Five possible reasons why China's productivity slowed down

And why speeding it back up will be difficult

It’s always an interesting experience to read books about China’s economy from before 2018 or so. So many world-shaking events have changed the story since then — Trump’s trade war, Covid, Xi’s industrial crackdowns, the real estate bust, lockdowns, Russia’s invasion of Ukraine. Reading predictions of China’s evolution from before these events occurred is a little like reading sci-fi from 1962.

When I started China's Economy: What Everyone Needs to Know®, by the veteran economic consultant Arthur Kroeber, I was prepared for this surreal effect. After all, it was published in April 2016 — not the most opportune timing. So I was pleasantly surprised by how relevant the book still felt. Most of the book’s explanations of aspects of the Chinese economy — fiscal federalism, urbanization and real estate construction, corruption, Chinese firms’ position within the supply chain, etc. — are either still highly relevant, or provide important explanations of what Xi’s policies were reacting against. Dan Wang was not wrong to recommend that I read it.

But China’s Economy is still a book from 2016, and through it all runs a strain of stubborn optimism that seems a lot less justifiable six years later. Most crucially, while Kroeber acknowledged many of China’s economic challenges — an unsustainable pace of real estate construction, low efficiency of capital, an imbalance between investment and consumption, and so on — he argued that China would eventually overcome these challenges by shifting from an extensive growth model based on resource mobilization to one based on greater efficiency and productivity improvements. This was despite his acknowledgement of the fact that productivity growth had already slowed well before 2016, and that Xi’s policies so far didn’t seem up to the challenge of reviving it.

In many ways, productivity growth is the thread that ties together the entire story of the Chinese economy since 2008. Basic economic theory says that eventually the growth benefits of capital accumulation hit a wall, and you have to improve technology and/or efficiency to keep growth going. Some countries, like Japan, South Korea, Singapore, and Taiwan, have done this successfully, and are now rich; other, like Thailand, failed to do it and are now languishing at the middle income level. For several decades, Chinese productivity growth looked like Japan’s or Korea’s did. But slightly before Xi came to power, it downshifted to look a bit more like Thailand. Here’s a graph from the Lowy Institute’s recent report:

In fact, the Lowy Institute’s numbers are more optimistic than some other sources. The Penn World Tables has China’s total factor productivity growth at around 0 or negative since 2011:

And the Conference Board agrees.

Personally, I suspect these sources probably underestimate TFP growth (for all countries, not just for China). But even Lowy’s more reasonable numbers show a huge deceleration in the 2010s. If this productivity slump persists, it will be very difficult for China to grow itself out of its problems — such as its giant mountain of debt — in the next two decades.

The question then becomes: Why has Chinese productivity growth slowed to a crawl? There are several main candidate explanations, and they have important implications for whether Xi will turn things around.

The first reason, of course, is that China had several tailwinds that were helping them become more productive, and these are mostly gone now.

Reason 1: Hitting natural limits

One thing helping Chinese productivity growth was simply their distance from the technological frontier. When you don’t even know how to do fairly simply industrial processes, it’s pretty easy to learn these quickly. China imported basic foreign technology by insisting that foreign companies set up local joint ventures when they invest in China, by sending students overseas to learn in rich countries, by reverse-engineering developed-country products, by acquiring foreign companies, etc. Also by industrial espionage, of course, but there are lots of above-board ways to absorb foreign technology too.

The problem is, this has limits. As you reach the frontier, the remaining technologies you need to absorb to keep growing productivity quickly become more and more complicated — not the kind of thing you can easily learn from looking at blueprints or taking a class. Companies guard these higher-level secret-sauce technologies much more carefully. A case in point is that China has had trouble building its own fighter jets, because the metallurgy to build the specialized jet engines that make modern top-of-the-line fighters possible is only known to a few companies in a few countries. So over time, the ability to absorb foreign technology peters out and it becomes necessary to start inventing your own stuff.

A second tailwind was demographics. Everyone (including Kroeber) talks about China’s unusually large demographic dividend in terms of labor input — when you have a ton of young people with few elders or kids to take care of, they can go work a lot — but it’s also probably a factor in productivity. Maestas, Mullen & Powell (2016) shows a negative relationship between population age and productivity at the U.S. state level, while Ozimek, DeAntonio & Zandi (2018) find that the same is true at the firm level. The mechanism is unknown, but the pattern is pretty robust. In any case, China began to age rapidly rapidly right around 2010, when its working-age population peaked as a percentage of the total (and peaked in absolute terms shortly afterward):

A third tailwind for productivity was rapid urbanization. As Arthur Lewis famously noted, simply moving people from low-productivity agricultural work to high-productivity urban manufacturing work raises productivity a lot. Agglomeration economies are another force by which urbanization raises productivity. And economists find that China hit its “Lewis turning point” — i.e. ran out of surplus agricultural laborers to move to the cities — right around 2010. Of course, China also limited urbanization unnecessarily by using its hukou (household registration) system to keep migrant laborers from settling permanently in cities. But in any case, this tailwind also appears to be over.

So in the last decade, three big tailwinds that were driving Chinese productivity growth probably dried up. And there’s not really anything that Xi Jinping or any leader can do about that. But there are probably other factors dragging down China’s productivity growth as well, that might be more amenable to policy fixes.

Reason 2: Low research productivity

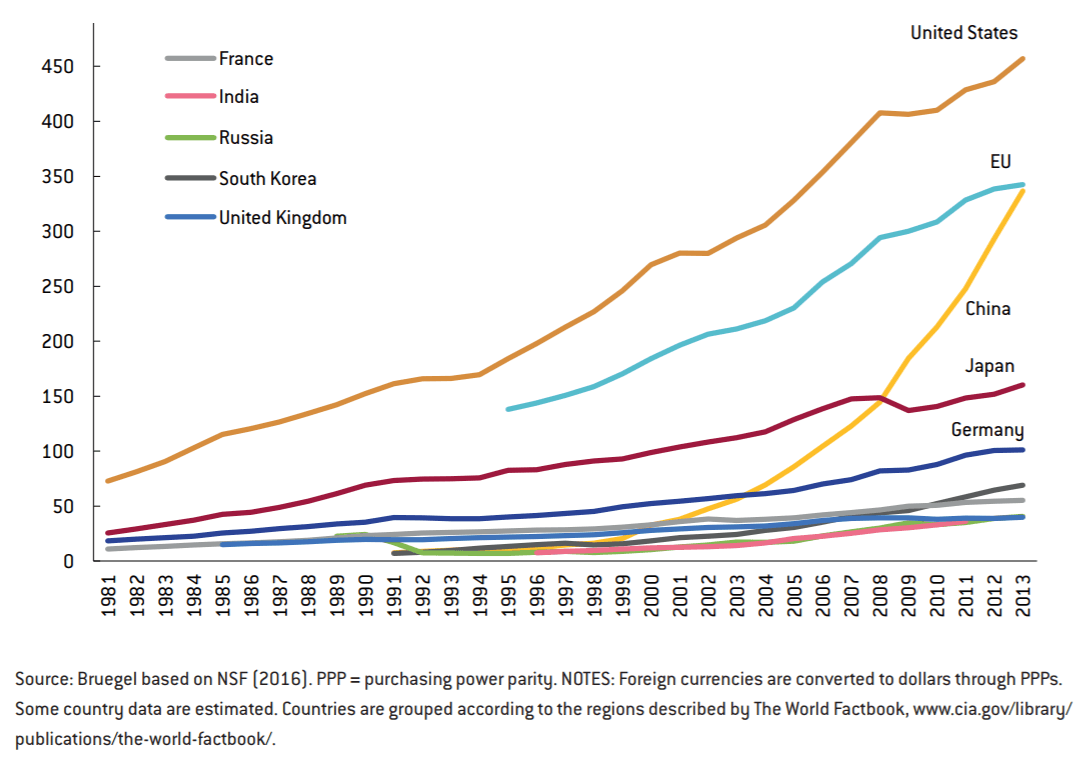

If you can no longer import foreign technology, one thing you can do is to invent your own. In fact, this is a good thing to do even if you do import foreign technology, since companies should create new products and new markets instead of just aping foreign stuff. And indeed, China has been spending a lot more on research and development in recent years. Here’s a chart from the blog Bruegel:

Unfortunately, research input doesn’t always lead to research output. A 2018 study by Zhang, Zhang & Zhao finds that Chinese state-owned companies have much lower R&D productivity than Chinese private companies, which in turn have much lower productivity than foreign-owned companies. And a 2021 paper by König et al. finds that while R&D spending by Chinese companies does appear to raise TFP growth, the effect is quite modest:

The authors suggest misallocation of resources as a major culprit in low R&D productivity — in other words, a lot of this spending is being done by state-owned companies that are just throwing money at “research” because the government tells them to, but not really discovering much. They also note that some companies simply reclassify normal investment as “R&D” in order to take advantage of tax breaks (note that companies do this everywhere).

What about university research? This is an extremely important part of how the U.S. keeps its technological edge. And China has indeed been throwing huge amounts of money at university research, such that its expenditure now nearly rivals that of the U.S. China recently passed the U.S. in terms of published scientific papers, including highly cited papers.

But the quality of this research has been called into question. Investigations regularly find that despite all this publication activity and all this spending, Chinese universities are not the leaders in most fields of research. Basically, the story is that Chinese scientists are under tremendous pressure to publish a ton of crappy papers, which all cite each other, raising citation counts. In the words of Scientific American, this has led to “the proliferation of research malpractice, including plagiarism, nepotism, misrepresentation and falsification of records, bribery, conspiracy and collusion”.

So the low productivity of Chinese R&D may help explain why the country’s domestic innovation hasn’t risen to take the place of foreign technology absorption.

Reason 3: Limited export markets

As everyone who reads this blog knows, I’m a big fan of the development theories of Joe Studwell and Ha-Joon Chang. A pillar of the Chang-Studwell model is the idea of “export discipline”. Basically, when companies venture out into global markets, they encounter tougher competition and also ideas for new products, new customers, and new technologies. This raises their incentive (and their ability) to import more foreign technology, and in general makes them more productive and innovative.

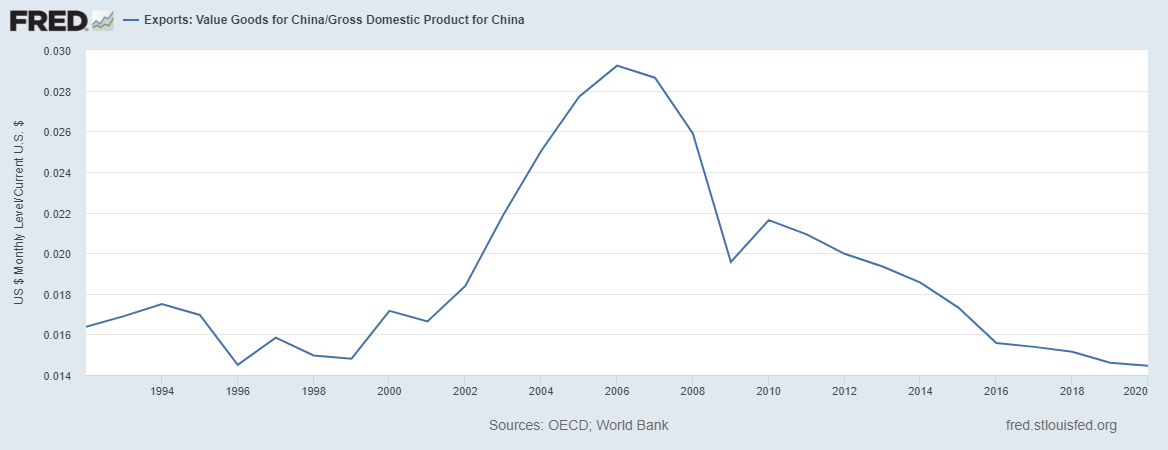

After the global financial crisis of 2008 and the recession that followed, the U.S. wasn’t able to absorb an ever-expanding amount of imports from China. So Chinese exports to the U.S. market slowed in the 2010s, and then Trump’s trade war slowed them even more. China’s exports to the EU rose a bit, but not that much. Developed-country markets simply became saturated with Chinese goods, and there wasn’t much more room for expansion. Developing countries are buying somewhat more Chinese goods, but they simply don’t have the purchasing power of the rich countries. So China’s exports as a share of GDP has actually fallen quite a bit since the mid-2000s:

Many people (including Kroeber) talk about this as a shift from export-led growth to growth led by domestic investment. And so it is. But if productivity benefits from exporting, then this is also a challenge for long-term growth, because there’s less opportunity for export discipline to work its magic.

In fact, this might be one reason that it’s harder for big countries to grow relative to small countries. It’s a lot harder to be an export-led economy when you have 1.4 billion people than when you only have 50 million people (as South Korea does), because the world simply gets saturated with your exports. Which raises the question of why the U.S. manages to be so productive — more productive even than most European and rich East Asian economies. Consumption might have something to do with that.

Reason 4: Not enough consumption

The U.S. is a very large economy that is geographically distant from most other major economies. This explains why the U.S. has a very low amount of trade relative to GDP — just 23%, compared to 81% for Germany and 69% for South Korea. But the U.S. is also a highly productive economy, more productive than all but a few small rich nations. Exports certainly helped the U.S. grow, but to a large extent it simply sold stuff to itself.

As the chart above shows, China increasingly does the same. But unlike the U.S., China’s domestic economy is heavily weighted towards investment in capital goods — apartment buildings, highways, trains, and so on. China’s final consumption is only 54% of GDP, compared to over 80% in the U.S. And private household consumption accounts for only 39% of China’s GDP, compared with 67% in the U.S. Of course, China is still at an earlier stage of development, but as Kroeber notes in his book, even countries like Japan and South Korea had significantly higher consumption shares at equivalent stages of their own growth stories.

Usually this gets discussed in the context of “imbalances”. But what if it also affects productivity? Consumers have a preference for differentiated goods that spurs companies to develop new products, increase quality, offer new features, and so on. The strategy professor Michael Porter argues that when companies compete by differentiating their products instead of simply competing on costs, it results in higher value added — in other words, it makes them more productive.

Over the past decade, China has been building a lot of buildings and a lot of infrastructure. But it hasn’t been developing a lot of innovative and high-quality cutting-edge consumer products. Various government policies that funnel resources toward domestic investment rather than domestic consumption may inadvertently be holding back Chinese productivity.

And the biggest such policy might be macroeconomic stabilization.

Reason 5: Macroeconomic stabilization

It’s important to stabilize the economy. Recessions throw people out of work and create tons of suffering, and probably also lead to underinvestment by companies. They can damage the cohesion of entire societies. The U.S. rediscovered this lesson the hard way in 2008-11, when our insufficient fiscal stimulus resulted in a recession that was longer and more painful than it had to be.

But there may be such a thing as too much stabilization. As I explained in a post last September, China avoided going into recession both in 2008-11 and again in 2015-16 (after a big stock market crash) by pumping money into real estate, via lending by state-controlled banks, often to SOEs and to local governments.

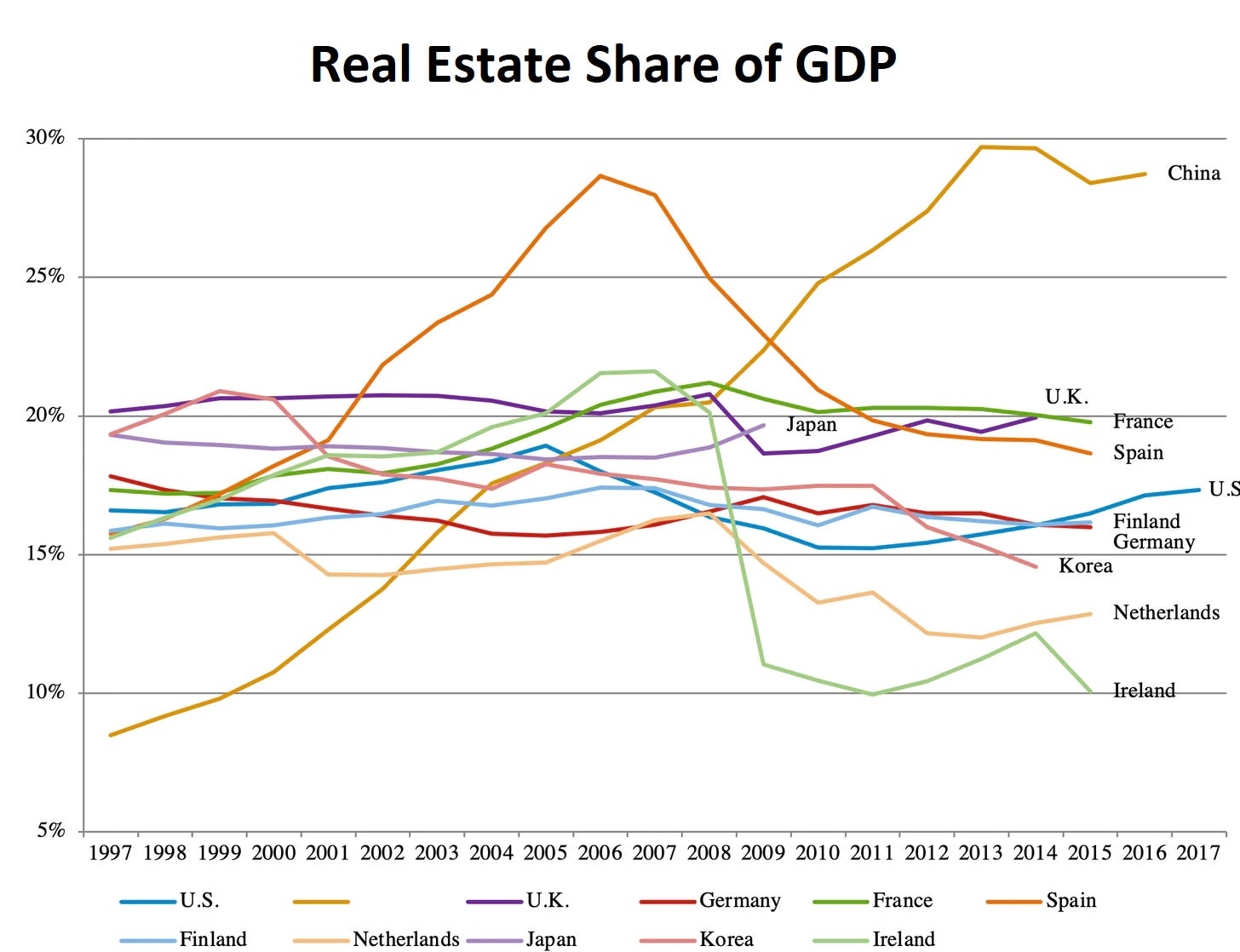

This likely saved the Chinese economy from experiencing recessions in 2008-11 and 2015-16. But it had a big negative effect on productivity growth, for three reasons. First, SOEs simply aren’t very productive compared to other Chinese companies. Second, the money was shoveled out the door very quickly, meaning that there wasn’t much time or incentive to figure out which projects were worth investing in. And third, real estate and construction are sectors of the economy with notoriously low rates of productivity growth. This last is probably the scariest, as it led China’s economy to be more dependent on real estate than any other in recent memory:

Anyone who has followed the saga of China’s Covid lockdowns will sense a familiar pattern here. The Chinese government, eager to preserve the appearance of invincibility, often goes overboard in unleashing the tools of control. But while recessions are not healthy things, the lengths to which Chinese policymakers went to make absolutely 100% sure they never had even the slightest recession may have left their economy with a huge hangover of low-productivity industry.

Will Xi bring back productivity growth?

So there are plenty of reasons why China’s productivity growth crashed to a low level in the 2010s and 2020s. But speeding it back up again — which every analyst, including Kroeber, seems to recommend — will be no easy task. The tailwinds driving productivity higher are gone. And China’s misallocation of resources toward low-quality research and low-quality real estate industries will not be easy to reverse; these systems have a way of getting entrenched.

Xi Jinping, of course, is going to try. Part of his effort consists of industrial policy — the Made in China 2025 initiative and the big push for a domestic semiconductor industry. It remains to be seen whether those will bear fruit.

But in the last three years, Xi has undertaken a second, more destructive effort to reshape China’s industrial landscape. Instead of simply boosting the industries he wants, he has attacked the industries he doesn’t want. He has cracked down on consumer internet companies, finance companies, video games and entertainment. And he has attempted to curtail the size of the real estate industry, resulting in a slow-motion crash that’s still ongoing.

Essentially, Xi is trying to crush industries he doesn’t like, in the hopes that resources — talent and capital — flow to the industries he does like. This is a new kind of industrial policy — instead of “picking winners”, Xi is stomping losers. One of the saddest things about optimistic 2016-era analyses like Kroeber’s is how much hope they place in internet companies like Alibaba, Tencent, and Baidu as heralds of a new, more innovative China. Xi has declared that these companies are not, in fact, the future.

But it’s far from clear that an economy works like a tube of toothpaste, where smashing one end will send resources squirting out the other end. If you’re a budding entrepreneur, do you really think that starting a semiconductor company instead of an internet company will win you Emperor Xi’s favor? What if next week he decides that he doesn’t need more chip companies, and that your company isn’t one of his preferred champions? What if after you get rich and successful, Xi decides you’re a potential rival and appropriates your fortune?

An economy where the leader is always smashing companies and industries he doesn’t like is inherently an economy full of risk. Yes, Chinese engineers and managers will obey Xi’s will and go into the industries he wants them to go into. But the loss of entrepreneurship and initiative might make this a pyrrhic victory.

In other words, escaping China’s low-productivity-growth trap is going to be tough, and Xi’s strategy doesn’t fill me with a ton of confidence so far.

This has impact on the US and global economy as well, as China is no longer "exporting deflation" as it did throughout the first two decades of the 2000s.

I do not understand why the Chinese government would throw away its succession policy (critical for long- term stability) for someone with Xi’s record. It’s all cost with no apparent gain.