Macroeconomic update: Soft landing in progress?

Disinflation finally arrives, the job market is strong, and we'll still probably see rate hikes.

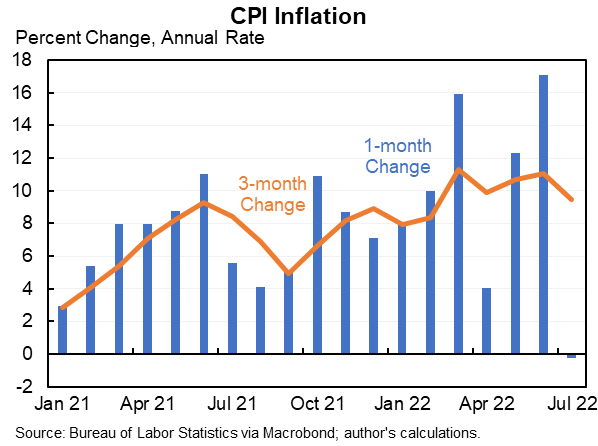

Well, folks, I have some good news. After some scary June numbers, disinflation finally looks like it has kicked in. Consumer prices as a whole increased 0% from June to July — nada, zilch, nothing — whereas before they had been increasing at an almost 16% annualized rate. Here’s what that looks like:

This is being driven by big declines in the price of gasoline, and smaller but still significant declines in the price of food. Those are very volatile commodities whose prices move in fits and starts. Core inflation, which omits these fast-changing items, also fell, but by a more modest amount:

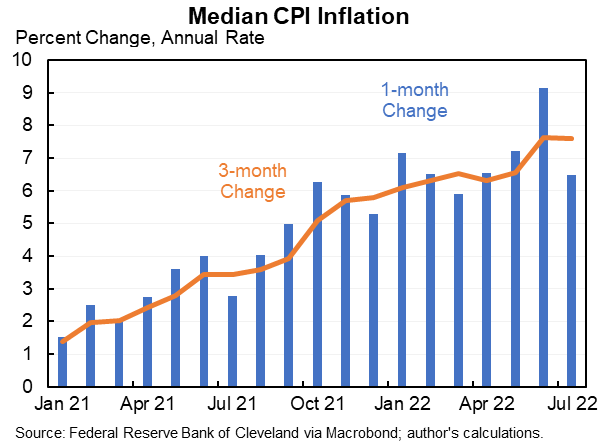

Now, this is great news — especially since it comes alongside a still-strong job market — but we shouldn’t over-extrapolate from one single month of data. Note that inflation dipped in summer 2021, causing people in “team transitory” to crow in victory, only to come roaring back at the end of the year. This time there are more reasons to think that disinflation is for real — Fed rate hikes, fiscal austerity, increased food and energy production in response to the Ukraine war, and supply chains that have recovered from the pandemic. But remember that inflation is incredibly hard to predict, and monthly data is extremely noisy. So don’t breathe a sigh of relief yet. Median inflation, which ignores the outlier items with big monthly price moves, decreased only a small amount:

The most obvious story here — and the one that we all want to be true — is the “soft landing” scenario, where the Fed has increased rates just enough to restrain price increases without causing noticeable damage to the real economy. I’ve said a number of times that I think this is the most likely scenario, but that doesn’t mean it’s in the bag.

The 0% inflation debate

One of the more entertaining aspects of this month’s data release is watching people argue over whether inflation has hit 0% or not. When I said that “everyone wants to see a soft landing”, I wasn’t being literal — in fact, some people are so brain-poisoned with politics that they actually want to see inflation continue just so they can complain about it. Thus, we saw certain people getting very very upset over the notion that inflation has halted:

In fact, Twitter itself bowed to this furor and added “context” to Joe Biden’s claim about 0% inflation:

So was July inflation 0% or 8.5%? It just depends on whether we are talking about month-over-month or year-over-year numbers. Let me explain those real quick.

Month-over-month inflation (or m/m) means how much prices change from one month to the next. Usually we express this as an annualized rate — the amount of annual inflation we’d experience if the month-over-month rate continued for a whole year. So if prices go up 1% between January and February, that’s a 12.7% annualized month-over-month rate of inflation.

Year-over-year inflation (or y/y) means how much prices have changed relative to one year ago. So if prices in February 2022 are 7.9% higher than prices in February 2021 were, that’s a 7.9% year-over-year rate of inflation.

Inflation numbers tend to bounce back and forth from month to month, which is why year-over-year tends to be a smoother measure of inflation. Here’s a picture of m/m inflation (blue) vs. y/y inflation (red). These are the exact same data, just presented two different ways:

The silly politicos who are screaming that 0% inflation is a lie are silly — it’s just one way of representing this month’s numbers. But there are two reasons that using the 0% number in isolation is over-optimistic.

First, as we see on the graph above, y/y inflation is more stable, so the blue line will likely bounce back somewhat in a month or two. Thus, focusing too much on the 0% m/m number will cause us to understate the danger that inflation still poses.

Second, some people reported y/y numbers when inflation was accelerating between January 2021 and June 2022, but now are reporting m/m numbers when inflation appears to be going down. This is probably because they consciously or unconsciously wanted to report whichever inflation number is lower, either to soothe their own fears or to make the Biden administration look better. This was misleading.

The best thing to do, in my opinion, is simply to report both m/m and y/y numbers if the two are very different from each other. Yes, that requires people to know what these numbers mean. But why report any numbers at all if you don’t expect people to know what they mean?

Are labor markets too hot?

A more substantive and interesting question is whether or not hot labor markets are exerting inflationary pressure on the economy. Besides slowing inflation, the other good piece of economic news this month was that the job market is still doing great — the economy added 528,000 jobs in July, which is very fast considering most Americans who want jobs already have them. Nominal wages are rising too, at somewhere north of 5%.

This has some economists worried that tight labor markets are going to keep pushing up on inflation:

This is the idea of a wage-price spiral — workers demand more pay, which leads them to spend more, which pushes up consumer prices, which spurs workers to demand more pay, and so on. Back in the old days, economists used to worry about this a lot, but in recent years they’ve been less worried. Empirical studies (which, to be fair, are always tricky when it comes to macro) just don’t find a lot of evidence for wage-price spiral effects.

It’s also kind of hard to imagine that wages are the main thing pushing up on inflation when wages have been lagging behind inflation until the most recent month. Here are average hourly earnings adjusted for headline CPI. You can see that they’ve been heading down since April 2020, and are now below their pre-pandemic levels (and far below the pre-pandemic trend):

Jason Furman, an economist I respect a lot, is worried nevertheless. He wrote a recent article at Project Syndicate entitled “America’s wage price persistence must be stopped”. He argues that even if wages are failing to keep pace with consumer prices, the fact that workers are getting raises is still exerting some amount of upward pressure on prices, and therefore the Fed must keep raising rates until wages stop growing.

But I am not convinced. Above and beyond the econometric evidence that wages are not a big contributor to modern inflations, focusing on curbing wage growth seems to misunderstand why inflation is bad in the first place.

Falling real wages are the main reason people are upset about inflation in the first place — since their pay can’t keep up with consumer price hikes, they’re seeing their purchasing power erode. We want to see real wages rise, not fall. If the Fed targets wages when setting interest rate policy, there’s the possibility that they’ll go too far — that they’ll keep pushing wages down even after consumer prices have already been tamed.

Instead, I think the prudent policy is to simply target consumer prices themselves, without thinking about wages. If taming inflation means that wage growth slows, so be it. But if we end up successfully restraining consumer prices even as wages continue to grow — as happened in the month of July — then that’s a win, both politically and in terms of the well-being of the American middle class.

The Fed’s next move

Which brings me to the final question: What will the Fed do in response to this July inflation number? Some people will call for rate hikes to cease. Having conquered inflation, they say, it would be foolish to risk causing a recession for no reason. But I predict that the Fed will keep raising rates, for two reasons.

First, the optimistic scenario — that inflation subsides fairly quickly — is already baked into the Fed’s promises, and into expectations. As John Cochrane explained in an excellent post back in April, if the Fed expected inflation to persist at around its current level, it would be raising interest rates — or promising to raise them — a lot more. A classic Taylor Rule, for example, would have interest rates at 8%! The fact that the Fed recently predicted that it will end up raising rates only to somewhere around 4% means that they expect inflation to go down.

But rates are currently only at 2.33%! Which means the Fed has maybe 150 basis points of hiking left to do just to fulfill the amount that it predicted it would have to do in order to quickly quell inflation. To let up earlier than they said they would, just because of a month of encouraging data, might sacrifice credibility and cause inflation to rebound.

(Note: This post initially stated that the federal funds rate was 1.68%. That was the July number; since then it has risen to 2.33%, due to a Fed rate hike.)

The second reason I don’t expect the Fed to stop hiking rates is that month-over-month inflation data, as we’ve discussed, tends to bounce back and forth quite a lot. And gas and food prices, which drove the July numbers, bounce around even more than other types of inflation. Pundits may be jumping to conclude that inflation is dead after one month of encouraging data, but the Fed will not. It will likely wait to stop firing until it no longer sees the whites of inflation’s eyes.

But anyway, we’ll get one more month of inflation data before the Fed makes its next move in late September. If prices continue to look like they did in July, I could see the Fed doing a smaller hike. But if prices bounce back, I’d expect them to stay the course they began earlier this year.

It seems like part of the problem is an assumption by some that fixing inflation means going back to 2020 price levels, rather than just bringing the rate of change down to managable levels. My understand is that that is both an unrealistic expectation, as CPI rarely falls in that way and, if it did happen, it would either indicate or cause major economic disaster (possibly both).

Fed funds is 2.25/2.5 right? Not 1.68?