How much will beating inflation hurt American workers?

The question on a lot of people's minds.

Well, the Fed hiked rates again, as expected. The federal funds rate went up by 75 basis points (0.75%), to a target range of 3%-3.25%. Perhaps more importantly, the Fed has promised to hike more in the future. The “dot plot” — the central bankers’ own predictions of how much they’ll raise rates — now peaks at 4.6% in 2023, compared to 3.8% two months ago. Market expectations have gone up by slightly more — back in July the markets predicted that rates would peak at 3.5%, but that number is now 4.5%.

The reason for this, of course, is that inflation has stubbornly refused to fall. Though headline inflation has fallen thanks to drops in oil and gasoline prices, core inflation — the measure the Fed pays the most attention to — remained somewhere between 6% and 7%, whether measured month-over-month or year-over-year:

In some respects, even this latest hike means the Fed is still, to some degree, on “Team Transitory”. A classic Taylor Rule, which sets monetary policy based on current inflation, would probably have interest rates at 9% or higher. That’s a lot higher than the Fed’s current planned peak of 4.5%. The reason the Fed isn’t hiking that much is that they expect inflationary pressures — whether due to government spending, post-pandemic disruptions, or the war in Ukraine — to diminish somewhat on their own.

This may still happen. Oil and gas prices have fallen, reducing one major cost for businesses. That should eventually work its way through to lower consumer prices. And people are slowly working through their pent-up savings from the pandemic. Nor are government deficits at anywhere near where they were in 2021 and 2020. It may be that these external shifts allow the Fed to get away with only hiking to 4.5% instead of to 9% or more. That’s consistent with surveys of inflation expectations, which now show inflation going back to the normal range in 3 years:

But there’s a chance this won’t happen — it certainly hasn’t happened yet. And if it doesn’t, expect the Fed to keep hiking, for fear of losing its inflation-fighting credibility. This is an optimistic Fed, but not a dovish one.

The question not on everyone’s mind is: How much will this hurt the economy? Eventually, higher rates will curb economic activity, and then people will start to lose their jobs. The Fed is prepared for this, and you should be too. A lot of people are quite nervous, wondering how much pain we’re in for over the next three years or so. So I thought I’d go over some of the aspects of that debate.

Does beating inflation mean bringing down wages?

One big question on a lot of people’s minds is whether tight labor markets are driving inflation. Basically the idea here is that when companies want to hire more workers than are available, they bid up wages. When wages go up, companies’ labor costs go up (forcing them to raise prices), and workers’ buying power goes up (making them willing to pay higher prices), and as a result, consumer prices go up. The most extreme version of this is the hypothetical wage-price spiral, where wages and consumer prices just keep driving each other higher.

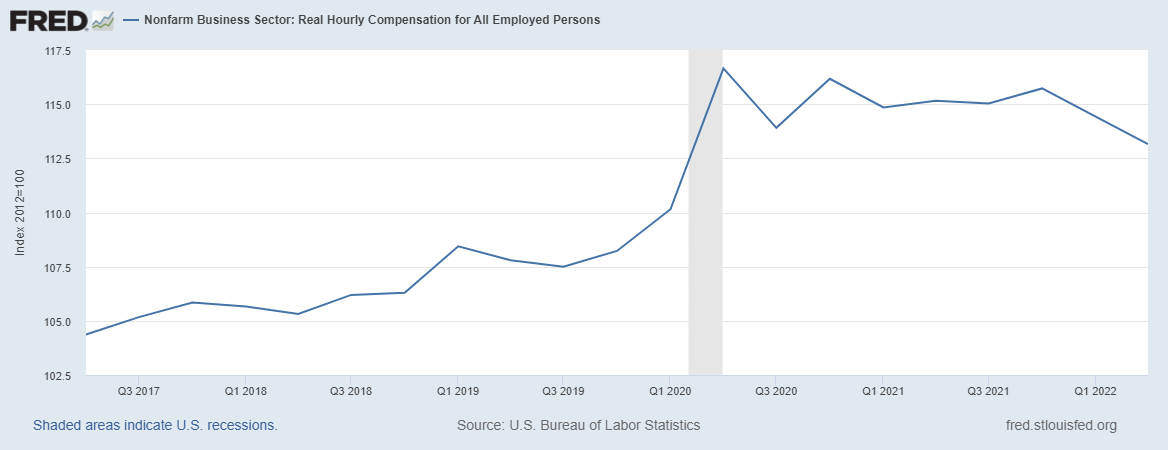

Personally, it’s hard for me to believe that anything like that is happening right now. Real wages aren’t even going up — they’re going down, as consumer prices outpace wage gains.

If prices are rising faster than wages, it means two things. First, it means that workers are feeling squeezed, as they experience a decrease in their real purchasing power. Every month they go to pay rent or buy groceries or shop for new cars or whatever, and the prices are higher relative to their paychecks. They’re demanding raises, but the raises aren’t keeping up with the prices. In that sort of environment, it seems odd that people would be in a frenzied buying mood. Second, falling real compensation means that companies’ labor costs — at least, per worker — are falling relative to the prices they charge for their products. That doesn’t sound like an environment where companies feel like they have to keep hiking prices just to stay ahead of costs.

On top of that, though the headline employment rate is low, the economy keeps adding tons of jobs. Nor does this appear to be a statistical artifact; my favorite measure of the labor market, the prime-age employment-to-population ratio, rose in both July and August:

You’d think if the labor market were really tight, we’d see employment top out and real wages go up, as employers bid higher and higher for a fixed pool of workers. But instead we see real wages failing to keep pace with inflation, as companies continue to successfully find more and more workers to hire. To me, that doesn’t look like wages are a big driver of inflation right now.

But this is apparently not quite how Powell and the Fed see things. In his recent remarks, Powell said that the labor market is tight and that wages will need to come down:

Now, Powell did say that prices coming down is even more important than wages coming down. But it’s clear he thinks the labor market is one of the culprits behind high inflation.

Some economists are even more insistent that wages are at the center of the inflation puzzle. For example, here’s Jason Furman in Project Syndicate from early August:

At this stage, inflation is increasingly embedded in price growth, which is fueling wage growth that is in turn fueling price growth. This worrisome process – some call it a “wage-price spiral,” but I prefer “wage-price persistence” – is underwritten by short-term inflation expectations, which have risen markedly…

The latest data show that private wages and salaries grew at a 5.7% annual rate in the first half of this year, which is about 2.5 percentage points faster than the pace of growth prior to the pandemic. All told, adding 2.5 percentage points to the pre-COVID inflation rate implies an underlying inflation rate of 4.5%. Moreover, a range of alternative measures of wage growth are consistent with the same or even higher inflation, according to estimates by Alex Domash of the Harvard Kennedy School…

Unfortunately, the only solution to wage-price persistence is to restrain demand.

Now, Jason Furman is an economist I both like and respect. But to be perfectly honest, I’m still just not quite sure I buy this story. Jason says that rising nominal (dollar) wages are “adding 2.5 percentage points” to inflation. That implies that if other inflationary pressures went away, those 2.5 percentage points would still be chugging along. But in another spot he says that inflation expectations are driving wage increases. If that’s true, it implies that if other inflationary pressures went away, workers would moderate their wage demands.

In general, my view is that macroeconomists tend to focus too much on wages as a driver of inflation. This is baked into lots of economic models, and so it surprised veteran model-maker Olivier Blanchard when this current bout of inflation manifested in prices more than wages:

But I’m not sure why this was so surprising; in the 70s, too, wages fell behind as prices zoomed ahead.

So I still don’t think that getting workers to moderate their wage demands is really the key to solving this bout of inflation. In fact, I think if we can beat inflation with rate hikes, we can get back to a situation where real wages are rising, as they did in the late 2010s. And that will be a good thing. The people who think wages are the culprit here will have to work a little harder to convince me.

That doesn’t mean, however, that workers will come through a bout of disinflation unscathed. Even if real wages don’t take a hit, employment almost certainly will.

How much will unemployment have to rise?

The question of how many Americans will have to lose their jobs in order to get inflation back down to 2% is a very important one. In economics there’s a term for this grim number: the “sacrifice ratio”. Usually the sacrifice ratio is expressed as the amount of economic output (GDP growth) that we have to give up in order to reduce inflation, but since there’s usually a pretty tight correlation between growth and employment, it amounts to basically the same thing.

The sacrifice ratio is something that’s easy to name but hard to estimate. The reason is that you can’t just look at the data here — correlation isn’t causation — so you need a model of the macroeconomy in order to tell you the cost of bringing down inflation. And macroeconomic models are notoriously based on dodgy assumptions. For this reason, estimates of the sacrifice ratio are extremely sensitive to which set of dodgy assumptions you decide to make. Fed economist J. Benson Durham pointed this out in a 2001 paper, and other attempts to estimate the ratio have also been frustrated.

It’s also probably true that the sacrifice ratio isn’t set in stone — it depends on how the Fed carries out the disinflation. In the 90s, Lawrence Ball looked at disinflations in OECD countries and found that the faster inflation came down, the less unemployment went up. In other words, if we just get it over with and clobber inflation now, the pain might be less. But Mazumder (2014) argued that when you look at core inflation rather than headline, this conclusion goes away.

It also depends on what’s causing the inflation. If inflation is caused by supply shocks, the pain might be greater. But almost two years into the current bout of inflation, there’s still no consensus on how much supply shocks matter. Certainly there seemed to be a spike in both inflation and inflation expectations when the Ukraine War and the Russia sanctions hit, but the inflation started much earlier than that. And falling oil prices and falling freight prices and the end of supply chain snarls haven’t brought down core inflation yet. So it’s still a very open question how much supply shocks play a role here.

Another crucial question is the role of expectations. Ricardo Reis had a good thread recently about how this factors into the equation. As Ball, Leigh and Mishra (2022) point out, the more that expectations are adaptive — in other words, the more that high inflation makes people used to high inflation — the more painful it’ll be to bring it down again. Essentially, in that world, the Fed has to basically clobber people over the head with a terrible economy to get them to wake up and realize that inflation isn’t going to be high anymore.

But Reis argues that we shouldn’t be so pessimistic, because people look ahead to the future instead of just assuming that tomorrow will be just like today. And his argument is persuasive, since inflation expectations — whether measured by surveys or by markets — are coming down, even though there hasn’t been a recession yet. So that’s good news.

In any case, though, the upshot here is that the sacrifice ratio is really hard to know. That’s not surprising — the more you dive into macroeconomic debates, the more you realize that “we don’t really know, but we have to make a policy decision anyway” is pretty much always the conclusion.

So let’s just throw in some numbers here. The Fed, for their part, is forecasting that headline unemployment will rise to 4.4% (from a current 3.7%) as a result of planned rate hikes. I don’t really know where they get that number — probably some internal model with a ton of dodgy assumptions — but it’s pretty significant. That would mean about 1.5 million Americans out of work. If rates have to double to 9%, it would mean a lot higher unemployment — maybe 3 million Americans out of work compared to today?

1.5 million is a big number, and 3 million is a very big number — one-sixth and one-third, respectively, of the number of Americans who lost their jobs in the Great Recession. Understandably that has many people worried. And the most worried people are progressives:

But in my view, progressives are too worried about unemployment and not worried enough about inflation. It’s very hard for government to alleviate the burden of inflation — after all, handing out cash so people can afford higher prices just makes the situation worse, since it pushes prices up even more. It’s far easier to alleviate at least the burden of unemployment, through programs like extended unemployment insurance, plus other safety net programs. That doesn’t mean unemployment isn’t bad — government relief efforts can’t fully make up for the loss of a job — but it does mean that unemployment, as opposed to inflation, is a problem we can at least ameliorate. On top of that, continued or rising inflation could threaten the Democratic party, the progressive political project, and — via the return of Trump — the stability of our country itself.

So while throwing 1.5 million or even 3 million Americans out of work sounds heartless and horrible, so is condemning hundreds of millions of Americans to watching their living standards steadily fall. The facts of economics often compel policymakers to make grim tradeoffs that will inevitably result in some group of people getting hurt — that’s a sad fact of life, but we can’t just wish it away. The best we can do is to use targeted policies to help the people who get the short end of the stick.

And who knows, maybe the Fed is being pessimistic, and inflation can be restrained with less economic damage than they think. Fingers crossed.

I think it's important to push back against this idea:

"people are slowly working through their pent-up savings from the pandemic"

The last one ($1,400) was 18 months ago. Really??

https://twitter.com/asymptosis/status/1537461695903281152/photo/1

Thread: https://twitter.com/asymptosis/status/1537461695903281152

Yep wages are NOT to blame for the current high inflation in the US. Instead, the current high inflation is the price being paid for the extreme increase in the money supply (driven by enormous federal government deficits and the monetisation of those deficits by the Fed).

Wages are simply desperately trying to play catch up, but as is often the case during periods of high inflation, the working class, and those who can least afford it, are increasingly falling further and further behind. It's a real extra kick in the guts to these people that so many economists and policymakers are effectively using them as a scapegoat for their own failures in fiscal and monetary policy.

Though with the Fed tightening as aggressively as it has, inflation will come down, and is already showing significant signs of doing so. Most importantly the Fed doesn't need to keep raising rates. Current monetary policy settings have already resulted in the M2 money supply flatlining - the hard work has already been done. Durables prices peaked in February, have fallen significantly since, and are set to decelerate further on a YoY basis from October. Oil prices continue to roll over, which will continue to see the nondurables category decelerate. The main issue with inflation as measured by the CPI are shelter costs. Though again, there is reason for optimism here, as market based measures of rents have decelerated in recent months, and during August, were below the rate of growth being recorded by the CPI. Unfortunately the CPI (as well as the PCEPI), measures rental costs with a SIGNIFICANT lag, raising the risk of the CPI overstating inflation and the Fed overtightening. Though on an underlying basis, everything is pointing to a material decline in inflation over the next year - the bigger concern is will the Fed unnecessarily tip the economy into a severe recession by excessively tightening monetary policy, a scenario which I think is quite possible.