Disinflation begins

Prices are starting to decelerate, but the cause isn't yet clear.

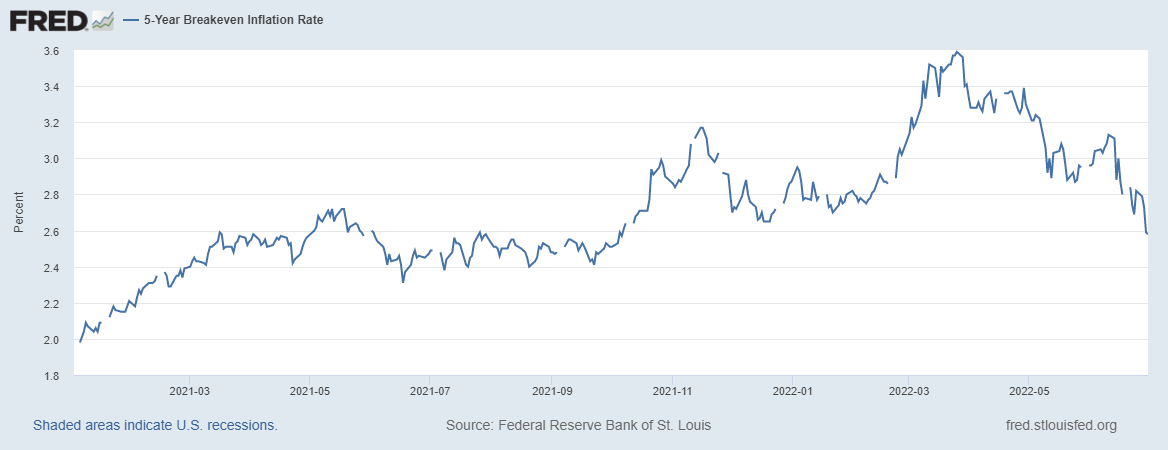

For over a year now, we’ve seen inflation rise relentlessly. Price rises have lowered real wages for most workers, driven popular anger, and threatened economic stability. But there are finally indications that the tide is turning. In March, financial markets were predicting an annualized inflation rate of around 3.5% over the next five years; now, that number is down to 2.6%.

And expectations for inflation over the following five years, which had spiked up during the initial phase of the Ukraine war, have plunged back toward the Fed’s official 2% inflation target:

So markets think prices are going to cool down. That’s good in and of itself, because it means we’re in less danger of the sort of expectations-driven spiral that can lead to truly devastating hyperinflation. Markets have not yet lost confidence in the Fed. But this doesn’t mean we’re out of the woods, since markets are actually pretty bad at predicting future inflation.

But fortunately, there are a number of other indicators that suggest we’re heading for disinflation. (Note: “disinflation” means that inflation is positive but lower than before, while “deflation” means prices actually go down. Deflation is an economic emergency; disinflation is what we actually want right now.)

The signs of disinflation

Here is a list of indicators I’ve noticed in recent weeks that portend a lower inflation rate.

1. Falling freight rates

The explosion of container shipping prices in 2021 was the result of the supply chain snarls that we spent much of the last year talking about. These aren’t consumer prices, but they definitely feed into consumer prices. And when container rates fall, it suggests bottlenecks in the system are working themselves out.

2. Falling commodity prices

Commodities are ingredients into production, so when they get cheaper it means that production costs go down. Also, while energy and food prices aren’t included in the “core” inflation measure that the Fed pays attention to, they are probably the prices that hit American consumers the hardest and make them the angriest. So it’s a relief to see that food prices are now falling worldwide, and gasoline prices may also be starting to fall as well.

3. Easing rents

For people who pay rent, it’s generally their single biggest monthly expense, so falling rents will be a huge relief for many consumers, especially lower-income consumers. But easing rents also signal a cooling off of the red-hot housing market, which is historically the biggest single factor in the business cycle.

4. Cheaper GPUs

Chips were the most important commodity that was in noticeably short supply in early 2021. They’re an input into all kinds of manufactured goods, from cars to electronics to household appliances. So it’s good to see that prices for GPUs are tanking.

5. Rising retail inventories

Rising inventories and slowing sales are a sign of a cooling economy. They’re also a sign of cooling prices, since retailers will have to make significant markdowns to clear our their inventory.

Update: The excellent Barry Ritholtz has more here, and the excellent Joe Weisenthal and Tracy Alloway have yet more here.

Is it supply or demand?

The next question is: What’s causing the disinflation? There are two basic possible explanations. The first is supply. Perhaps logistics and shipping firms have worked out the kinks in their supply chains. And perhaps manufacturers and miners and farmers have ramped up their production in response to high prices. The second possible explanation is demand — perhaps aggressive Fed rate hikes and balance sheet reductions, along with falling government spending and a negative wealth effect from the stock and crypto crashes, have cooled off the economy. People argue back and forth about how much of the recent inflation was caused by supply factors vs. demand factors; soon we will be having a similar argument about disinflation.

In the real world — and also in academic macro theories — the relationship between supply and demand is not so simple. There are expectations, lags (delayed effects), feedback loops, and a bunch of other complicating factors. But if we want to use the simple AD-AS (aggregate demand and aggregate supply) model, then it basically goes like this: If prices go down and output goes up, then supply increased, but if prices go down and output also goes down, then demand decreased. Of course, you can have both of these at once; in this case, the effect on output will be relatively muted, while both factors push prices down.

GDP numbers for the second quarter won’t be out for a while, but already we can see a few indicators showing slowing economic activity. Consumer spending is now falling in inflation-adjusted terms, while manufacturing is slowing and home sales have been trending down. That suggests that the Fed is succeeding in its mission to cool off the economy. But capital spending has remained firm, and employment numbers have held up, so we’re still getting mixed signals on the real economy. It’s not clear how severe a recession we’re going to get.

Meanwhile, there are definite signs that supply is increasing. U.S. oil production is rising, Russian production is recovering as it sells more to China (at a discounted price), and OPEC has pledged to drill more as well. Miners are mining more minerals and chipmakers are making more chips. There’s also falling demand in China due to Covid lockdowns and a real estate crash; this actually acts like a positive supply shock for America, because it means China is buying fewer commodities on the world markets, leaving more for us.

So it’s reasonable to think that both supply increases and demand destruction are at work here. The goldilocks scenario here, of course, is that the Fed manages to cool off the economy just enough to bring down inflation, but no more. The Federal Bank of New York thinks there’s only a 10% chance we’ll get this “soft landing”, but Goldman Sachs thinks we’re still on track to pull it off. So it’s really up to whose forecast you want to believe, there.

But basically, the more supply increases, the better off we’ll all be. Just as negative supply shocks force a bad tradeoff on the Fed — tank the economy or let inflation run wild — increases in supply make the Fed’s job easier. Thus, although it’s important for the Fed to do its job and keep the pressure on inflation, the President and Congress should be focus on doing everything they can to boost supply — especially of oil, computer chips, and other crucial production inputs. The sooner the world gets flooded in cheap commodities, the sooner the Fed can ease up on the economy.

Not disagreeing with the broader thrust of this article, but:

Second-hand GPU prices are not indicative of the broader chip market, certainly not the cheap-and-simple chips that the automotive industry uses by the million and is is still very short of.

I'd add another tidbit to your list: I'm starting to see a few discounts on (some types of) bicycles again. The bicycle industry saw the same supply challenges as all other manufacturing industries over the past couple of years, coupled with particularly high demand both from cash burning a hole in pockets and cycling being one of the least restricted activities.

Thanks, very useful post and in accord with some of what I've been looking at. Unfortunately, the decreases are out in the future and likely not to help the Dems this November.