Does China have hidden reservoirs of growth potential?

I'm not so sure.

Within the last year, I’ve noticed a distinct souring on the topic of China’s growth prospects among the commentariat. This makes sense, of course. Between seemingly never-ending Covid lockdowns, a protracted crash in the vast real estate sector, Xi’s weird crackdown on internet companies, and the fear of Russia-like sanctions in the event of a conflict, there are now a lot more reasons to worry that China’s amazing catch-up growth story is drawing to an end. In fact, these new stumbles come on the heels of longer-term trends that have relentlessly pushed down China’s growth prospects — slowing productivity growth, reduced opportunities for copying Western technology, and rapidly aging demographics.

This is obviously an important question for multinational companies who are thinking about curbing or even abandoning their investments in China:

China witnessed $17.5 billion worth of portfolio outflows last month, an all-time high, according to most recent data from the Institute of International Finance (IIF). The US-based trade association called this capital flight by overseas investors "unprecedented," especially as there were no similar outflows from other emerging markets during this period. The outflows included $11.2 billion in bonds, while the rest were equities.

With so many reasons to leave, why stay? The answer is: Sheer market size. The most important reason to be invested in China switched long ago from cheap labor costs to market access. Even if the Chinese government takes various steps to limit foreign companies’ market access and support home-grown competitors, even a tiny sliver of a billion consumers equals vast riches. So obviously, the question of whether the Chinese market will continue to grow is an important factor for investors.

Despite the darkening outlook on the China growth question, pockets of optimism remain. Some of these come from the people I call “obligate longs” — people whose job it is, in essence, to reassure Western businesspeople that investing in China is safe and attractive. But some optimism comes from less directly interested parties — for example, from my fellow Substack blogger Adam Tooze, and from Bert Hofman of the National University of Singapore.

Demographics

One of their main arguments is that China’s demographic crisis is not nearly as severe as people think. For example, here is a slide from Hofman’s talk showing that if China were to simply raise its retirement age to 65, its labor woes would essentially vanish:

Currently, China’s retirement age is 60 for most men and even lower for most women. That’s obviously far below developed-country standards. Could simply keeping old folks in the labor force solve the demographic decline?

Color me very skeptical. Here are the UN’s projections for China’s population age 15-64:

There are a few scenarios where the working-age population recovers, but A) Chinese demographic numbers have tended to surprise on the downside, and B) all of the scenarios agree on a big drop between now and 2060. So the envelope of how many people China can put to work is shrinking. The question is whether China can boost the number of people within that age range who do work. Yes, if there are a bunch of 61-year-old retirees kicking up their heels and watching TV at home while collecting pensions, you might be able to take away their pensions and make them go back to work.

But having seen firsthand the effects of forced early retirement in Japan (where the retirement age was 60 for many workers for a long time), I’m skeptical that a lot of these 61-year-olds are actually retired. Many of them probably go to work at much more low-paying jobs after being forced to quit their career job. They’re still in the labor force, they’re just not earning nearly as much. So the labor force bump from Hofman’s projection might be illusory.

It still might be true, of course, that keeping those folks in their career jobs for a few years longer will raise national productivity by a substantial amount. Old workers certainly have a big accumulated stock of knowledge about the companies and industries where they’ve worked for decades. But as Adam Ozimek suggested in a recent presentation, it’s also possible that doing this will cause Chinese companies to ossify — top-heavy with older management, these companies might fail to embrace new technologies and new business models. Ozimek’s own research shows a negative correlation between population aging and productivity:

And Ozimek also finds that companies with a greater share of older workers have lower productivity, and that when more older workers retire from those companies, they tend to have higher productivity.

In other words, productivity probably peaks at some point in a worker’s life. So keeping elderly managers in the top spots in China’s companies might not be the best idea for growth, whatever the official labor force numbers say.

Conversely, there’s the question of how many young workers China has. And we see that this number has already fallen by quite a lot:

If fertility continues to shrink, this will fall even more.

So to sum up, China’s demographics probably are just as much of a headwind as everyone thinks they are.

Nor will further urbanization ride to the rescue here. Officially, China has only a 64.7% urbanization rate, compared to over 80% in the U.S. You might think, therefore, that China has plenty of room to move people from farms to cities. But in fact, this is purely an artifact of how China defines urban population. In China, only people who live in cities with populations of larger than 100,000 are considered “urban”. In the U.S., that number is just 2500. So lots of China’s “rural” population isn’t even close to what Americans would consider “rural”.

In fact, when economists try to estimate China’s “Lewis Turning Point” — the point where a country no longer has surplus agricultural population to shift into urban manufacturing industries — they agree that China either reached it a while ago, or is reaching it right about now.

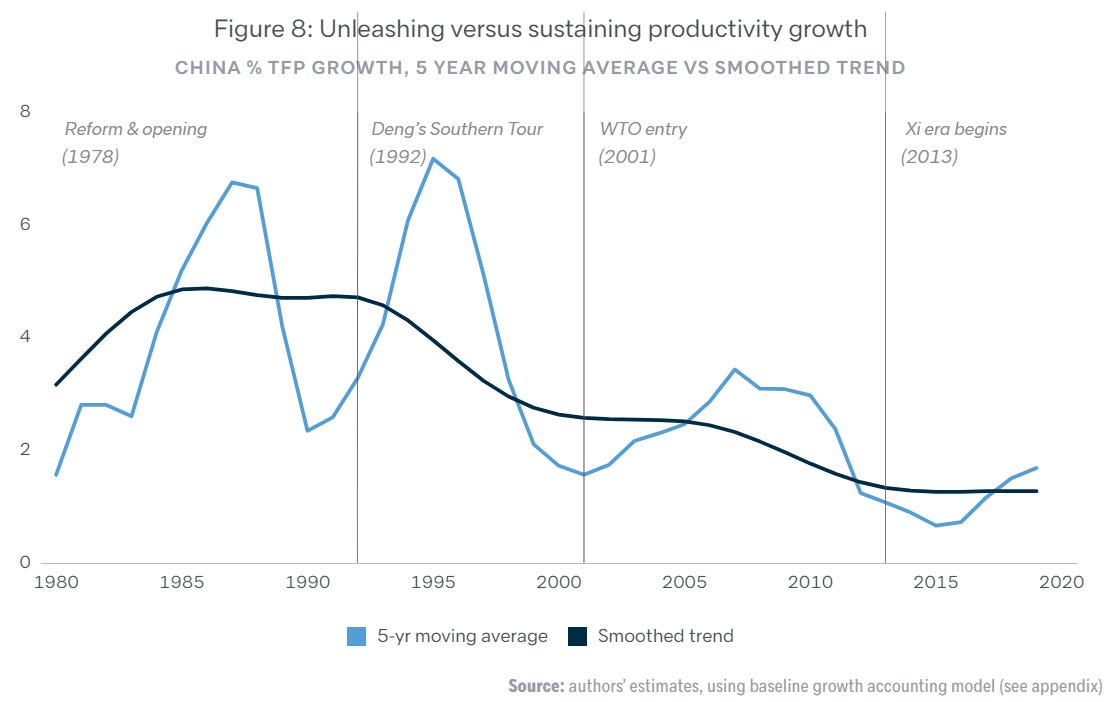

Productivity

Tooze and Hofman emphasize the fact that China still has only a little over 1/4 the per capita GDP of the U.S., and so still seems to have plenty of “room to grow”. But there are a great many countries in the world that fail to grow fast despite having plenty of room. In the past, China has fulfilled its potential; in the future, this may change.

The key here is productivity. You can build a lot of physical capital, but once you’ve built a certain amount, how rich you are relative to top countries like the U.S. depends entirely on how efficiently you use your resources of labor and capital.

And here, China has not been looking so amazing in the last 15 years or so. The Lowy Institute has a long and highly informative article with a great section on productivity (which Tooze links to). Here’s one of their graphs:

Even more damning, perhaps, is this graph, showing that China’s productivity slowed down at a much lower income level than other East Asian countries:

Now, as the experience of Taiwan, Korea, and Singapore show, it’s possible to dip and then recover, at least somewhat. But China’s productivity growth slowed so much earlier than that of its regional peers that even a modest re-acceleration would leave it significantly behind.

In other words, just because China has “room” to catch up with the rich countries doesn’t mean it will.

So what’s the positive case for a productivity acceleration here? Tooze and Hofman tout the country’s rising tertiary (college) education levels:

It is true that higher education tends to raise productivity, but looking at this graph, I immediately notice that some of the biggest gains in China’s educational achievement came at times when its productivity growth was simultaneously slowing to a crawl. That might indicate that China is not doing an amazing job of educating its college kids (as some rumors suggest).

Finally, Tooze touts Xi Jinping’s industrial policy, covered in depth in a recent Economist article. Basically, the idea here is that Xi is going to force China’s economy to divert resources away from industries like real estate, internet, and finance, and toward industries like semiconductors, artificial intelligence, robotics, electric vehicles, and the internet of things, and that this will result in big productivity gains.

In fact, I think it’s no exaggeration to say that this is the main hope for continued Chinese growth. But I also think that what Xi Jinping is trying to do is qualitatively different from the (occasionally successful) industrial policy drives that other countries have undertaken. He’s not just promoting the industries he likes; he’s trying to supercharge their growth by smashing the industries he doesn’t like. The idea seems to be that the economy’s industrial structure is like a tube of toothpaste, and if you squeeze one end, capital and labor and human ingenuity will spurt out the other end. Industrial policy is usually about picking winners; Xi wants to pick losers too.

I am skeptical that this will work. Sure, Xi can probably get a little mileage from pumping up the industries of the future (though even there it will depend on competence in execution, which is generally the exception rather than the norm). But I don’t think most of the untold millions of Chinese people who are forced to quit building and financing apartment buildings are going to start successful, innovative companies in AI and robotics. They just don’t know how to do that.

And I think Xi already sort of realizes that. Already, in the face of slowing growth, the government is trying to partially back away from its crackdown on internet companies. But at this point the damage has probably been done, not just to that industry but to entrepreneurship everywhere. It’s going to be harder, going forward, to get innovative entrepreneurship in any sector other than the ones Xi explicitly supports.

So while it’s conceivable that Xi will be able to pull off some totally novel industrial policy magic, the chances don’t look great — unless you’re one of those people who think that the Chinese government is just operating on another level from every other government that has ever existed, which is a thing that some people do think.

Anyway, to sum up, the continued bull case for Chinese growth rests to a large degree on optimistic assumptions about two things:

China’s ability to counteract extremely unfavorable demographics by having old people stay in their jobs longer, and

Xi Jinping’s ability to invent whole new and wildly successful forms of industrial policy.

I don’t think I quite buy this case just yet.

The reason Chinese workers retire in their mid-50s is a result of a deliberate policy. Grandparents are expected to leave the workforce to be the primary adults raising their grandkids. Their adult children -- ostensibly in their working prime -- are thus freed up to work harder and longer, secure in the knowledge that Grandma and Grandpa have the kids covered.

Raising the retirement age would mean the country would need to seriously up its number of child care workers. It would also dismantle the strong family ties and cultural continuity inherent in the current system. The timing seems particularly bad now that the one-child policy is nearly a decade in the past, and Chinese families are having more kids, which means they're more reliant on this system, not less.

This policy doesn't exist in a vacuum; and the reason it exists needs to be accounted for in any discussion of changing it.

There are also some people who think China will be able to raise their TFR again. The argument generally goes that just like they were able to crush fertility rates due to their strong social control and heavy handed one child policies, they will be able to leverage their agitprop to generate a pro-natal society, and if that doesn't work they can just fall back on policies that are equally as heavy handed as the one child rule, such as restricting abortion or placing taxes on childless adults.

I am skeptical. Western interventions have shown that pro-natal policies can work, but even wide ranging support structures have surprisingly limited effect. Tax rebates and free kindergartens work and are important, but can only do so much compared to other economic trends and societal expectations. "Negative" policies such as restricting access to abortion have probably little to no effect (though that may help with the gender balance). They obviously can't ban contraceptives. Banning after school online courses could help let's see how that works out.

Using their control over societal opinion isn't going to be very effective either. By now having one child is the norm, and the opinions I have heard from pro-natal advocates are essentially conservative boomeresque ramblings that are entirely divorced from the reality of young Chinese couples. Few young chinese women are interested in playing an entirely subservient role to their husbands and place their career on hold to bear and raise more children.

To raise their TFR to more manageable levels, China needs, in that order: happier mothers, happier families, and a happier society. That means more affordable homes, more support for families, and a more equal society that doesn't delay the career of mothers. It currently pulls sone of the right levers, but simply not enough of them.