So, how can we lower gas prices?

There are a variety of options.

These days when I talk about the need for rate hikes to bring inflation down, I’m sometimes confronted with the argument that the only thing that needs to come down is gas prices. The thinking seems to be that even if much of our inflation is due to high aggregate demand, gas prices themselves are due to a supply shock, perhaps from the Russia sanctions. And if gas prices, rather than inflation in general, are what Americans really care about, then really we don’t need to focus on beating inflation itself; we just need to find some way to increase the supply of gasoline. So, no need for a Fed-induced recession.

Or so the theory goes, anyway. The idea that Americans mostly just care about gas prices, instead of about inflation, has partial empirical support from the political science literature. Harbridge, Krosnick, & Wooldridge (2016) do find that while inflation matters for presidential approval ratings, gasoline prices also matter above and beyond inflation itself. Here is an interview where they discuss their results.

So while gas prices aren’t the whole game, they do have a special importance. So how to get them down? The best thing to do is to build more transit and to switch to electric cars, and we need to do this as fast as we can. But this takes a lot of time, so we also need some other measures that work faster.

A new report by some folks at the Center for Public Enterprise suggest some very sensible measures — fare holidays for cheap transit, accelerated and streamlined approval of transit projects, and encouragement of more work-from-home. But it also has some suggestions that involve asking Americans to cut back — encouraging carpooling and reducing national speed limits. I fear that this approach would end up repeating the mistakes of the Carter administration — demanding that Americans cut back on their lifestyles has never been a great political move.

So to lower gas prices, we need some more palatable alternatives. In fact, there are a number of things we can do. The first thing, interestingly enough, is to raise interest rates.

Rate hikes will bring down gas prices — at a price

Interest rate hikes reduce aggregate demand. That means a reduction in demand for basically everything that people buy, including gasoline. Reduced demand means price goes down; thus, rate hikes will bring gas prices down.

Now, this effect is seriously diluted by the fact that demand for oil is global. The U.S. consumes only a fifth of the world’s oil, so if demand holds up in other places, the effect will be marginal. But central banks in other countries do tend to follow the Fed to some degree, and inflation is a problem in most places, so we’d probably be looking at a semi-coordinated series of rate hikes.

(Also, it bears mentioning that although the market for oil is global, the market for gasoline is less so. Gasoline has to be refined, and a U.S.-specific reduction in demand would put a squeeze on refiners’ margins. I’ll talk more about this in a bit.)

In fact, there’s a very basic reason why rate hikes could bring down gas prices a whole lot. It’s because both the supply of gasoline and the demand for gasoline are highly inelastic in the short term.

Inelastic supply and demand means that the amount people want to buy and the amount they want to sell isn’t very sensitive to price changes. And in the short term this is true — if you charge people double for their daily commute, and there’s no good train in the area, most people are just going to pay up. That’s why it hurts regular Americans so much when gas prices go up — our national dependence on car transportation gives them little alternative but to suffer. As for supply, it generally takes time to develop new oil supply (or to convince the Saudis to turn on the taps, I suppose), so that’s pretty price-insensitive as well.

But the flip side of inelastic supply and demand is that a small reduction in demand can lead to a very big reduction in price. Here’s what that looks like:

So a little really goes a long way here. A modest international campaign of rate hikes could send gas prices way down.

The question we should then ask is whether this is worth doing at all. If gas prices are a supply problem, how is reducing demand — which hurts the economy even more — a solution? The answer to this question can only be a political-economic one: If lowering gas prices is more important to the American public than avoiding a recession, then that’s what we’ll probably end up doing. In fact, there is some evidence that voters care more about inflation than about growth (which stands to reason, since inflation affects more people than unemployment).

But that doesn’t mean that supply-focused solutions are wrong. Indeed, we should be trying to raise oil and gasoline supply as much as we can right now. Easing supply constraints makes all the rest of our policy tradeoffs much less harsh.

How to pump more oil

First, the good news. Everyone thinks there’s going to be this huge negative supply shock from the cutoff of Russian oil sales to the West due to sanctions. But this oil mostly won’t be taken off the market — Russia will just sell to China and India, who will get a special discount on their Russian oil purchases and will thus purchase less from Saudi Arabia, Nigeria, or wherever — freeing up more oil for U.S. consumption. So we’re probably not dealing with that huge of a supply shock here.

So how do we boost supply? The most obvious thing to do in order to increase gasoline supply is just to increase oil supply. Oil and gas prices tend to move together (though oil is a bit more volatile):

Of course, many people will yell “Just frack! Drill baby drill!” And this is the goal, but it’s not so easy.

First of all, just like oil demand, oil supply is a very global thing. The U.S. boosting oil output alone will boost global supply only modestly. In fact, our best hope is probably to use U.S. fracking to spur the Saudis and other OPEC countries to turn on the taps as well, in an attempt to reduce prices even more and drive all the higher-cost U.S. producers out of business. As Robinson Meyer explains in a recent article, OPEC is widely considered to have the world’s biggest reserve of “spare capacity” — i.e., supply that they can turn on and off quickly. Thus, some combination of jawboning the Saudis and threatening them with U.S. competition is probably the best approach.

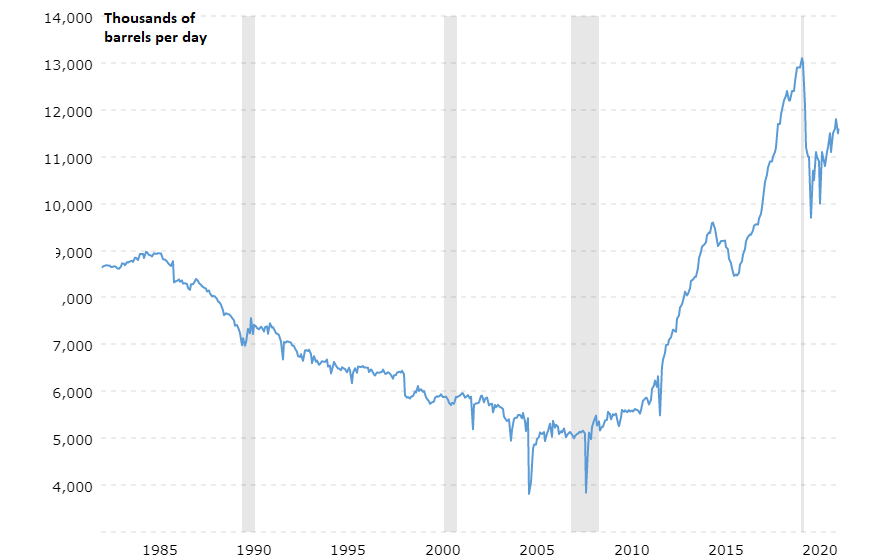

So what’s the best way to “drill baby drill”? In fact, U.S. crude oil production, though down a bit since the start of Covid, is still pretty high:

So the narrative that the Biden administration has been holding back shale production with burdensome regulation and anti-oil rhetoric needs to be put in perspective here. The U.S. is still drilling quite a lot.

But the narrative is not false, either. Biden halted new leases for oil drilling on federal lands, and has tried to push through a new SEC rule that will require companies to disclose their greenhouse emissions levels. And he canceled the Keystone XL oil pipeline and greatly increased the requirements for building other oil pipelines.

This approach makes sense in the long term, because of the need to fight climate change. But if the GOP wins in 2024, not much climate-change-fighting is going to happen for a while, so Biden is probably thinking of putting short-term considerations over long-term ones here. A sensible middle path would probably be to encourage increased oil production by deregulating the sector for now, but at the same time to increase subsidies for a rapid transition to electric cars and transit.

There’s also the question of whether the oil sector has become too concentrated. This can be solved with policies that explicitly encourage new small, independent oil producers to enter the market rapidly, say by offering tax breaks to new drillers. Claudia Sahm suggests setting a price floor for oil producers. There are a lot of policy tools available here. But whatever tool we use, the main hurdle will be psychological — a mental pivot away from fighting climate change as the singular overriding short-term objective of public policy.

Refineries: Why gas is more than just oil

It’s also important to remember that Americans don’t pay for crude oil; they pay for gasoline. As you can see from the graph above, oil and gas prices move together but they don’t track each other precisely. In the early 2010s, oil prices were almost as high as they are now, but gasoline prices were much lower. What’s the difference? Refineries:

Refineries are raising gasoline prices well above what crude oil costs dictate. This means they’re making enormous profit margins. Theoretically this should prompt companies to build more refineries, but for some reason they aren’t doing so:

According to the Energy Information Administration, the United States will be using about 95% of its refining capacity in June. Yet, we’re refining about a million barrels per day less than we were just a couple of years ago…

[I]f refiner’s margins are so big and they’re making a killing on every barrel of fuel they get to market, why don’t energy companies just build more refineries while the money’s there?

It takes a lot of money and time to build refineries. Additionally, “investors do not want to see companies pouring money into organic oil and gas growth,” Gabelman said.

The long-term prospects for fossil fuels are uncertain. Most investors don’t want to be asked to chip in for long-term growth. In the present economic climate, they’re demanding a quicker return on their investment.

This smells like classic monopoly behavior — restricting output in order to rake in profits. And indeed, refinery capacity has fallen by about a million barrels since Covid struck, suggesting that there may have been some increase in market power:

But this is really only a very modest decline. And distillation inputs — a measure of actual production — have fallen by less than capacity. Nor does there appear to have been an especially big wave of mergers in the oil industry since the early 2010s. And even if monopoly power is a big part of the reason for restricted capacity, it’s not clear that having Joe Biden yell at refiners to accept lower profits and refine more gas will have any effect on the economic bottom line.

What’s more, it’s not clear that any policy to encourage new entrants into the refining industry would have an effect in the sort of time frame we need here. Unlike shale wells, which can be drilled very quickly, oil refineries take three years to build. Some have suggested that we might be able to reopen recently shuttered refineries, but it’s not clear how technologically feasible or quick that would be.

Still, encouraging new market entrants is a good idea. The reason is that existing refiners will have an incentive to reduce their profit margins a bit in order to keep competition out of the market. In fact, we could even have the government get into the refining business. This competitive motive could relieve some of the pressure on gas prices, potentially very quickly. (You’ll notice a similarity between this and the “frack more to make OPEC produce more” approach.)

Again, as with fracking, the main barrier here is mindset. The private sector has spent the last few years gearing up for a big ESG investing push to drive fossil fuels out of the market, and the Biden administration supported this approach with regulation and rhetoric in 2021.

But this is 2022, not 2021. Right now, inflation is Americans’ primary concern and also the primary threat to Democrats’ chances in 2024. And since gas prices are the most important single piece of inflation, it’s probably time to temper the anti-oil crusade for a little while. Subsidies for electric cars and public transit should take the place of restrictive measures aimed at shutting down the production of gasoline. That will be a difficult mental whiplash for many, but desperate times call for flexibility and adaptation.

It really stresses me out to see this all laid out here, and then to see the Biden admin’s proposed solutions, and to note that they have approximately 0 overlap.

US petroleum refinery capacity has dropped partly due to bad luck (explosion in 2019 knocking Philadelphia Energy Solutions refinery off the market) and partly due to the generous incentives offered by California's Low Carbon Fuel Standard. Neste and Valero figured out early that they could make fat profits by pouring modest-cost feedstocks like UCO (used cooking oil) and beef tallow into refurbished petroleum refineries, and producing renewable diesel. So other petroleum refiners, notably Marathon, figured they could get into that game, especially in 2020, when the outlook for petroleum refining looked dismal. So the Martinez CA petroleum refinery went off line in 2020, and is coming back online in 2022 as a renewable diesel facility. There are other players doing the same thing, which has eaten into the US petroleum refining capacity. Of course, there's not enough beef tallow and UCO to go around, so these bio refineries will be looking for other feedstocks, like palm oil (sorry orangutans) and soybean oil (look out Amazon).