Inflation is real; now it's up to the Fed

Biden's spending policies aren't going to affect inflation much one way or the other.

There are two different groups of people who go by the name of “Team Transitory”. First, and most prominently, there are the analysts who say that because inflation is purely due to transitory supply factors like supply chain snarls and post-pandemic shifts in demand, it will go away soon on its own and policymakers don’t need to worry about it. That version of Team Transitory is taking a serious shellacking. Core inflation — the most widely used measure of broad-based inflation — came in at 0.6% this month, which is a 7.4% annualized rate. This was the measure that led some people to claim that “Team Transitory won” when it briefly dipped down in September. Well, now it’s back up. Other measures that try to crop out outliers (so that the price of one or two things, e.g. used cars and computer chips, can’t affect the total) show the same acceleration:

So the Team Transitory that said to just wait and watch inflation go away on its own increasingly looks to have lost the argument; inflation might go away on its own, but if so it’s going to take a long, long time.

But there’s a second, more reasonable Team Transitory, which makes a slightly different prediction: Inflation will fall, but only because the Fed takes action to bring it down. Tyler Cowen is on this second team. And for right now, I am too — I think the Fed is not ready to give up its Volcker-Greenspan-Bernanke-Yellen reputation just yet.

In fact, it’s very important that the country as a whole agree with Tyler, because as long as people expect the Fed to tame inflation eventually, it won’t spiral out of control. But here there are some worrying signs. 5-year breakevens, which measure the market’s expectations of inflation over the next 5 years, are now rising rapidly, and are the highest they’ve been since we started measuring them two decades ago:

If this continues, it means people are starting to doubt the Fed’s commitment to restraining inflation. And this is the real danger, because that could cause a price-expectations spiral that would send inflation into double digits — and would eventually force the Fed to pull a Paul Volcker and throw millions of Americans out of work just to put the genie back in the bottle.

So that’s where we are right now, overall. Now on to a few more specific points:

Are we headed for hyperinflation?

Jack Dorsey certainly thinks we are:

But he’s probably just been talking to crypto friends who’ve been telling him this stuff in order to pump up the value of their Bitcoin portfolios. Some Bitcoiners have really run with the whole “digital gold” idea, and are trying to get people to view crypto as an inflation hedge. And if enough people start to think of it that way, then it really will be an inflation hedge. That’s why we’re seeing this talk of hyperinflation from people with lightning bolts in their screen names.

That said, however, it’s impossible to rule out actual hyperinflation. It would probably require a completely compliant Fed financing government spending with money creation. That doesn’t describe the Fed we currently have, but if, say, Donald Trump comes back into office and assumes quasi-dictatorial powers like Hugo Chavez did in Venezuela, then it’s possible we could see inflation spiral out of control. So watch out for that.

Is inflation being caused by Covid relief spending?

This is a tough one. In theory, deficit spending raises aggregate demand, which tends to be inflationary. We’ve done a lot of deficit spending for Covid relief, and people like Larry Summers and Jason Furman have been predicting that it would lead to inflation. The theory here is pretty simple, too — Covid relief put money in people’s pockets, and they spent that money, so prices went up. Thus, the recent inflation numbers may look like vindication for Summers, Furman, & co. Inflation is global, of course, but most countries did quite a bit of Covid relief spending.

Of course, we know another factor pushing up inflation, which is supply chain snarls. That’s a major negative shock to aggregate supply, which also tends to be inflationary. It’s hard to know which of these factors is contributing more to the inflation we’re seeing (in econ jargon, it depends on knowing the elasticities of the aggregate demand and aggregate supply curves, which are hard to estimate).

Some researchers claim that deficits caused inflation in certain historical episodes, but in general big deficits don’t seem to correlate with high inflation. Notably, Ronald Reagan pumped up deficits even as inflation fell, and Japan in the 1990s went on a huge deficit spending binge that failed to get them out of inflation. (A very interesting randomized controlled trial by Coibion, Gorodnichenko, and Weber found that learning about high current deficits doesn’t increase people’s stated expectations of inflation, but expected future deficits do.)

So the real answer here is that we don’t know how much Covid relief spending has contributed to the rise in inflation. Doubtless Republicans and some centrist Dems like Joe Manchin won’t wait for confirmation, and will use inflation as a reason to nix Biden’s spending plans, just as they used the inflation of the 1970s to call on Jimmy Carter to cut social spending. It may even work.

This would probably be a mistake. The Carter and Reagan eras, and Japan’s experience, show that monetary policy is far more effective at controlling inflation than fiscal policy — if the Fed is committed to restraining inflation, big deficits probably don’t do much. I certainly don’t think that the Build Back Better bill — which would spend a modest 0.83% of GDP as per the current proposal — is significant enough to have any noticeable effect on inflation one way or the other.

Inflation-fighting is a job for the Fed.

Build Back Better won’t tame inflation, but won’t increase it much either

In an attempt to get out in front of the inevitable Republican/Manchin attempts to kill Build Batter over inflation fears, the Biden administration is going around saying that the BBB bill (along with the infrastructure bill that already passed) would actually act against inflation:

This seems obviously false to me. The administration’s reasoning is that inflation is being caused by a supply crunch, and building things like infrastructure and housing will ease the supply crunch.

This is true in the long run, but the timing is just way off here. Building roads, bridges, houses, etc. takes several years, especially in America where construction moves at a glacial pace. (This was the experience with the American Recovery and Reinvestment Act a decade ago.) There’s no way this added supply will bring down inflation in any material way in the next 5 years.

Instead, Biden’s bills will increase demand for the materials needed to build housing and infrastructure. Those materials, many of which are subject to supply chain snarls, will go up in price, and this will probably be inflationary.

The administration’s final argument is that expanded child care provisions would allow more parents to go to work, thus increasing labor supply and pushing down inflation. But this only works if the increased labor supply pushes down wages, which then push down prices for other goods. That doesn’t sound like the best outcome. But it’s also pretty unrealistic. Rising wages are not a major cause of the current inflation — in fact, real wages are flat or falling, so labor is not really the bottleneck here. Moreover, getting more people into the workforce increases their income, which increases demand. So there’s just no way that expanded child care is going to tamp down prices.

To sum up, I expect Biden’s bills to push upward on inflation, rather than downward. That said, the inflationary impact will be very small — this is only 0.83% of GDP we’re talking about, at most. That is much much smaller than the Covid relief bills. An order of magnitude smaller. Really, the people on both sides trying to use inflation to support their desired fiscal policies are just playing politics here.

The Fed’s expectations management game

The Fed is in a dilemma here. Supply chain snarls represent a negative aggregate supply shock, sort of analogous to the oil shocks in the 1970s. The situation isn’t the same overall, of course — in the 70s we had stagflation, while right now we’re seeing booming demand from the pandemic recovery and from the relief bills. But there’s still a negative supply shock underneath it all, and negative supply shocks offer a central bank the option of two bad choices.

Choice 1: You can tighten monetary policy in an attempt to fight the inflation, but this will cause a recession and throw millions of Americans out of work.

Choice 2: You can loosen monetary policy in an attempt to cancel out the negative supply shock’s effect on the real economy, but this just makes the inflation worse.

In other words, no matter what the Fed does, it’ll make something worse. That argues in favor of doing nothing.

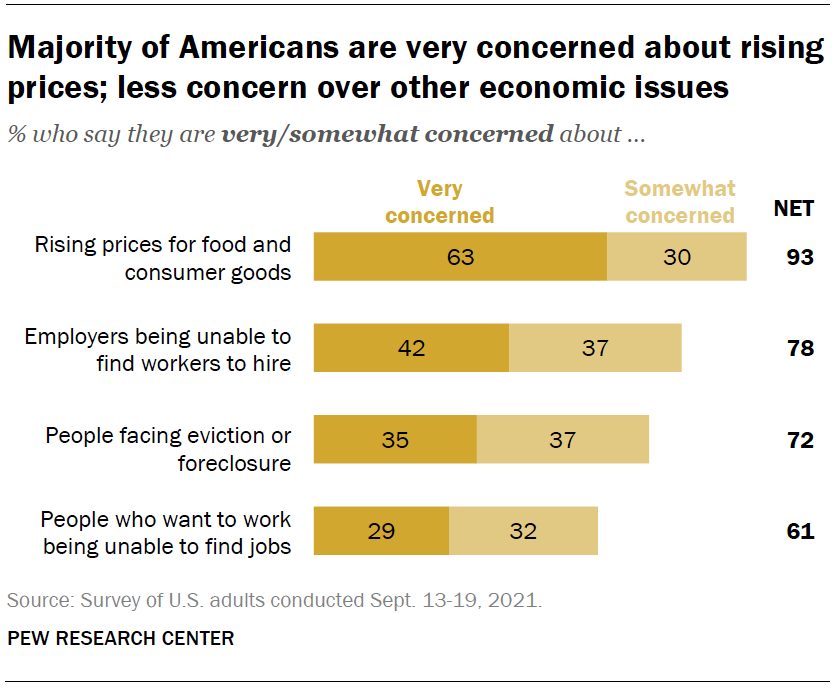

The big danger here, though, is that doing nothing might cause the country to decide that the Fed no longer cares much about fighting inflation. And then we could start to see the really really bad kind of inflation appear — an upward spiral of expectations and prices. That’s probably what happened in the 70s — what started out as just a negative supply shock (from oil) eventually turned into a spiral when the Fed ignored the supply shock for too long and people decided (probably correctly) that it wasn’t sufficiently anti-inflation. The rise in the 5-year breakeven rate, which I noted above, should make us more worried about this same thing happening now. Meanwhile, surveys show that the country is definitely starting to pay attention to the rise in consumer prices.

So the Fed needs to make sure this doesn’t happen, and that the public knows that they still care about inflation. That’s why the Fed is currently tapering its quantitative easing programs. Right now, it’s being cautious and trying to chart out a middle path — making sure everyone knows it’s willing to tighten, while not actually tightening so much that it endangers the economic recovery.

But if market inflation expectations keep rising, the Fed will probably have to do more. At that point, expect rate hikes, probably followed by a recession or at least a mild slowdown like in 2016. That will suck, and a lot of progressives will likely accuse the Fed of sabotaging Biden’s agenda and trying to get Republicans elected. But if inflation expectations spiral out of control, the alternative — doing nothing and allowing the spiral to continue — would be just as bad for Democrats and much worse for the country.

So keep a close eye on those 5-year breakevens. This could get hairy.

Good piece. A few thoughts:

1) It's never so easy as deficits do or don't cause inflation. Excess deficits + a central bank unwilling to tighten if necessary, cause inflation. As long as there is a credible central bank inflation should be very hard to get out of control. All eyes on the Fed.

2) If Republicans come into power in a big way over the next 3 years it's likely to be on an anti-inflation platform. I suspect todays' inflation will be highly unpopular with the electorate.

3) Jack is just spouting crypto nonsense. However, I do believe a changing mindset among the public would be an early step in inflation becoming a long-term problem. I don't take his words literally, but I take them seriously as an indicator of how opinions are shifting.

4) I fear price controls are going to make a comeback.

I think Noah is misunderstanding the transitory vs non-transitory.

Non-transitory inflation is caused by structural factors that sustain inflation. Transitory is not.

If inflation is not transferring into wages, it will necessarily go away. You can't have 4-6 percent inflation for long unless wages keep up. Wages are not keeping up, so inflation is not self-sustaining. https://fred.stlouisfed.org/graph/?g=ILOI