MMT and the meme-ification of macro

Goodbye models, hello memes

MMT is very difficult to engage with, because it’s hard to pin down what the theory actually says. You’re typically reduced to either crawling through interminable MMT writings that make the same sort of vague hand-waving points over and over, or asking questions of irascible gurus whose pronouncements sometimes contradict each other (but who always seem agree on the basic fact that you’re a contemptible idiot). On the few occasions that MMT people actually write down a quantitative model, the results are…a bit concerning.

So it’s helpful that MMT now has an actual textbook — “Macroeconomics,” by William Mitchell, Randall Wray and Martin Watts. I haven’t read it yet, but Scott Sumner (of the Mercatus Center and Bentley University) is going through it, and already a few tidbits are emerging that I think shed some light on both MMT and the macroeconomics debate in general.

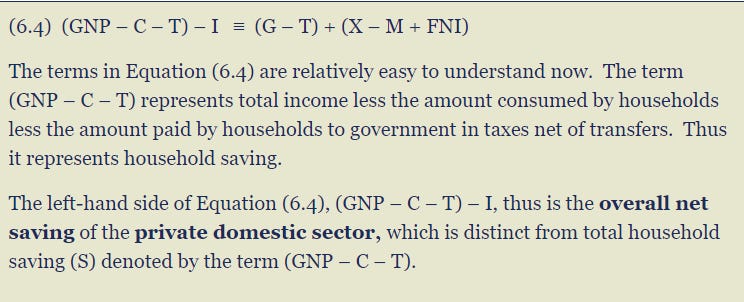

Sumner notes that MMT has a peculiar definition of saving:

As Sumner points out, this isn’t what economists typically think of as private saving. Normally, economists think that investment represents a form of saving. If a private company builds a factory, that’s investment. It can use that factory to make useful, valuable stuff next year, which the company can then sell. Spending money on building that factory therefore counts as saving, because you get money out later.

At least in the typical econ definition. In MMT, investment doesn’t count as part of net saving; it gets subtracted out. What’s left is just the amount that the private sector lends out to other sectors — government or foreigners.

That’s weird, because lending money to other sectors of the economy shouldn’t be the only way the private sector can save. Suppose the world was just one country (so, no foreigners). And suppose the government of this country didn’t borrow or lend at all (so, no government deficit). According to MMT, the private sector would be completely unable to save anything at all! But according to typical economics, the private sector would be able to save by investing for the future.

So, good. We’re starting to get an idea of where MMT diverges from traditional econ concepts.

But note that this difference is semantic. It’s definitional, not substantive. MMT people have taken the thing that economists typically call “private saving”, and subtracted investment, and relabeled the difference as “net private saving”. So what? Who cares? Instead of arguing about what constitutes “saving”, couldn’t we just find a new term for this new object? In fact, the sectoral balances framework, developed by Wynne Godley and others, defines “private sector surpluses” the exact same way that the MMT textbook defines “net private sector savings”. So who cares whether it’s called “surplus” or “saving”?

The answer, I think, is that MMT is engaged in a very different activity from traditional economic analysis. Traditional econ is trying to model and understand the economy. But MMT is engaged in policy advocacy — their goal is to make the government more willing to run deficits.

Math models aren’t very useful in this quest. Outside of a few elite circles, no one understands mathy macro models. And who listens to those few elites, especially after the debacle of the Great Recession? People are out there getting their policy ideas from Twitch streams, Twitter feeds, podcasts and subreddits. How much politicians care about deficits still partly depends on the nostrums whispered into their ears by respected policy advisors, but in a populist age, the passions of the masses might also matter a lot.

And in this arena, the MMT people are up against a deeply entrenched and powerful meme — the idea of government as a household. When a household runs up its credit cards instead of saving money, it gets poorer and poorer. So people tend to think that when the U.S. government runs up the national debt, America is getting poorer. Let’s call this the Austerity Meme.

In fact, the Austerity Meme is wrong — the country is not the same as the government. Most of the money that the U.S. government borrows is being lent by private citizens and companies. “National debt” doesn’t actually make the country poorer (except the fraction that’s borrowed from foreigners). Nor does national saving even correspond to material standards of living, which is probably what we should really care about.

So the MMT people are trying to make their own counter-meme. By telling people that private sector saving equals government deficits, they hope to create the popular perception that a country gets richer when the government borrows money. After all, a household gets rich by saving its money, right? So if the only way for the private sector to “save” is for the government to borrow, it means that government deficits are necessary to make us private citizens richer…right?

Of course, this MMT Meme doesn’t describe reality any more than the Austerity Meme. But it has one thing going for it, which is that Keynesianism really works. When the government spends money during a recession, it really does increase GDP. So if government borrowing goes along with increased government spending, living standards often do improve. That makes it kinda-sorta seem like the MMT meme is right — like government deficits somehow did make the country richer — even though it actually has nothing to do with the definitions that the MMT people are playing with here.

But in an age of populism, that might not matter. If macro policy is now driven by groups of poorly-informed internet randos throwing their backs into the fight, then repeating the mantra that “government deficits equal private sector savings” (or surpluses, or whatever) might be able to help get us the fiscal stimulus we need.

Of course, the question is whether, in doing so, the MMT Meme will also cause people to forget the importance of taxes. And what the consequences of that might be. In fact, one of the people who was instrumental in the creation of MMT was supply-side guru (and later Trump advisor) Art Laffer…But that’s a topic for another day.

Your bit about it being policy advocacy aligns with what I’ve seen from my friends who subscribe to the MMT ideas.

I’m all for getting medlock-pilled. But the idea that we can have everything we could ever want simply with “money printer go brrr” (a gross simplification) always struck me as, ridiculous.

This was a helpful explanation of MMT and a confirmation of my understanding of it without reading a book on the subject. Can you please do a part 2 and tell us why they support a federal job guarantee as the extension of their theory? Or is that pushed by just some of the MMT proponents? I never understood the connection.