages.

But the thing was, the U.S. didn’t really seem to need that sort of a push. The economy seems to have done a good job at restoring mass employment on its own, with the prime-age employment rate — the best single measure of labor market health — bouncing back to about 80% after every downturn.

As for wages, these have become a bit less unequal in the last decade. Since the mid-2010s, wages in the bottom half of the distribution have outpaced wages in the top half, with the lowest quartile seeing the biggest percentage gains:

The common progressive belief that inequality trends upward without a big corrective push by the government may simply be false, at least as far as wage income is concerned. The mild but consistent improvement here could have taken away some of the impetus for a big push to create care jobs.

It’s worth noting here that I always thought the “care economy” was by far the weakest of the three pillars of Bidenomics. It basically shovels government subsidies at industries that are already vastly overpriced, which will increase their cost to users (and just about everyone is a user of health care, child care, and eldercare). In other words, it provides jobs and wage boosts to the few but at the expense of higher costs for the many. So I was always wary of making this part of the agenda.

A pillar I did strongly believe in — and still do, really — is cash benefits. Cash is far simpler to administrate than welfare with means tests and work requirements. It catches all kinds of people who fall through the cracks of more targeted systems. If it’s done in a more universal way, it avoids many of the perverse incentives of means-tested programs. Not all the research supports cash benefits, but a lot of it does. I still think cash has the potential to become the future of our welfare state.

The problem here is the macroeconomic situation. In the Great Depression, our economic problem was unemployment, as it also was during most of the Obama administration. In 2022 our problem is definitely inflation. And whether or not the cash benefits handed out during Covid were a major cause of the current inflation, it’s definitely true that cash benefits are inflationary. This is because poorer people spend a lot more of their income than rich people, so giving poor people a bunch of money means a boost in spending, whether or not you pay for it with taxes on rich people. If you don’t pay for it with taxes, and just borrow to pay for the benefits, it’s even more inflationary.

That doesn’t mean cash benefits are a bad idea; it just means that we have to get inflation under control before we start doling out a lot more of them. In fact, we sort of did this in the 90s; with inflation having been conquered in the 80s by Paul Volcker, Bill Clinton felt safe in expanding the EITC (a form of cash-based welfare), which contributed to the increasing progressivity of the U.S. fiscal system during that decade (Clinton’s assertion that “the age of big government is over” was just marketing B.S.).

An inflationary economy simply isn’t the kind of thing the progressive economic policy package was designed to deal with. The playbook inherited from FDR and the New Dealers, which is now embraced by the aptly-named Roosevelt Institute and many of the other progressives advising Biden on economics, is all about fighting depressions. It’s about mobilizing big government to take over when the free market has failed, pumping up aggregate demand, providing jobs, boosting wages, and carrying out needed investment.

The investment part of that is still vitally important (and would be deflationary in the medium term due to increased capacity). But the other two pillars — a big push for care jobs and a big increase in cash benefits — look more suited to 2009 than to 2022. (This is not to say that small-government Reaganomics is the answer to inflation either, of course; in fact, it probably didn’t even help reduce inflation in the 80s!). An economic program comprised of one-third stuff we really do need, and two-thirds stuff that looks out step with the biggest economics problems facing the nation right now, is not likely to catch fire.

So why didn’t Democrats see this, and prioritize the investment piece of Bidenomics, shelving the other two pieces until inflation comes down? Well, some definitely tried to do that, paring down the BBB bill to mostly just the climate pieces (which Manchin then killed), and talking up the disinflationary benefits of investment. But it was too little, too late; BBB had spent much of its life as a giant grab bag of giveaways to the Democratic party’s kaleidoscopic collection of competing interest groups (the most ridiculous being a hideously expensive tax cut for upper-income people in high-tax states). That lack of leadership and focus certainly played a part in Bidenomics’ eventual downfall.

The way forward

All of this leaves us with the big question: Where do we go from here? As I see it, the answer has to be some form of what Ezra Klein calls “supply-side progressivism” and Derek Thompson calls “the abundance agenda”. America isn’t dealing with a crisis of jobs right now; we’re dealing with a crisis of costs, both in the macroeconomic inflation sense, and in the long term everything-costs-too-damn-much sense. Making life less expensive for regular Americans is a mission that fits the times we’re in.

Government investment — and encouragement of increased private investment — has got to be a big part of this. High-quality infrastructure and public goods like R&D funding are important for boosting growth in real incomes. And a big push for abundant green energy — whose costs are already lower than fossil fuels and falling by the day — is key to making all kinds of things cheaper.

It’ll also mean a big push for cheap housing and better transit. That will include lots of upzoning and other deregulation, but also a push for government-constructed housing. The YIMBY movement shows the way ahead here; with cities all around the country following coastal hubs into unaffordable territory, this needs to be a nationwide movement.

It will also mean establishing a national health insurance system. This should not be an expansive single-payer system like the plan advanced by Bernie Sanders, focused on eliminating out-of-pocket costs; instead, it should be a system where the government pays some portion of every medical bill and leaves the rest to private insurance. That’s the system used in Japan and South Korea, and it’s very good at keeping costs down, because the monopsony power of the national insurer allows it to negotiate down prices for all services.

I believe this sort of progressive agenda would win broad support. Progressive policy advisors, think-tankers, and pundits should move away from the idea of providing mass employment, and toward the idea of providing mass abundance. Bidenomics is dead, but that doesn’t mean progressive economic policy is dead. We don’t have to repeat the 1980s here. Progressives just need to pivot, and offer America more of what it needs today instead of more of what it needed in 1933.

Update: Some great news, as Manchin has agreed in principle to a reconciliation bill that’s focused on investment. Cash benefits and care jobs are gone, as I predicted, but the important and good piece of Bidenomics — the part that’s in keeping with the Abundance Agenda — is still in place. That’s great to see. And the CHIPS Act, which just passed the Senate, will provide another boost to government investment (and private investment). Good, good.

It is probably worth tackling the elephant in the room when it comes to housing costs: every purchase of a house for a price that the buyer thinks is astronomical and indicative of the sheer lunacy of the housing market, is also a sale of a house that the seller thinks is a potentially life changing influx of cash in exchange for an asset that they invested in and feel entitled to profit from.

There is a generation of people who are counting on the sale of a house at a high price to partially fund their retirement. Any policy designed to provide relief to the buyer in that situation will, by definition, also provide pain to the seller. And those sellers are very typically older people (boomers, often), who vote.

So in truth, we will not deal with housing until we are ready to turn the page on the boomer generation. Because we have to piss off the old people to fix this, and to date our country has been categorically incapable of committing to any course of action that does that. So we won't fix the housing market until we are capable of crossing that bridge. And I wholeheartedly support racing towards that goal.

This would be a huge deal. Perhaps the most important thing that our country could do. Our governments at every level are currently struggling under the accumulated weight of having to deal with 50 years of boomer bullshit. Every stupid political battle they had, every compromise to please the special interests of their generational priorities, every convoluted plan to deal with (or avoid dealing with) all of the self-indulgent nonsense that they marinated in since the 70's.... All of it has crippled our institutions and enfeebled our government.

Now that the people themselves are clearly so infirm as a generation, can we finally take power from them and move on? If we can't, then we will allow our country to be driven over a cliff by what is essentially a ruling class of senile, barely lucid octogenarians.

Instead, we should make housing the first stand in this generational battle. Piss off the sellers (the elderly) for the greater benefit of the buyers - families, students, workers - you know, the future of the country! Any society whose decisions favor the past rather than the future is doomed to collapse. So let's prioritize prosperity for the future rather than for the past.

I think a huge cause for Biden's unpopularity is inflation, and the average American falsely assuming that the President is the one primarily responsible for controlling it.

If this global inflation had not occured, and we were instead in a "regular" economy, the average voter could easily have gotten on board with focusing on climate change, cash benefits, voter rights reform, and the like.

I imagine the history books are going to include a quip about how inflation was very high under Biden's Presidency. But will they also mention how any economist would attest that the vast majority of power to control inflation is vested outside of the Oval Office? I doubt it.

And that's kind of bullshit, frankly: how someone can do the right things, but bad events happen outside their control, so people just assume it's their fault. Everytime I read an article that casually mentions Biden's approval and inflation, I feel like I'm taking crazy pills. How hard is it for the media to acknowledge that it's mostly outside of the president's control? And why do even the more enlightened writers, including yourself, simply take it as a given that people will blame the president for inflation or the economic cycle in general, without stopping to comment on how unfair that is? Why is this a thing that we are ok with, or don't bother trying to fix?