America is getting the economy we voted for

The beatings will continue until someone comes in and fudges the data.

Noahpinion began as a macroeconomics blog. So every once in a while I feel like I ought to report on the macroeconomic situation.

Fortunately, the header image at the top of this post is not a picture of where the U.S. economy stands today; it’s not yet a sinking ship. But with the real economy looking shaky and inflation persistently above target, things are not looking great. The worst news, however, is that the people in charge of the economy don’t look like they have any desire to right the ship; instead, they’re the ones who caused the problems in the first place, and they seem to have every intention of doubling down.

First let’s talk about some of the latest numbers. We basically want our economy to do two things: 1) give everyone a job with a good income, and 2) keep prices stable. In other words, the “macroeconomy” can basically be boiled down to the labor market and inflation. Economic growth is important, but mainly because it makes everyone have a job and makes wages go up — in other words, when we say “the real economy”, we mean growth and the labor market, which are really the same thing.

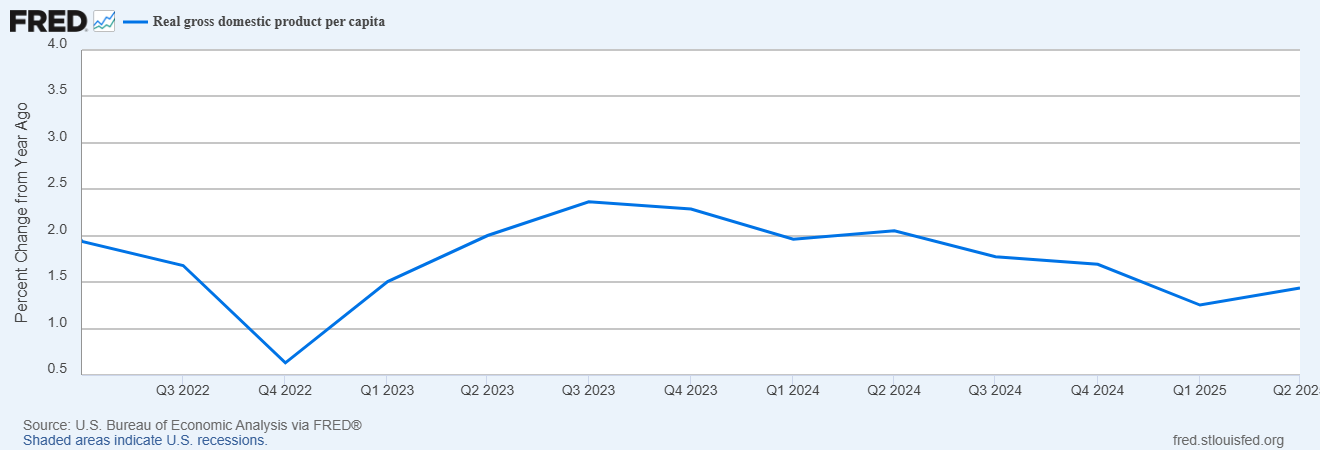

There’s not much action on the economic growth front — at least, so far. Growth has been kind of slow under Trump, but not in recession territory, and Q2 was actually slightly better than Q1:

But growth numbers only come out once every three months, while lots of labor market data comes out monthly. So if we want a more up-to-the-minute picture of how the economy is doing, we should look at things like job growth and the unemployment rate.

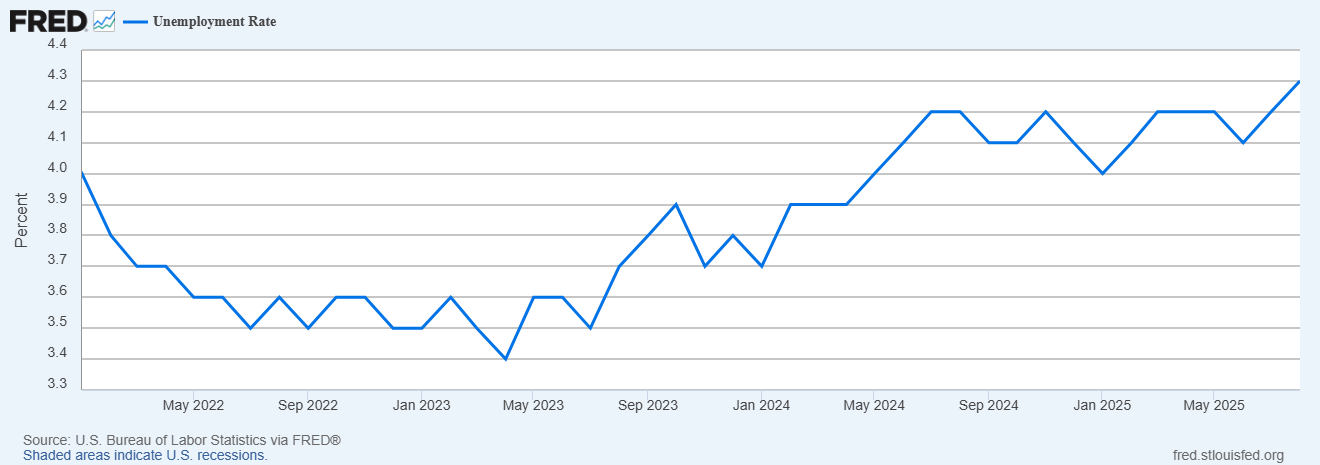

The unemployment rate just came out today, and it’s slowly rising. It’s still low in historical terms, at less than 5%, but it’s creeping steadily up:

A better measure of the overall health of the labor market is the prime-age employment rate (also called the “employment-population ratio”), which doesn’t depend on who says they’re looking for a job. As of August it was still at very high levels, just a little bit lower than it was in 2024:

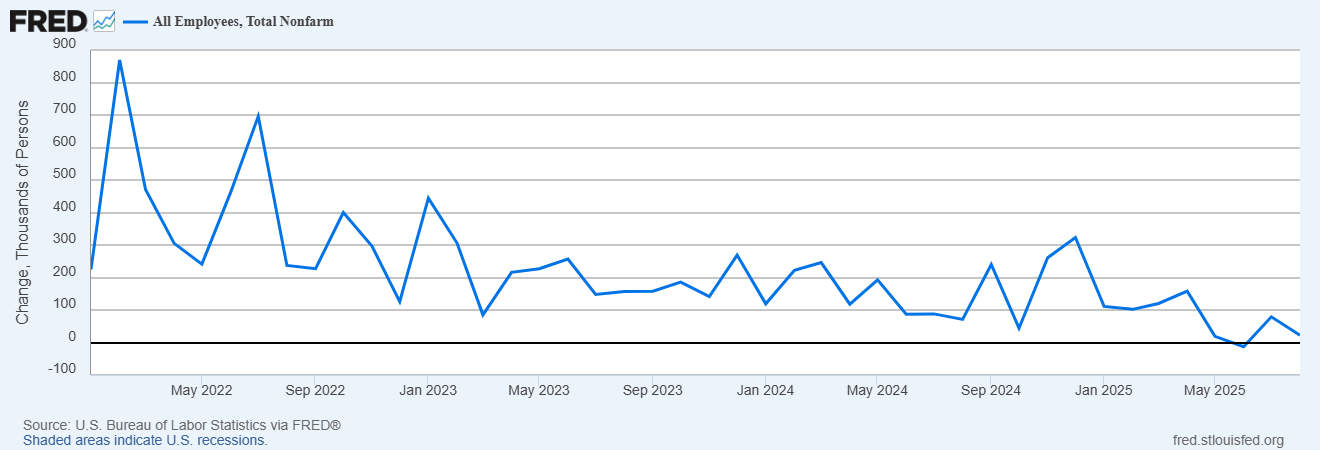

So that’s not too worrying, yet. But we have another source of data about jobs, which is a survey measuring how many jobs employers add each month — the “jobs numbers” that you always see reported in the media. The August numbers just came in, and they don’t look too hot:

The Bureau of Labor Statistics (BLS) reported that the U.S. added 22,000 jobs in August, well below expectations for 75,000. Employment data for June was revised to show a net loss for that month, the BLS said, though July’s figures were revised slightly higher…Taken together, the U.S. has added 598,000 jobs so far this year, compared with 1,144,000 for the first eight months of 2024.

In fact, job growth has been weak since Trump started announcing big tariffs on “Liberation Day” back in April:

Now, one possible reason we could have slow job growth with stable employment levels is that Trump could be forcing a bunch of illegal immigrants out of the country. If you don’t care about jobs for illegal immigrants, then maybe that wouldn’t bother you. But the native-born unemployment rate has been creeping up as well:

And jobs for the native-born, which had been rising a bit, took a tumble in August as well.

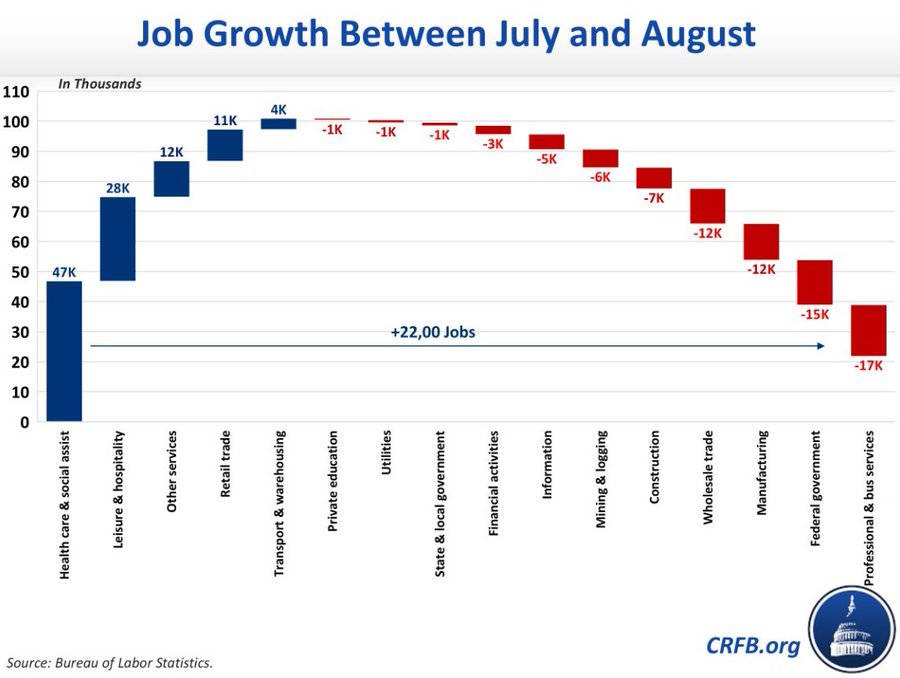

Also, when we look at which industries are seeing weak job numbers, a lot of them don’t look like the type of industries you’d expect to employ a lot of illegal immigrants:

We can also look at some other various numbers to get an overall picture of the health of the labor market. ADP, the private payroll processing company, showed a slowdown in hiring last month:

U.S. private-sector hiring rose less than expected in August, data released Thursday shows, offering the latest indication of trouble in the labor market…Private payrolls increased by just 54,000 in August, according to data from processing firm ADP published Thursday morning. That’s below the consensus forecast of 75,000 from economists polled by Dow Jones, and marks a significant slowdown from the revised gain of 106,000 seen in the prior month.

Jobless claims are rising too:

Applications for US unemployment benefits rose to the highest since June, adding to evidence that the labor market is cooling…Initial claims increased by 8,000 to 237,000 in the week ended Aug. 30.

US job openings fell in July to the lowest in 10 months, adding to other data that show a gradually diminishing appetite for workers amid heightened policy uncertainty…Available positions decreased to 7.18 million from a downwardly revised 7.36 million in June, according to Bureau of Labor Statistics data published Wednesday. The median estimate in a Bloomberg survey of economists called for 7.38 million openings.

And a private-sector job placement firm reports that companies are reducing hiring plans and announcing more job cuts:

Hiring plans fell to the weakest level for any August on record and intended job cuts mounted amid broader economic uncertainty, according to outplacement firm Challenger, Gray & Christmas…US-based companies announced in August plans to add 1,494 jobs, the fewest for the month in data going back to 2009. Of the 30 industries tracked by Challenger, hiring plans were concentrated in aerospace and defense, industrial goods and retail…Announced job cuts jumped from a year ago to almost 85,980 and marked the largest August total since 2020. Excluding the impact of the pandemic, the number was the highest for any August since the Great Recession in 2008.

So basically, the labor market doesn’t look great. It’s not a catastrophe yet, but things are steadily weakening.

How will the Trump administration respond? One thing they’ll probably try to do is to cook the books, by firing government employees who report accurate economic numbers, and bringing in apparatchiks who massage the numbers to make the news look better. After the previous month of bad jobs numbers, Trump fired the head of the Bureau of Labor Statistics and replaced her with — to put it quite bluntly — a partisan operative who appears to know little about economics.

This will be harder than simply putting Trump’s loyal apparatchiks in charge, though. There are a lot of different economic numbers, and the U.S. government is very transparent about how it collects them. If you mess with them, everyone will know the numbers are now fake, and economic confidence will plummet. Furthermore, political operatives who don’t actually understand economic numbers in the first place will naturally have trouble figuring out how to cook the books in a consistent way.

Another thing Trump will try to do is to blame the Fed for the weak labor market. This will gain a lot more traction — even the New York Times says that the latest jobs numbers strengthen the case for rate cuts. So Trump’s next move will be to try to get the Fed to bail him out. And this will probably work; Fed Chair Jerome Powell says that the time has come for rate cuts.

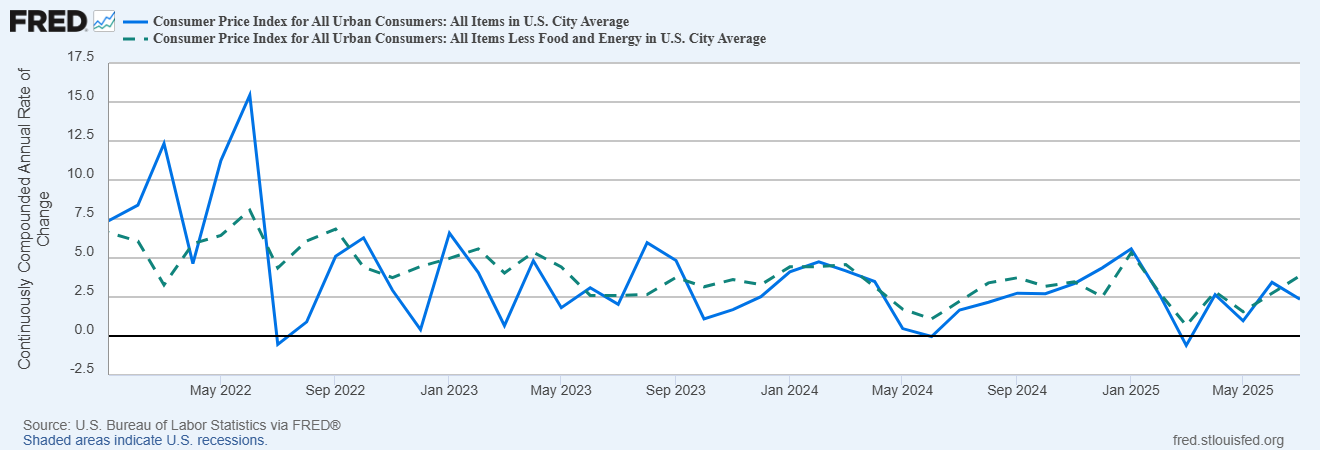

But there’s a reason why this won’t fix everything that’s wrong with the macroeconomy. Rate cuts work by boosting aggregate demand. When aggregate demand is too low, inflation should be low as well (because people are paying less for things, so prices aren’t being pushed up). But inflation is higher than the 2% target, and looks like it’s creeping back up:

And markets are expecting inflation to stay above target for the next 5 years.

This suggests that the economy’s gradual slowdown is being caused not by high rates, but by a shortage of aggregate supply. When there’s a negative supply shock, you can still boost the labor market by cutting rates, but this comes at a steeper price — you end up exacerbating inflation. Many economists argue that this is what the Fed did in the 1970s, when it cut rates to support the job market during an oil shock.

The current supply shock isn’t as bad as the 1970s, obviously. 2.5% inflation is not that bad. But the problem here is that unlike in the 1970s, the supply shortage has an obvious cause: Trump’s tariffs, which are making it harder for manufacturers to produce things by cutting them off from their supply chains.

Jason Furman notes that Trump’s immigration crackdown is yet another negative supply shock. Trump’s ICE recently raided a Hyundai factory in Georgia, arresting hundreds of factory workers.

Plenty of data show U.S. manufacturing in a parlous state. The Institute for Supply Management is showing a contraction in the sector, and everyone agrees that tariffs are to blame:

US factory activity shrank in August for a sixth straight month, driven by a pullback in production that shows manufacturing remains bogged down by higher import duties…The group’s index of factory output sank 3.6 points to 47.8, moving back into contraction territory for the first time in three months.

Iconic American companies like John Deere are suffering from the higher prices they now have to pay for imported materials like steel and aluminum.

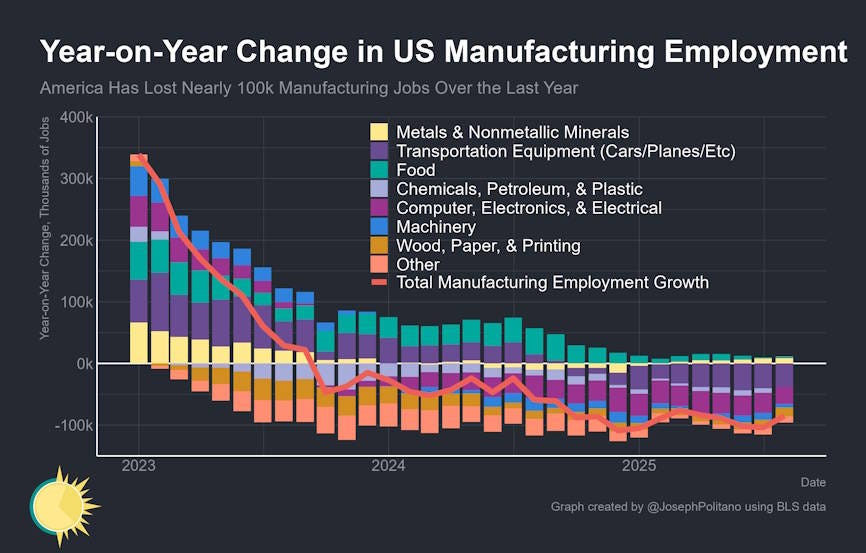

Manufacturing employment isn’t doing great either. It was shrinking in 2024 (possibly due to rate hikes), but is shrinking much faster since Trump took office:

America has now lost about 78,000 manufacturing jobs in 2025, on net. Manufacturing, of course, is uniquely exposed to tariffs because of its reliance on supply chains.

In other words, the sky is not yet falling, and the ship is not yet sinking, but the Trump administration is doing everything it can to make things worse. The U.S. economy is incredibly resilient, but if you hit it with enough bad policies, even the most resilient economy will sour. We’re now seeing a slow souring of our economy — a new normal that the government just expects Americans to accept, in service of ideological goals that most of the population doesn’t share.

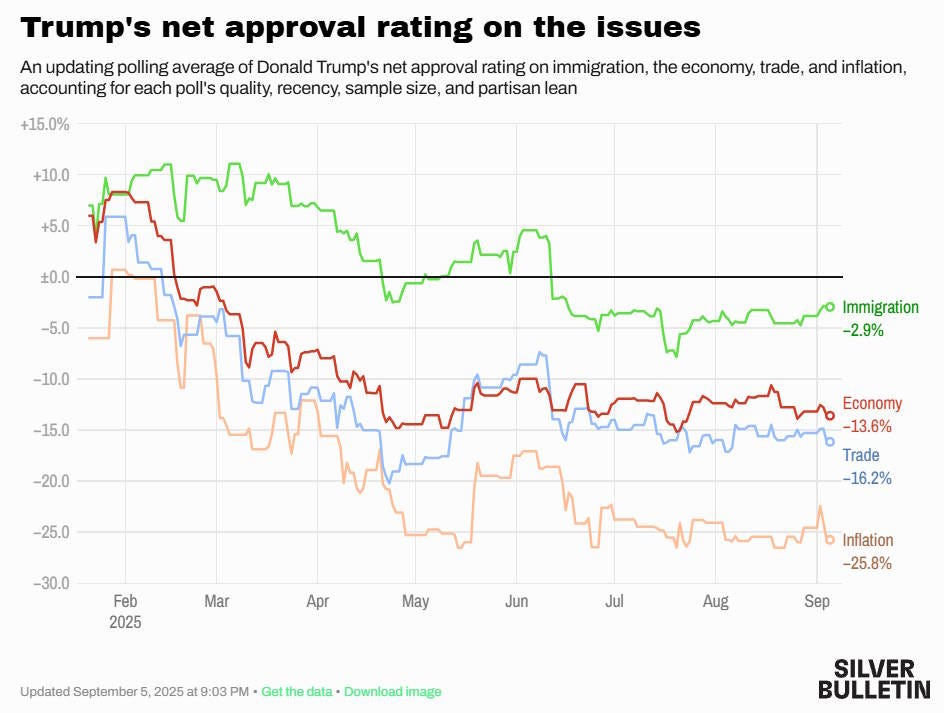

Americans are not exactly happy about this, giving Trump lower ratings on economic issues than on cultural issues like immigration:

But so far, the economy isn’t bad enough, nor the anger severe enough, to pose a serious threat to Trump.

America is getting the macroeconomy it voted for, and it’s grumblingly accepting it.

"This is exactly what I voted for" is the chant from the MAGAverse. "Donald Trump's Tariffs are working". "Just look at how much money has been collected due to tariffs". Tariffs are money that could have been used to employ more workers and increase productivity. That money is now going into government coffers instead of the economy and the Government is spending lots more money on building a paramilitary agency which will enforce Trump's fantasy of total control. We are paying Donald Trump to build himself a personal army of gunslingers who will do his bidding in a quest for power while we are poorer and have fewer jobs. And less security. "This is exactly what I voted for!" What could go wrong?

But Trump's voters are not getting the economy he promised them.

It was only after the election that Trump revealed that there was going to be pain before the Golden Age began.